Financial management for new ventures

TYPICAL FINANCIAL PROCESSES

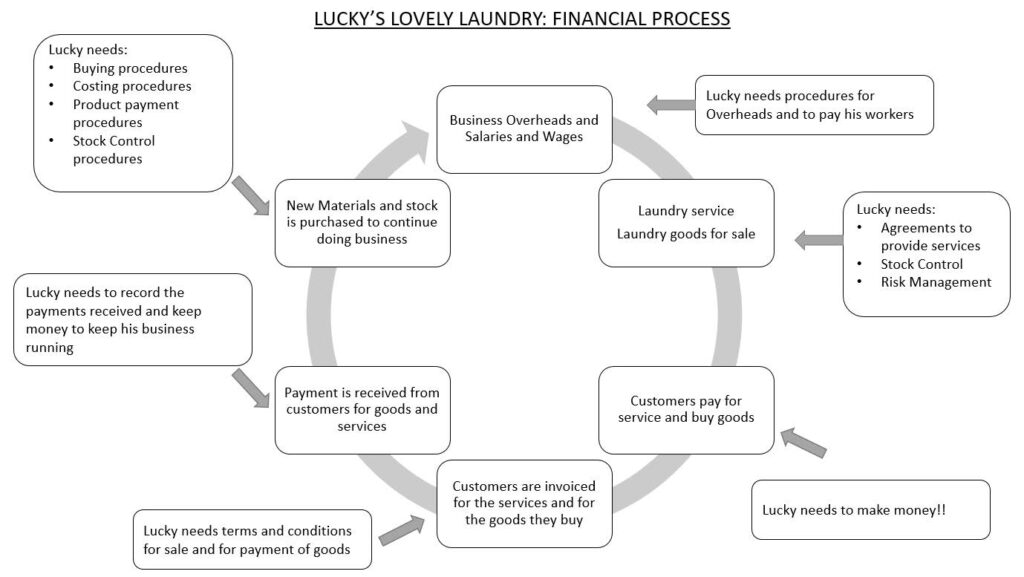

The following diagram illustrates a typical financial process. This is for Lucky’s Lovely Laundry. Lucky provides a service (he washes laundry) and also makes his own washing powder that his customers buy called “Lucky’s Magic Bubbly Wubbly”. His company is thus both a service and a goods company. He needs to make sure he follows the following process:

FINANCIAL CONCEPTS AND PRINCIPLES

The key financial concepts and principles that apply to new ventures include the following:

1: START-UP CAPITAL

Start-up capital is the money needed to begin your business. This would include everything essential for product development and the product launch. Before going after start-up capital make sure you know how much money you need, and then how you will apply those funds. Being as specific as possible with the plans for the money will increase the likelihood that your business will get financed.

WHERE DO YOU FIND START UP CAPITAL?

Banks are a straightforward source of funds. Many offer small-business loans if you’ve already started your business. You’ll need a business plan and perhaps a personal guarantee. The funds are a loan, so you must generate enough cash to cover loan payments.

Finding friends and family who will invest in your start-up is straightforward: Start calling. You’re after high-net-worth investors who take personal referrals seriously. The best way to find them is through personal networking.

Suppliers and customers may also back you. If your product complements a supplier’s, they might invest–for example, if you distribute its music, a record label might want to invest. Be careful, though: Taking money from a supplier may prevent you from using that supplier’s competitors.

Strategic investors get their return in many forms: increased sales of their own products, stock sale of your company, advertising through your distribution channels, etc. These arrangements are rarely made just for a cash return, so the payback can take many forms.

- WORKING CAPITAL

Working capital is the amount of money that a company has tied up in funding its day to day operations. It is regarded as the lifeblood of a business without which, a company can become bankrupt. A company has to tie up money to fund its stock, credit sales and other current assets, but this is offset by its ability to fund this from current liabilities; liabilities such as purchases on credit. If a company buys on credit it does not have to tie up (as much) money in its stocks. In some businesses (such as grocery retail) working capital can even be negative. A business that buys on credit and sells for cash is being partly funded by its suppliers.

Changes in working capital will impact a business’ cash flow. When working capital increases, the effect on cash flow is negative. This is often caused by the liquidation of inventory or the drawing of money from accounts that are due to be paid by the business. On the other hand, a decrease in working capital translates into less money to settle short-term debts.

When a company has too little working capital, it can face financial difficulties and may even be forced toward bankruptcy. This is true of both very small companies and billion-dollar organizations. A company with this problem may pay creditors late or even skip payments. It may borrow money in an attempt to remain afloat. If late payments have affected the company’s credit rating, it may have difficulty obtaining a loan at an affordable interest rate.

In some types of businesses, it isn’t as much of a problem to have a lower amount of working capital. Companies that are operated on as cash basis, have fast inventory turnovers, and can generate cash quickly don’t necessarilyneed as much working capital. For example, a grocery store might meet these requirements and do well with less working capital.

- CASHFLOW MANAGEMENT

Cash flow management is the process of monitoring, analyzing, and adjusting your business’ cash flows. For small businesses, the most important aspect of cash flow management is avoiding extended cash shortages, caused by having too great a gap between cash inflows and outflows. You won’t be able to stay in business if you can’t pay your bills for any extended length of time!

Therefore, you need to perform a cash flow analysis on a regular basis, and use cash flow forecasting so you can take the steps necessary to head off cash flow problems. Many software accounting programs have built-in reporting features that make cash flow analysis easy. This is the first step of cash flow management.

The second step of cash flow management is to develop and use strategies that will maintain an adequate cash flow for your business. One of the most useful strategies for small businesses is to shorten your cash flow conversion period so that your business can bring in money faster.

This short story illustrates that cash is king . . .

I must have cash; my income statement shows that I made a profit this month?

When I was growing up in the country-side of North Georgia, one of my first jobs was manually picking up eggs on a chicken farm. Now for those of you who are not familiar with that process let’s just say that it is not pleasant experience.

Basically, you go to the chicken coop and steal the eggs from underneath a sitting hen while trying not to get pecked to death or pooped on. Chickens it seems have the same motherly instinct as other fowl, and do not take kindly to someone coming into their nest and stealing their eggs. Thankfully, technology has made the process of sending 12 year olds into the chicken house to steal eggs obsolete. Now, when the hen lays her eggs, they miraculously disappear from the nest through a trap door onto a conveyor belt to be collected in a nice safe place. Lucky me, I was just born too early have this the technology!

So, why was I willing to undertake such an unpleasant task at the tender age of 12? It was for one reason and one reason only! CASH! The owner of the farm always paid me in CASH! I would run home to my dad and show him the CASH that I had made from my work at the farm. It was a great experience!

At around the age of fourteen, I got tired of breathing what seemed like one hundred percent ammonia and fighting chickens for their eggs. No matter how much CASH I came out with at the end of the week I was done in the egg business. The next summer, I started another venture; a lawn mowing service.

It was in this little venture that I learned the truth of Law #15 – Cash flow is more important than profit.

The story goes like this. I had around 10 customers. I would mow lawns for them on a weekly basis at an agreed upon price. I did the work during the day and for most of my customers, I would receive CASH when I completed the yard. For some customers, I would collect the CASH later because they were at work during the day and not at home to pay me. For those customers, I would leave a note with my bill for cutting the lawn and tell them that I would be back to collect the money.

While all of my customers always paid me, the timing of the payment depended upon when I went back to collect on the account.

One week during my summer of lawn mowing, I had a chance to go to Six Flags Over Georgia, an amusement park in Atlanta. The only requirement was that I had enough money to purchase the ticket in cash when I arrived at the park on Friday.

I worked very hard that week to complete my lawns so I would have the money to buy my ticket. For some reason that week, most of my customers were not home at the time I mowed the lawn.

I left them my customary note and told them I would be by collect before Friday. For whatever reason, I was unable to collect the cash by Friday. Frankly, I do not remember the specific circumstances of why I was unable to collect the money. What I do remember is that I could not go to the amusement park because they were not interested in taking my accounts receivable aging report as payment for the ticket.

That was when I learned Law # 15 – Cash Flow is More Important than Profit. On paper, I made the same amount of profit as in all the other weeks. I cut the same number of yards, charged the same amount of money and had the same expenses. There was only one difference! I did not have sufficient cash flow to go to the amusement park.

(Apparently, I had a spending problem as well, or I could have used some cash from previous weeks.)

Source: http://www.amplifyadvisors.com

RELATIONSHIP BETWEEN CASHFLOW AND PROFIT

Best known measure of the success of an enterprise, it is the surplus remaining after total costs are deducted from total revenue, and the basis on which tax is computed and dividend is paid.

There is a relationship between cashflow and profit. Making profit generates cash flow. Any business owner knows that. But the actual increase in cash during a given period is invariably lower or higher than the profit number. The following points illustrate how cash flow relates to profit:

– The amounts of cash flows during the period rarely are equal to the revenue and expense numbers in the P&L (profit and loss) report for the period.

– Actions that lower cash flow: increasing accounts receivable and inventory; decreasing accounts payable and accrued expenses payable.

– Actions that raise cash flow: decreasing accounts receivable and inventory; increasing accounts payable and accrued expenses payable.

– Depreciation expense is not a cash outlay in the period recorded; neither is amortization expense; unusual losses recorded in the period may not involve cash outlay but rather be write-downs of assets or write-ups of liabilities.

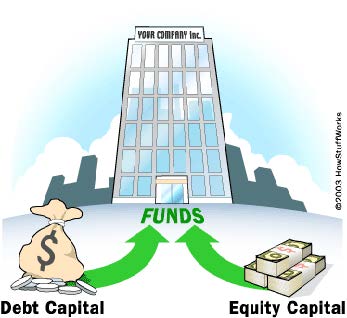

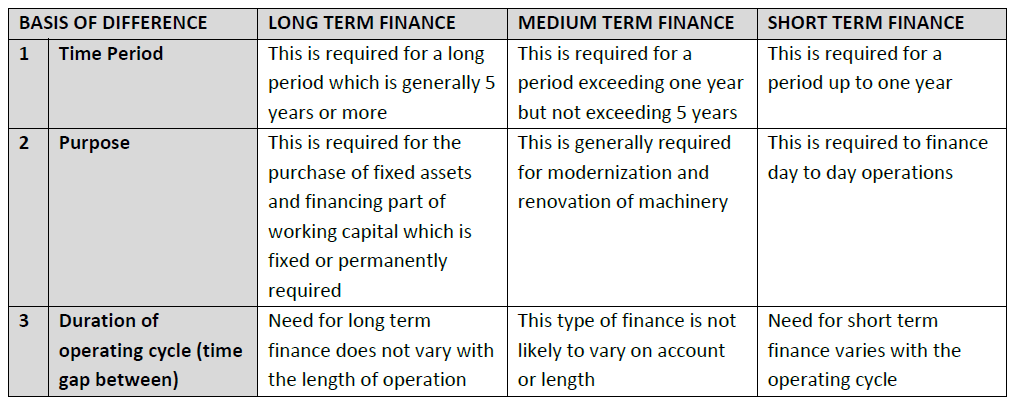

LONG TERM AND SHORT TERM FINANCING

A venture depends on financing in order to maintain its cashflow and also to buy necessary assets required in the business. Financing available to a new venture can be divided into;

- Short term financing and

- Long term financing

- SHORT TERM FINANCING

Short-term finance is that financial boost that helps a new venture to meet their temporary requirements of money (usually not exceeding 12 months). They do not create a heavy burden of interest on the organisation. Usually after establishment of a business, funds are required to meet its day to day expenses. For example, raw materials must be purchased at regular intervals, workers must be paid wages regularly, water and power charges have to be paid regularly. Thus there is a continuous necessity of liquid cash to be available for meeting these expenses. For financing such requirements short-term funds are needed. The availability of short-term funds is essential. Inadequacy of short-term funds may even lead to closure of business.

FORMS OF SHORT TERM FINANCING

There are a number of sources of short-term finance which are listed below:

– Trade credit

– Bank credit

– Loans and advances

– Cash credit

– Overdraft

– Discounting of bills

– Customers’ advances

– Instalment credit

PURPOSE OF SHORT TERM FINANCING

Short-term finance serves the following purposes:

- It facilitates the smooth running of business operations by meeting day to day financial requirements.

- It enables firms to hold stock of raw materials and finished product.

- With the availability of short-term finance goods can be sold on credit. Sales are for a certain period and collection of money from debtors takes time. During this time gap, production continues and money will be needed to finance various operations of the business.

- Short-term finance becomes more essential when it is necessary to increase the volume of production at a short notice.

MERITS OF SHORT-TERM FINANCE

Economical: Finance for short-term purposes can be arranged at a short notice and does not involve any cost of raising. The amount of interest payable is also affordable. It is, thus, relatively more economical to raise short-term finance. Flexibility: Loans to meet short-term financial need can be raised as and when required. These can be paid back if not required. This provides flexibility.

No interference in management: The lenders of short-term finance cannot interfere with the management of the borrowing concern. The management retain their freedom in decision making.

May also serve long-term purposes: Generally business firms keep on renewing short-term credit, e.g. cash credit is granted for one year but it can be extended up to 3 years with annual review. After three years it can be renewed. Thus, sources of short-term finance may sometimes provide funds for long-term purposes.

DEMERITS OF SHORT-TERM FINANCE

Short-term finance suffers from a few demerits which are listed below:

Fixed Burden: Like all borrowings interest has to be paid on short-term loans irrespective of profit or loss earned by the organisation. That is why business firms use short-term finance only for temporary purposes.

Charge on assets: Generally short-term finance is raised on the basis of security of moveable assets. In such a case the borrowing concern cannot raise further loans against the security of these assets nor can these be sold until the loan is cleared (repaid).

Difficulty of raising finance: When business firms suffer intermittent losses of huge amount or market demand is declining or industry is in recession, it loses its creditworthiness. In such -circumstances they find it difficult to borrow from banks or other sources of short-term finance.

Uncertainty: In cases of crisis business firms always face the uncertainty of securing funds from sources of short-term finance. If the amount of finance required is large, it is also more uncertain to get the finance.

- LONG TERM FINANCING

As the name suggests, Long term financing is a form of financing that is provided for a period of more than a year. Long term financing services are provided to those business entities that face a shortage of capital. It is different from short term financing which is normally used to provide money that has to be paid back within a year. The period may be shorter than one year as well.

Examples of long-term financing include

– 30-year mortgage or a 10-year Treasury note.

– Equity, such as when a company issues stock to raise capital for a new project.

– Medium term loans

PURPOSE OF LONG TERM FINANCE:

Long-term finance serves the following purposes:

- To finance fixed assets.

- Expansion of companies.

- To finance the permanent part of working capital.

- Increasing facilities.

- Construction projects on a big scale.

- Provide capital for funding the operations. This helps in adjusting the cash flow.

The table below summarises the difference between long term, medium term and short term financing.

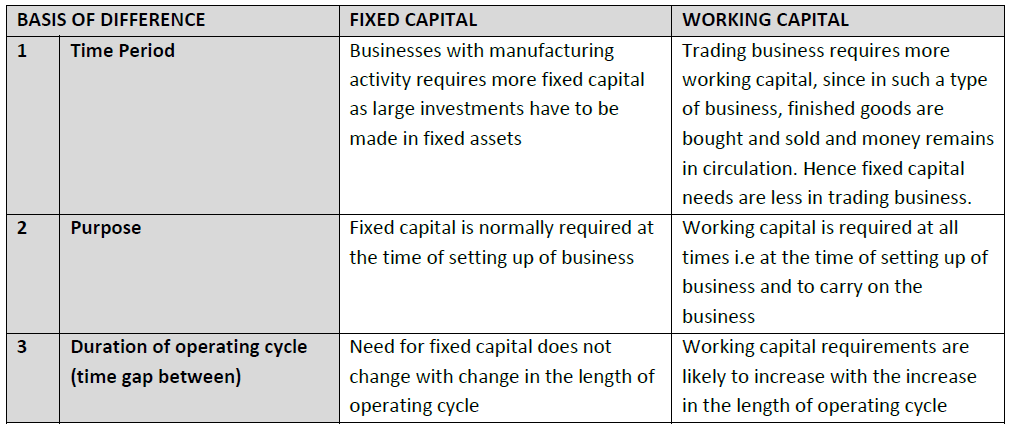

FIXED CAPITAL AND WORKING CAPITAL

Fixed capital refers to the total value of assets in a business which are of durable nature and used in a business over a considerable period of time. It comprises of assets like land, building, machinery, furniture etc. The capital invested in these assets is fixed in the sense that these are required for permanent use in business and not for sale.

On the other hand, working capital consists of those assets which are either in the form of cash or can easily be converted into cash, e.g. cash and bank balances, debtors, bills receivable, stock, etc. These assets are also known as current assets. Working capital is needed for day to day operations of the business. However, a part of working capital is required at all times to maintain minimum level of stock and cash to pay wages and salaries etc. This part of working capital is called ‘permanent’ working capital.

The following table shows the difference between fixed and working capital

APPLY CASH FLOW MANAGEMENT IN THE RUNNING OF A NEW VENTURE.

INTRODUCTION

Business analysts report that poor management is the main reason for business failure. Poor cash management is probably the most frequent stumbling block for entrepreneurs.

CONCEPTS OF CASH FLOW

Understanding the basic concepts of cash flow will help one to plan for the unforeseen eventualities that nearly every new venture faces.

CASH

Cash is ready money in the bank or in the business. It is not inventory, it is not accounts receivable (what you are owed), and it is not property. These can potentially be converted to cash, but can’t be used to pay suppliers, rent, or employees. Profit growth does not necessarily mean more cash on hand. Profit is the amount of money you expect to make over a given period of time, while cash is what you must have on hand to keep your business running. Over time, a company’s profits are of little value if they are not accompanied by positive net cash flow. You can’t spend profit; you can only spend cash.

CASH FLOW

Cash flow refers to the movement of cash into and out of a business. Watching the cash inflows and outflows is one of the most pressing management tasks for any business. The outflow of cash includes those checks you write each month to pay salaries, suppliers, and creditors. The inflow includes the cash you receive from customers, lenders, and investors.

POSITIVE CASH FLOW

If its cash inflow exceeds the outflow, a company has a positive cash flow. A positive cash flow is a good sign of financial health, but is by no means the only one.

NEGATIVE CASH FLOW

If its cash outflow exceeds the inflow, a company has a negative cash flow. Reasons for negative cash flow include too much or obsolete inventory and poor collections on accounts receivable (what your customers owe you). If the company can’t borrow additional cash at this point, it may be in serious trouble.

THE COMPONENTS OF CASH FLOW

A “Cash Flow Statement” shows the sources and uses of cash and is typically divided into three components:

I. Operating Cash Flow, often referred to as working capital, is the cash flow generated from internal operations. It comes from sales of the product or service of your business, and because it is generated internally, it is under your control.

II. Investing Cash Flow is generated internally from non-operating activities. This includes investments in plant and equipment or other fixed assets, nonrecurring gains or losses, or other sources and uses of cash outside of normal operations.

III. Financing Cash Flow is the cash to and from external sources, such as lenders, investors and shareholders. A new loan, the repayment of a loan, the issuance of stock, and the payment of dividend are some of the activities that would be included in this section of the cash flow statement.

CASH-FLOW CYCLE

Cash flow can be described as a cycle: your business uses cash to acquire resources. The resources are put to work and goods and services produced. These are then sold to customers, you collect and deposit the funds, and so the cycle repeats. But what is crucially important is that you actively manage and control these cash inflows and outflows. It is the timing of these money flows which can be vital to the success, or otherwise, of your business.

It must be emphasised that your profits are not the same as your cash flow. It is possible to project a healthy profit for the year, and yet face a significant and costly monetary squeeze at various points during the year such that you may worry whether your company can survive.

INFLOWS

Inflows are the movement of money into your business. Inflows are most likely from the:

– receipt of monies from the sale of your goods/services to customers;

– receipt of monies on customer accounts outstanding;

– proceeds from a bank loan;

– interest received on investments;

– investment by shareholders in the company.

OUTFLOWS

Outflows are the movement of money out of your business. Outflows are most likely from:

– purchasing finished goods for re-sale;

– purchasing raw materials and other components needed for the manufacturing of the final product;

– paying salaries and wages and other operating expenses;

– purchasing fixed assets;

– paying principal and interest on loans;

– paying taxes.

Note: Cash flow management is all about managing the inflows and outflows of money in a new venture.

IMPORTANCE OF CASH FLOW MANAGEMENT

Everyone knows the saying “it takes money to make money.” No truer words have been spoken. A business needs money in order to purchase materials for resale, pay its employees, and to cover all of the other expenses. The revenues collected from your customers are needed to pay the expenses and turn a profit. If your customers are not paying timely, or not paying at all, your business will soon be without the cash flow it needs to pay its own expenses.

Cash flows are also the fundamental source of intrinsic (or economic) value for the firm or for any other type of financial investment. Private firms are valued using estimates of the future cash flows the business operation will be able to generate. Public companies have their common stock prices determined by supply and demand forces in the stock markets that are influenced by the cash flows the stock investments will return to investors over time. For the investors who are buying the stock, potential cash flows from different investment opportunities (including stocks) provide the information that allows them to decide where to invest their money. As a measure of liquidity, cash flow, or more precisely stated, consistent and accurate evaluation of cash flow, can lend tremendous insight to any business owner about not only the current condition of their company but, also, the probability of certain potential future states of their company.

SUMMARY:

The advantages are straightforward.

– You should know where your cash is tied up.

– You can spot potential bottlenecks and act to reduce their impact.

– You can plan ahead.

– You can reduce your dependence on your bankers and save interest charges.

– You can identify surpluses which can be invested to earn interest.

– You are in control of your business and can make informed decisions for future development and expansion

CASH FLOW FORECAST

One key skill in cash flow management is forecasting and managing company cash flow. Too few business owners use financial forecasting to identify potential financial issues that can impact earnings. Once learned, forecasting can help small business owners smooth out the regular ups and downs that all companies experience as a normal course of business. In fact, the firm’s financial statements and the forecast of future revenues and expenses are some of the most valuable management tools that small business owners have at their disposal.

There are several types of financial forecasts that an owner may need to prepare. The purpose of all of them is to show a realistic picture of the firm’s future cash flow. One type of cash flow forecast is those required by prospective lenders. Creditors will look and stress a company’s financials and cash flow forecast, to determine if a business will be able to cover principal and interest payments during the life of a loan. Stressing the cash flows means looking at scenarios where income and expenses are negatively impacted, to determine if the company can still fulfil its obligations in tough economic times.

STEPS IN CREATING A CASHFLOW FORECAST

There are 5 steps in creating a cash flow forecast:

STEP 1: PREPARE A LIST OF ASSUMPTIONS

Forecasts are driven by assumptions and therefore for the forecast to be useful the underlying assumptions must be appropriate to the business.

Assumptions can be based on past performance, industry publications, correspondence from customers and suppliers, etc. and generally include:

- Timing and quantum of price increases – both yours and your suppliers’

- Sales growth estimates

- Impact of seasonality

- Provision for general cost increases (CPI)

- Provision for internal salary and wage increases

Listing the assumptions within the forecast adds credibility serves as a reminder when assessing actual performance against forecast.

STEP 2 PREPARE ANTICIPATED SALES INCOME

Sales can be difficult to predict, and often the best place to start is to look at sales in previous years to identify trends. You can then identify internal (e.g. price increases) and external (e.g. economic) factors likely to impact the current period, and make necessary adjustments.

When you have determined realistic sales for the period, they need to be broken down into sales receipts (i.e. When is the cash expected to be collected from debtors?). There is often a pattern to debtor remittance (e.g. 60% within terms, 25% one month outside terms with the remainder coming in shortly thereafter). Note: this pattern should form one of the forecast’s underlying assumptions.

STEP 3 PREPARE A LIST OF ‘OTHER’ ESTIMATED CASH INFLOWS

To ensure your cash flow forecast is complete, compile a list of all other anticipated cash inflows, for example:

– tax refunds

– Insurance proceeds

– Additional equity contributions or loan proceeds

– Government grants receipts

– Cash from asset divestment

– Royalties or franchise/license fees

STEP 4 PREPARE A LIST OF ESTIMATED EXPENSES

These should include direct and indirect expenses. The key is identifying all the expenses required to operate the business and anticipating the timing of each payment. Cash outflows relating to financing and investing activities should be included, for example:

– Payments to suppliers

– Wages and salaries of all staff

– Purchase of new assets

– Loan repayments

– Director drawings

Bank statements are an easy way of identifying direct debit arrangements.

STEP 5: PUTTING THE INFORMATION TOGETHER

Simply put, a cash flow forecast is a rolling calculation based an opening cash position, adding cash inflows and deducting cash outflows, to arrive at a closing cash position.

Projection Notes

When making projections of items in the cashflow budget, take note of the following:

INCOME – SALES

Income from sales is the most important source of income and the most difficult to estimate. Two of the things you should bear in mind when trying to estimate your monthly sales figures are the age of your business and seasonal variations. If you are a new business you will need time to build up your trade. Your sales forecast should reflect this. It is advisable to begin with low monthly figures i.e. be conservative or ’realistic’. You should separate cash sales and cash from debtors.

STOCK AND RAW MATERIALS

The stock figure should include initial stock purchases and the subsequent replenishment of stock. The stock figure should bear a direct relationship to the sales figures i.e. if you buy an item for R25 and intend to sell it for R50. Then the stock should represent 50% of sales. A distinction needs to be made between your cash purchases and your credit purchases

CAPITAL EQUIPMENT

Make a list of all the equipment required to run your business then obtain prices for all items. Establish what you need to obtain at the outset and what could be bought later on in the year then budget accordingly. Consider the options of obtaining these items by outright purchase, hire purchase, leasing, etc. One advantage of hire purchase and leasing is that the cost can be spread over a specified period and this can aid your cash flow. The interest incurred has to be considered.

VEHICLE COSTS

When estimating your vehicle cost include not only the actual cost of the vehicle, (if on hire, purchased or leased) but also all the other costs e.g. road tax, insurance, repairs, renewals, petrol, etc. If purchased outright, see ’capital allowances’ under taxation.

OPENING BALANCE

This shows how much should be in your business bank account at the start of the month. When starting up you should put the figure of available funding or capital into the cash flow as its ’opening balance’.

CLOSING BALANCE

Work out the closing balance for the month by adding any opening bank balance to the total receipts and deducting from this the total payments figure. The closing bank balance becomes the opening bank balance automatically at the start of the next month.

The closing balance figure for each month is very important: if it’s a minus figure it means you may have to make use of an overdraft facility or plan a sales drive for the months preceding it to avoid ’going into the black’. The cumulative figure tells you whether your bank balance gets bigger or smaller over a period of time and highlights the duration of any borrowing requirements.

Refer to Study Guide for Cashflow template: https://incubateme.biz/wp-content/uploads/2024/11/FMP-FINANCIAL-MANAGEMENT-PROGRAMME-INFO-SHEET-V012024.pdf

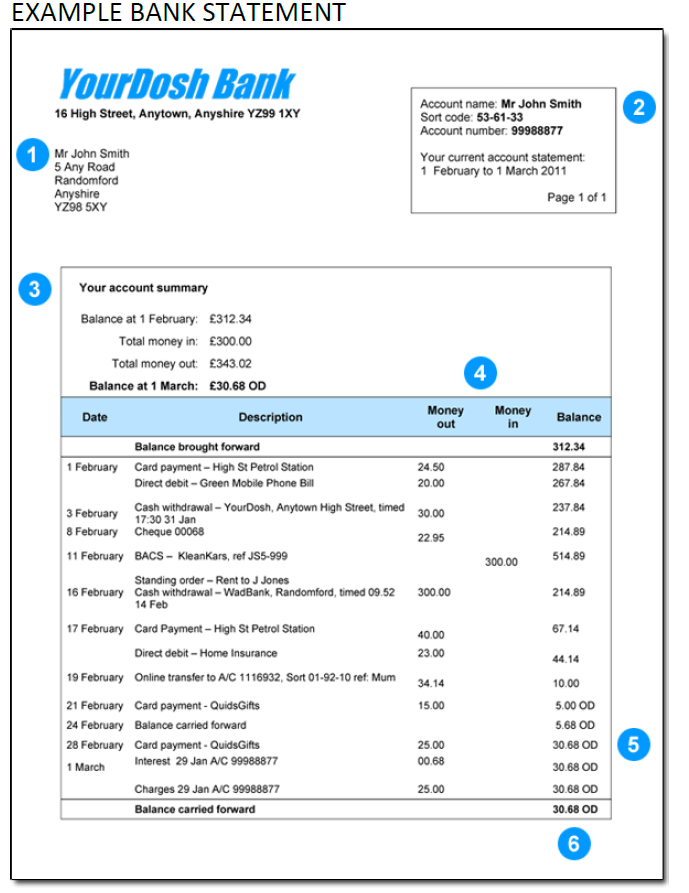

BANK STATEMENTS

The bank statement is a handy way of seeing all your incomings and your outgoings at once. It’s definitely a good idea to open and read your bank statements so you can check you’ve received what you expected, and that you recognise all the payments going out too. We’ll help you to understand how to read and make sense of your bank statement.

Your bank statement might be sent monthly, quarterly or yearly, depending on what type of account you have. Have a look at the table below for a simple explanation:

You’ll probably get your statement through the post, but if you bank online, you can also access it on the internet, and possibly opt out of receiving paper statements.

Your statement will show all the money in and out for your account during the set period (monthly or otherwise).

The details will include the date, amount and an identifier for the payment (such as a shop name for purchases). For benefits, the identifier could be the Department for Work and Pensions, Jobcentre Plus or HM Revenue and Customs, or your local council if it’s housing benefit. Here’s our handy example of a bank statement showing the kinds of things you’ll see. Yours might look a bit different, but the same kind of information will be on there.

EXPLANATION OF CONTENTS

- YOUR PERSONAL INFORMATION

This is your name and permanent home address. Make sure it’s right, and that you haven’t got someone else’s bank statement! It’s really important to tell your bank if you move house, so they can safely and securely send any information about your account to you. - YOUR ACCOUNT INFORMATION

This will show the name you used to open your account with (’account name’), such as ‘Mr John Smith’. It will also show your account number and sort code. Your sort code is a six-digit number with dashes in (for example, 53-61-33) that helps the whole banking system identify which bank and local branch your account’s based at. - STATEMENT SUMMARY

You’ll be shown a basic account summary, which will usually show the total amounts paid in and out during that month (or other period if it’s a savings account). You can also see here that there’s a closing balance – this means the balance of your account at the time the statement was sent out. - MONTHLY INCOMINGS AND OUTGOINGS

On your statement there will be two columns showing money paid into your account (credits) and one for money paid out (debits). Your statement will be ordered by date, so it’ll show the oldest payments at the top, working down to the most recent. Next to each payment is also a description, which shows where you were when you made the payment (a shop or cash machine) or who you paid. There might also be standing orders or direct debits you’ve arranged. This information should also be available for the ‘money in’ section – it might say ‘bank transfer’ for your wages, ‘counter credit’ for cash or cheques you’ve paid in at your branch, refunds from shops, or automated payments made by the state to you, such as benefits.

Sometimes payments will show up on your statement a few days after you actually made them. For example, if you buy something with your debit card in a shop (or withdraw cash from a machine), it might not show up on your statement for a few days. This is because it takes time for payments to go through the banking system, especially over a weekend. When this happens, the actual date you made the purchase or cash withdrawal should be shown in the ‘description’ column. In the far right column, you can see a running total, the ‘balance’. This means the total you have in your account each day, as a result of money in and out of your account. - GOING OVERDRAWN

In your balance column, sometimes you’ll see the letters OD or a minus sign next to the figure. This means your account’s gone overdrawn and you’ve spent more money than you had in your account. So, if you had R10.00 in your account, but buy something on your debit card for R15.00, you’ll go overdrawn by R5 (R10-R15=-R5). You’ll have to pay this back to the bank, along with any interest and charges unless you have an interest-free overdraft. The longer you leave it to pay pack your overdraft, the longer you’ll be charged interest on it, and the harder you may find it to get out of your overdraft.

That’s why it’s really important not to become reliant on your overdraft it costs you more money in the long-term to borrow from the bank like this. It’s a good idea to do all you can to stay in ‘the black’ (plus numbers) and get out of ‘the red’ (minus numbers). It could be a spiral into debt, so make sure you’re not always right at the limit of your overdraft - BANK CHARGES

If your account’s gone overdrawn beyond your agreed limit, or you didn’t have an agreed overdraft, the bank will charge you for ‘unarranged borrowing’. They can also charge you if you pay in a cheque that bounces (that’s when the other person doesn’t have enough in their account to cover the amount they wrote the cheque for). Banks have to notify you before they take any money from your account for these charges.

APPLY AN ACCOUNTING SYSTEM TO MANAGE A NEW VENTURE.

In all activities (whether business activities or non-business activities) and in all organisations (whether business organisations like a manufacturing entity or trading entity or non-business organisations like schools, colleges, hospitals, libraries, clubs, churches, political parties) which require money and other economic resources, accounting is required to account for these resources. In other words, wherever money is involved, accounting is required to account for it. Accounting is often called the language of business. The basic function of any language is to serve as a means of communication. Accounting also serves this function.

DEFINITION OF ACCOUNTING

Accounting, as an information system is the process of identifying, measuring and communicating the economic information of an organisation to its users who need the information for decision making. It identifies transactions and events of a specific entity. A transaction is an exchange in which each participant receives or sacrifices value (e.g. purchase of raw material). An event (whether internal or external) is a happening of consequence to an entity (e.g. use of raw material for production). An entity means an economic unit that performs economic activities.

ACCOUNTING SYSTEM

An accounting system is an organized set of manual and computerized accounting methods, procedures and controls established to gather, record, classify, analyze, summarize, interpret, and present accurate and timely financial data for management decisions.

COMPONENTS OF THE ACCOUNTING SYSTEM

Think of the accounting system as a wheel whose hub is the general ledger (G/L). Feeding the hub information are the spokes of the wheel. These include;

- Accounts receivable

- Accounts payable

- Order entry

- Inventory control

- Cost accounting

- Payroll

- Fixed assets accounting

These modules are ledgers themselves. We call them sub ledgers. Each contains the detailed entries of its specific field, such as accounts receivable. The sub ledgers summarize the entries, then send the summary up to the general ledger. For example, each day the receivables sub ledger records all credit sales and payments received. The transactions net together then go up to the G/L to increase or decrease A/R, increase cash and decrease inventory.

We’ll always check to be sure that the balance of the sub ledger exactly equals the account balance for that sub ledger account in the G/L. If it doesn’t, then there’s a problem.

DIFFERENCES BETWEEN MANUAL AND AUTOMATED LEDGERS

Think of the G/L as a sheet of paper on which transactions from all four categories of accounts-assets, liabilities, income, and expenses-are recorded. Some of them flow up from various sub ledgers, and some are entered directly into the G/L through a general journal entry. An example of such a direct entry would be the payment on a loan.

The same concept of a sheet of paper holds for each sub ledger that feeds the general ledger. A computerized accounting system works the same way, except that the general ledger and sub ledgers are computer files instead of sheets of paper. Entries are posted to each and summarized, then the summary is sent up to the G/L for posting

SETTING-UP A NEW VENTURE ACCOUNTING SYSTEM

Many small business owners (including myself) tend to focus on the more glamorous aspects of their business like sales and marketing and product/service development. As a result, accounting (poor misunderstood accounting) does not get the attention it deserves. In addition to the perception that an accounting system does not necessarily add value, they can also be a little intimidating. However, setting up an accounting system does not have to be complicated and should be considered essential for any small business or self-employed owner. The following are the steps in setting an accounting system;

STEP 1: PICK AN ACCOUNTING METHOD:

The first decision to be made is which type of accounting method to choose, there are 2 choices:

The Cash Method (or Cash Basis) — this means that you count income when you actually receive it (either as cash, credit card charges or check) and your expenses are counted when you actually pay them. This is the most common method for small businesses, especially those that take immediate payment for a product or service (credit card, check, cash, etc.) The Accrual Method (or Accrual Basis) – this means that you count income when a sale is made (regardless if you actually receive the money for it) and expenses are counted when you actually receive the good or service (instead of paying for it immediately). This method is common for larger businesses or small businesses that utilize “invoicing” and frequently deliver a product or service before being paid for it.

NOTE: The accrual method is generally considered to give you a more accurate picture of your company’s financial situation but requires you to take extra steps like maintaining accounts receivable and accounts payable records. The cash method is generally easier to maintain and is the preferred method for small businesses

STEP 2: DECIDE WHICH BOOKKEEPING SYSTEM TO USE:

After you have chosen your accounting method, you will want to decide which bookkeeping system will be right for your new venture. There are two choices.

I. Single entry bookkeeping – Similar to your check register. You just add the money coming in and subtract the money going out and keep a running balance.

II. Double entry bookkeeping – Tracks your income and expenses AND your assets and liabilities. Assets and liabilities are captured on the balance sheet.

STEP 3: CHOOSE A METHOD FOR RECORDING TRANSACTIONS:

After you’ve decided on an accounting method, the next step is to decide how you are going to record transactions. You have basically 2 choices:

– Hand-Recording Transactions — you actually hand-write each transaction in a ledger.

– Software — you enter transactions in a software program which then automates many routine tasks.

By far the most popular method is software. There are dozens of accounting software packages and most of them will help you maintain your books as well as automate things like payroll and reports.

STEP 4: CREATE TEMPLATES

Create your purchase order and invoice templates. Accounting software users will find templates within the software program. Spreadsheet users can download a variety of templates from the software manufacturer. Invoices should include the date, business information, customer information, amount due, payment terms or due date and a description of the services or goods provided. Begin using purchase orders for your purchases and invoices to record customer sales.

STEP 5: CREATE A FILING SYSTEM

– Use file folders and labels to organize financial documents

– Maintain bank statements, customer invoices, vendor bills, government assessments etc. in separate files

– Investing in colour coded file folders can greatly facilitate file retrieval

– File regularly to avoid scrambling at the end of the year

– Maintain separate folders for outstanding invoices, bills and other documents which require follow up.

STEP 6: OPEN A BUSINESS BANK ACCOUNT

Very important: Open a separate bank account for your small business. Do not pay your personal expenses out of this account. If you need money from your business for personal expenses write yourself a check or transfer the money into your personal bank account.

STEP 7: ORGANISE THE ACCOUNTING DEPARTMENT

Organize your small-business accounting system by function. Often there’s just one person there to do all the transaction entries. From an internal control standpoint, this isn’t desirable. Having too few people doing all the accounting opens the door for fraud and embezzlement. Companies with more people assign functions in such a way that those done by the same person don’t pose a control threat.

Having the same person draft the checks and reconcile the checking account is a good example of how not to assign accounting duties. We’ll talk extensively about internal control later. However, for now, small businesses often can’t afford the number of people needed for an adequate separation of duties. The internal control structure that we’ll install in your new accounting system helps mitigate that risk through mechanics and procedures rather than expensive people.

NOTE: In many cases the same person will do many of these things. However, these are the areas we’ll be dealing with in setting up the accounting system. The person you assign to be in overall charge of the system should be the one who is most familiar with accounting. If you are just starting your company, you might want to think about the background of some of your new employees. At least one should have the capacity to run the accounting system.

MONITORING THE ACCOUNTING SYSTEM

Once you’ve chosen your accounting system, the next step is learning and maintaining your accounting system. Learning the system will obviously depend on what solution you’ve adopted, but maintaining the system is accomplished primarily by 2 things:

You Have to Use the System: once you’ve taken the time and energy to setup an accounting system, you have to actually utilize it properly. This means entering every transaction, check, bill, charge or refund.

Reconcile Your Bank Statement: the best way to maintain your accounting system is by reconciling your bank statement with your accounting system every month. This means that you compare each transaction from your bank account or accounts with your accounting system and make sure that they balance. This process alone will force you to properly account for the company’s money.

TAXATION REQUIREMENTS

SARS is obligated by law to determine and collect from each taxpayer only the correct amount of tax that is due to the Government. The SARS offices are the representatives of the Commissioner and in that capacity must ensure that the tax laws are administered correctly and fairly so that no one is favoured or prejudiced above the rest.

REGISTRATION

As soon as you commence your business (whether as a sole proprietor, partner or any other form), you are required to register with your local SARS office in order to obtain an income tax reference number.

FILING

A company/close corporation on the other hand is permitted to have a tax year ending on a date that coincides with its financial year. If the financial year-end is 30 June, its tax year or year of assessment will run from 1 July to 30 June. Income tax returns must be submitted manually or electronically by a specific date each year.

FORMS OF TAXES

The following are the main forms of taxation.

EMPLOYEES’ TAX (PAYE)

Employees’ tax is a system in terms of which an employer, as an agent of government, deducts income tax from the earnings of employees and pays it over to SARS on a monthly basis. Once registered, the employer will receive a monthly return (EMP 201) that must be completed and submitted together with the deducted employees’ tax within seven days of the month following the month for which the tax was withheld.

INCOME TAX

A sole proprietor or each partner is subject to income tax on his/her taxable income. Income tax is levied at progressive rates ranging from 18% to 40%. For the 2009 tax year, the maximum marginal rate of 40% applies where the taxable income exceeds R490 000. Unlike individuals, a company or CC pays income tax at a flat rate of 28% (except in the case of SBCs) on its taxable income for the tax year and 2210% secondary tax on companies (STC) on the net amount of dividends declared.

VALUE-ADDED TAX (VAT)

Value-Added Tax (VAT) is an indirect tax based on consumption of goods and services in the economy. Revenue is raised for the government by requiring certain traders or vendors to register and to charge VAT on taxable supplies of goods or services.

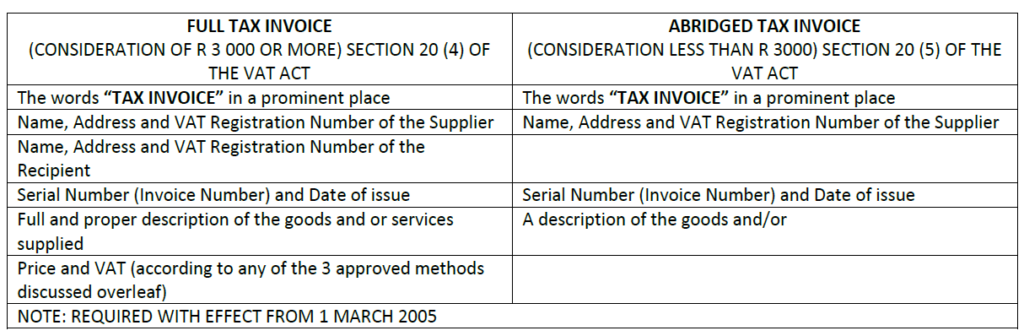

The most important document in such a system is the tax invoice. Without a proper tax invoice, you cannot deduct input tax on purchases for your enterprise, and if you have clients who are vendors or if you sell goods to foreign tourists, they cannot claim back the VAT that you have charged them, or claim a refund of the VAT when taking the goods out of the country.

The following information must be reflected on a tax invoice for it to be considered valid:

The following important points should also be noted with regard to tax invoices:

– A vendor is required to issue a tax invoice to the recipient within 21 days of the supply having been made where the consideration for the supply exceeds R50 (whether the recipient has requested this or not);

– If the consideration in money for the supply is R50 or less, a tax invoice is not required (however, a document such as a till slip or sales docket will still be required to verify the input tax claimed);

– Where the consideration for a taxable supply exceeds R50 but does not exceed R3 000, an abridged tax invoice may be issued (see example above);

– A tax invoice must be in South African currency, except for a zero-rated supply (e.g. goods exported). In such cases, a full tax invoice must be issued, even if the consideration is less than R3 000;

– A tax invoice is not issued by a debtor (vendor) under an installment credit agreement if the goods are repossessed. This will be done by the person exercising their right of repossession (i.e. the bank or other financier);

– It is a requirement to reflect the VAT registration number of the recipient of the supply on the tax invoice with effect from 1 March 2005 (if that person is a vendor) and the consideration for the supply exceeds R3 000;

-If a vendor fails to deduct input tax in respect of a particular tax period, it may be deducted in a later tax period, but limited to a period of 5 years from the date that the supply concerned was made.

ANALYSE AN INCOME AND EXPENDITURE STATEMENT.

Understanding financial statements is essential to the success of a small business. Financial statements can be used as a roadmap on your business journey to economic success. Using numbers as navigation aids can steer you in the right direction and help you avoid costly “breakdowns.”

IMPORTANCE OF FINANCIAL STATEMENTS

Many business experts and accountants recommend that you prepare financial statements monthly; quarterly at a minimum. Some companies prepare them at least once a week, sometimes daily, to stay abreast of results. The more frequently a company prepares their financial statements, the sooner timely decisions can be made.

TYPES OF FINANCIAL STATEMENTS

There are four types of financial statements; compiled, reviewed, audited, and unaudited:

A compiled statement contains financial data from a company reported in a financial statement format by a certified public accountant (CPA); it does not include any analysis of the statement.

The reviewed statement includes an analysis of the statement by a CPA in which unusual items or trends in the financial statement are explained.

An audited statement (also prepared by a CPA) contains any analysis which includes confirmation with outside parties, physical inspection and observation, and transactions traced to supporting documents. An audited statement offers the highest level of accuracy.

An unaudited statement applies to a financial statement prepared by the company which has not been compiled, reviewed, or audited by an outside CPA.

Small business owners must be aware that they may be required to submit financial statements in nine circumstances:

- Virtually all suppliers of capital, such as banks, finance companies, and venture capitalists, require these reports with each loan request, regardless of previous successful loan history. Banks may need CPA compiled or reviewed statements and, in some cases, audited statements. They may not accept company or individually prepared financial statements, unless they are backed by personal or corporate income. Typically, as a condition of granting a loan, a creditor may request periodic financial statements in order to monitor the success of the business and spot any possible repayment problems.

- Information from financial statements is necessary to prepare federal and state income tax returns.

- Statements themselves need not be filed.

- Prospective buyers of a business will ask to inspect financial statements and the financial/operational trends they reveal before they will negotiate a sale price and commit to the purchase.

- In the event that claims for losses are submitted to insurance companies, accounting records (particularly the Balance Sheet) are necessary to substantiate the original value of fixed assets.

- If business disputes develop, financial statements may be valuable to prove the nature and extent of any loss. Should litigation occur, lack of such statements may hamper preparation of the case.

- Whenever an audit is required–for example by owners or creditors–four statements must be prepared: a Balance Sheet (or Statement of Financial Position), Reconcilement of Equity (or Statement of Stockholder’s Equity for corporations), Income Statement (or Statement of Earnings), and Statement of Cash Flows.

- A number of states require corporations to furnish shareholders with annual statements. Certain corporations, whose stock is closely held, that is, owned by a small number of shareholders, are exempt.

- In instances where the sale of stock or other securities must be approved by a state corporation or securities agency, the agency usually requires financial statements.

INCOME AND EXPENDITURE STATEMENT

An income statement, otherwise known as a profit and loss statement, is a summary of a company’s profit or loss during any one given period of time, such as a month, three months, or one year. The income statement records all revenues for a business during this given period, as well as the operating expenses for the business.

KEY TERMS IN INCOME AND EXPENDITURE

INCOME

For the purpose of this module, income is defined as money that has been made within the time period of the statement. It is an important accounting concept to correctly account for income within appropriate time period of the financial statement. This means that you should include your income figure in the month where it belongs even if money has not been received.

For example, if you are a trader and sold goods to your customers on credit for R1000 as at 20 September 2010. In addition, as per the credit terms you agreed that the customer shall pay 6 months later.

Since a sales transaction has taken place, the income of R1 000 must be recorded as income in September even if the money will be received in another month.

EXPENDITURE

For the purpose of this module, expenditure is defined as the costs that have been incurred within the time period of the statement. As with the concept of income, you should include expenditure in the period in which it was incurred even if no money was paid. This ensures that you have an accurate statement of income and expenditure of real expenditures incurred within the period.

For example, you were doing a household income and expenditure statement for end of September 2010 and you have not received the electricity bill nor paid it for September, you should nonetheless include it (or a reasonable estimate) in the income and expenditure statement for September.

PROFIT OR LOSS

At the end of the income and expenditure statement, you should subtract Expenditure from income remaining with a proportion which enterprises call a profit or loss. If the income items are more than the expenditure items we call that profit but if the expenditures and more than the income, then the difference is known as loss.

PURPOSE OF INCOME AND EXPENDITURE STATEMENT

The following are some of the purposes of an income and expenditure statement;

– To clearly show how much money was made and how much was spent within a given time period

– To know how much profit or loss has been earned within a given financial period.

– Helps to pinpoint items that are causing unexpected expenditures.

– If you compare income & expenditure statement for different consecutive periods the enterprise can deduce whether the income is rising or stagnating.

Legislation requires that when doing financial statements of a company, certain specific requirements regarding the disclosure of information must be met. According to Companies Act 61 of 1973 a company’s financial statements have to be drawn up in accordance with Generally Accepted Accounting Practice (GAAP).

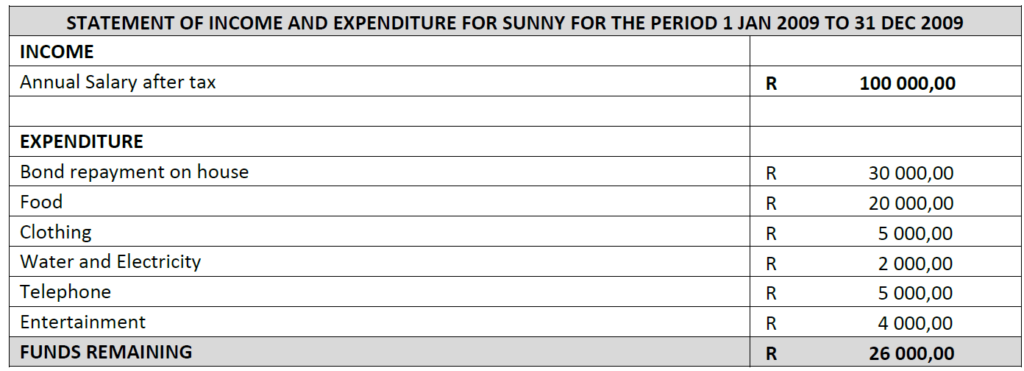

CASE STUDY 1: THE INCOME AND EXPENDITURE STATEMENT OF A PRIVATE INDIVIDUAL

Thando is a private individual who works in an office as a consultant. She wishes to obtain a loan from FBC Bank to finance the purchase of a new car. Big Sharks has requested that Thando produce an income and expenditure Statement to demonstrate to them that she has income necessary to meet the repayments of loan which amount to R1000 per month.

Thando has drawn up the following statement:

From this statement, FBC Bank can easily see that Thando has sufficient money left over after her expenses have been deducted to meet the loan repayments of (12 X R 1000= 12 000 per annum)

Normally an individual is only required to produce a statement like this either for, as in the case study, a bank loan or sometimes when completing a tax return. There is no requirement for an individual to produce the statement on an annual basis as required for companies by Companies Act 1973.

It is, however, a good personal management tool and wise person would compile such a statement and keep a good eye on it on a regular basis.

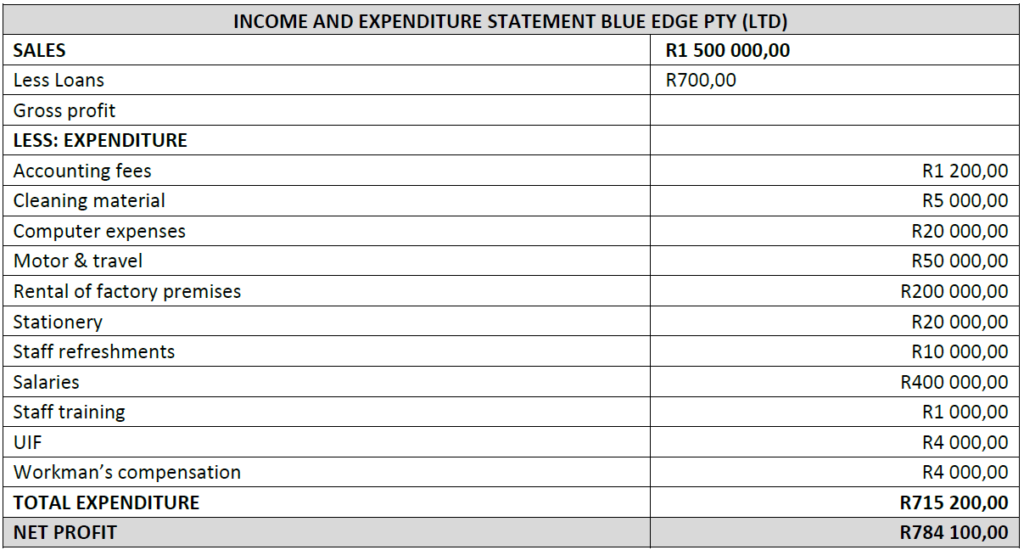

CASE STUDY 2: THE INCOME AND EXPENDITURE STATEMENT OF A COMPANY BLUE EDGE

Blue Edge LTD produces the chemical flavours used to flavour cakes. They have been in operation since 1940 and continue to run as family owned private business. Because they are incorporated as a company, they are required to produce client’s Annual financial statements. Interested parties, such as the owners of the company, clients and suppliers who do business, with them and SARS (The receiver of Revenue) may review these financial statements and make decisions on the results accordingly.

The accountant for Blue Edge LTD is responsible for ensuring that the figures contained in the Statement of Income and Expenditure are accurate and reflect a true position of the finances of the company. The Accountant must also produce these financial statements annually after the year end (which in Blue Edge case is the 31 October).

SOURCES OF INCOME AND EXPENDITURE

Income and expenditure sources are as varied as the types of industries and business in operation. People too, derive their income and spend their money in all possible ways. The ways of income are many and varied; it is your task to identify these in the financial statements and be able to differentiate between the income and the costs

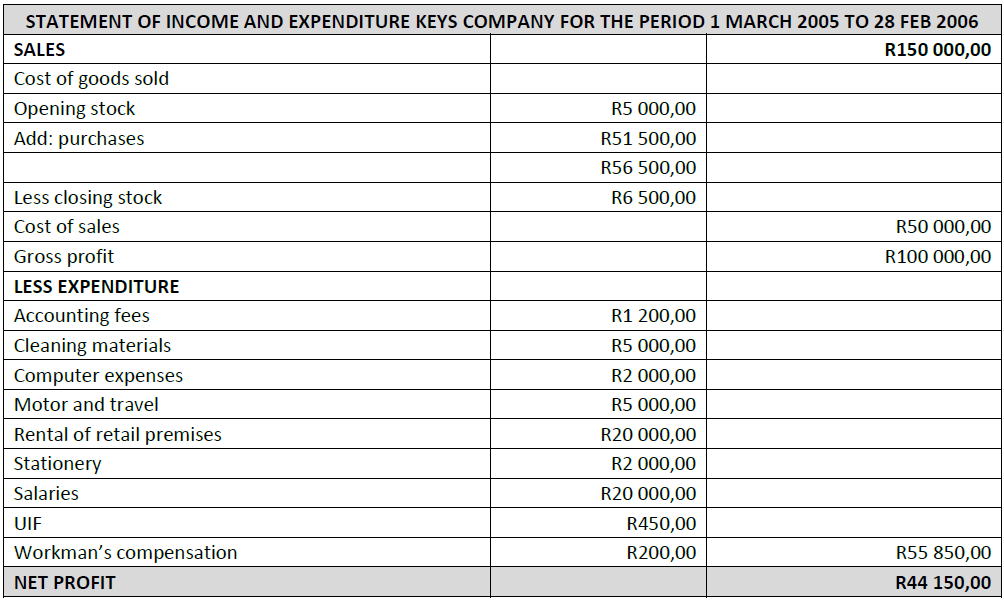

CASE STUDY 3: KEYS COMPANY

Keys Company has a shop in a shopping mall. They sell toys, educational devices, and children’s party tricks. Keys the owner, has had the following statement of income and expenditure prepared for tax purposes.

In case study above, expenditure incurred in generating sales include the purchases of goods for sale, called purchases. Note that purchases in accounting terms have a specific meaning: it means the cost incurred in acquiring goods for resale. It does not include other costs, such as the ones listed in the Expenditure section. These must be disclosed separately.

The cost of sales calculation, which is opening stock plus Purchases less closing stock, is calculated and subtracted from sales to give Gross profit. Gross profit is an indication of the profitability of operations, not including other expenses and overheads.

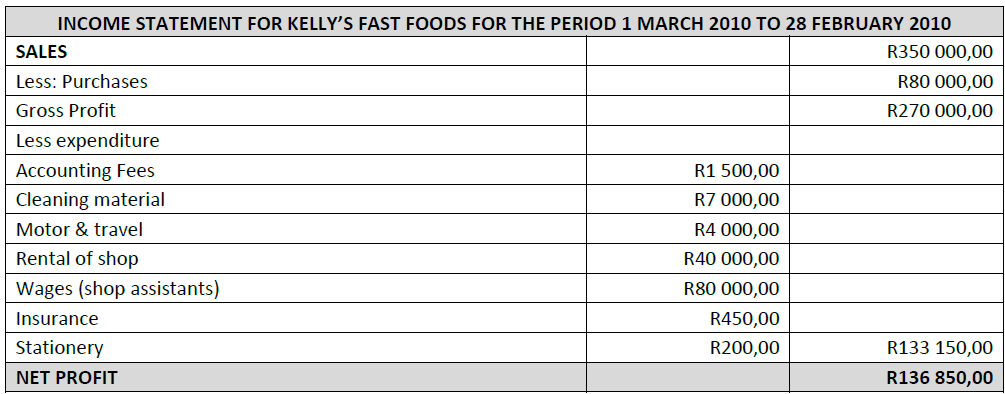

CASE STUDY 4 KELLY’S FAST FOOD

Kelly’s Fast foods is a vendor of pies, chicken, cold drinks, fish, chips, coffee and sandwiches. They cater for break fast and lunch time crowd in a nearby office park.

Below is Kelly’s Fast Foods Income statement prepared by the accountant for tax purposes. Now, identity the sources of income and expenditure for Kelly Fast Food.

ASSESSING FINANCIAL VIABILITY

The concept of going concern is an important accounting concept. Financial statements are usually prepared with the assumption that the enterprise is going concern, without evidence to the contrary. This assumption implies that the business will continue its operations.

Financial viability entails that:

– The concern will continue its operations in the foreseeable future.

– The enterprise is sufficiently profitable (or will be in the future) to continue its operations.

– There is inherent worth in continuing operations. This related to the concept of going profits. It is important to note that sometimes companies do not make a profit every year- especially in first few years of operations.

A businessperson would examine financial statements for their financial viability and also take a view on inherent worth. A full assessment or analysis of a company does not just look at one year in isolation: many years of operational results need to be examined for fundamental analysis.

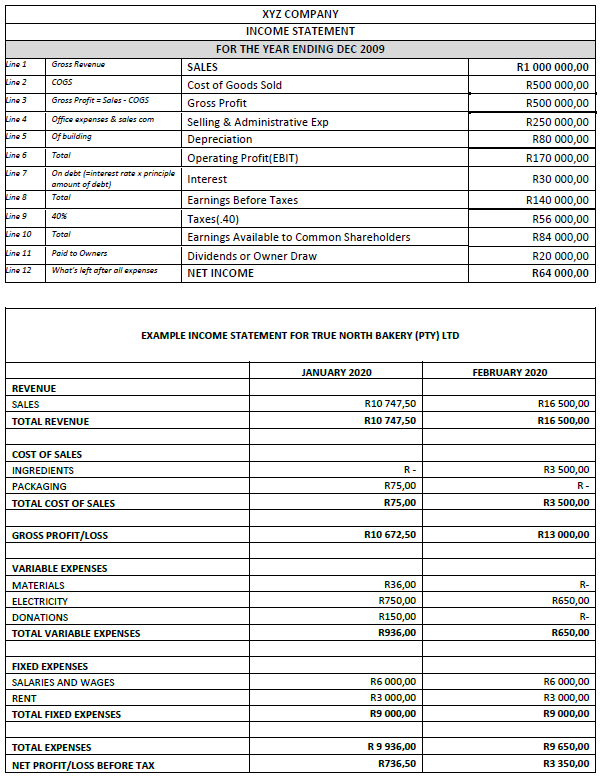

PREPARATION OF INCOME AND EXPENDITURE STATEMENTS

The income statement next page is presented step-by-step so we can look at the profit or loss after each expense is deducted.

Line 1 is the gross revenue or sales figure. This is the total of amount of sales in dollars that the firm has made in 2009.

Line 2 is a R500,000 entry for cost of goods sold. This is the cost specifically associated with units of your product sold. Cost of goods sold is usually your largest expense. Subtract cost of goods sold from gross sales to get gross profit (Line 3). After you get gross profit, you then subtract all of your other expenses from this number in order to generate your net profit.

From the R500,000 gross profit, the next expense you subtract is selling and administration expenses (Line 4). This R250,000 item represents your office expenses and sales commissions.

An important item that will merit more discussion is depreciation expense (Line 5). When you buy a building for your business or equipment, you depreciate it over a period of time. Depreciation is a non-cash expense and serves as a tax shelter so it is shown on the income statement. After subtracting out selling and administrative expenses and depreciation, you arrive at your operating profit (Line 6). Operating profit is also called earnings before interest and taxes (EBIT), which in this case is R170,000.

After you calculate EBIT, the next step is to calculate interest expense. Interest is what you pay on any debt your company has. In order to calculate the interest on debt, you have to know the interest rate you are paying and multiply it by the principal amount of your debt. For this example, the interest amount is assumed at R30,000 and is stated on Line 7.

After subtracting your interest expense from EBIT, you get earnings before taxes on Line 8. Then, you fill in the amount you pay in federal, state, local, and payroll taxes on Line 9. The tax rate, in this example, is 40%. After you subtract that expense, you are finally at the earnings available to your common shareholders, which is stated on Line 10.

If you have investors in your firm or if you take a salary from your firm, Line 11 is where you record the draw or the dividends. Line 12, then, is the firm’s net income or what you have left to plow back, or reinvest, into the firm in the form of retained earnings.

This is an example of a very simple income statement. The income statement of your company may be a little more complex and contain more line items. This statement should serve to give you the general idea of how a profit/loss statement, or income statement, works.

ANALYSE A BALANCE SHEET

A Balance Sheet is a ‘snapshot’ of the financial position of the school at a specific point in time, usually the end of an accounting period. This report lists assets and liabilities as current or non-current, as well as the organisation’s equity.

PURPOSE OF A BALANCE SHEET

The purpose of a balance sheet is to reflect the financial position of a company or enterprise at a point in time. It is different from a statement of income & expenditure in that the balance sheet is as at a specific date, whereas the income statement is for a period of time. Usually, the income statement will cover, say, a financial year, and the corresponding balance will reflect the financial position on the last day of the year under review.

REQUIREMENTS FOR PREPARING BALANCE SHEETS

- As part of Annual Financial Statements, companies are required to produce Balance Sheets every year.

- Individuals need not prepare balance sheet unless requested to do so by a bank or Receiver of Revenue.

ELEMENTS OF BALANCE SHEET

A balance sheet is separated into two distinct parts:

I. Capital employed section

II. Employment of capital

Based on the basic accounting equation:

TOTAL ASSETS = TOTAL LIABILITIES + OWNERS EQUITY

The two sections of the balance sheet reflect the calculation of the equation.

I. CAPITAL EMPLOYED SECTION

This section reflects the money the owner has put into the business. This side consists of the share capital of the business (if it is a company: certain forms of trading operations such as sole traders or partnerships, do not have share capital, but reflect the investment of the traders/partners).

SHARE CAPITAL

This is the equity of the business. Usually, a company is incorporated with an authorised share capital that is divided amongst the owners of the business. These shares, as in publicly traded companies on the stock exchange, are tradable in certain circumstances and can be bought and sold. They reflect the division of ownership and profit sharing.

If you own shares in a company, you are entitled to a share of profits in relation to the amount of shares that you hold. Often, companies pay these profits to shareholders in the form of dividends. But, a company is not legally forced to pay dividends.

II. EMPLOYMENT OF CAPITAL SECTION

The term “employment of capital” means what has been done with the money that the owners of the business have invested in the operations. This is the calculation of net Asset less Liabilities. A primary feature of a balance sheet, as indicated in the name of the statement, is that it MUST balance. If a balance sheet does not balance, it is not a balance sheet.

NOTES TO THE BALANCE SHEET

In terms of disclosure as required in the Companies Act 61 of 1973, there are many items that are disclosed in company’s Annual Financial Statements. Often, how the figures that appear on the balance sheet are arrived at are shown in Notes to the Balance sheet. An example of common note would be the calculation of depreciation for Fixed Assets.

THE ANALYSIS OF A BALANCE SHEET

Balance sheets are invaluable tools for analysis of companies’ net worth. By understanding and interpreting the clues within the balance sheet, the analyst can evaluate the value of the company, and make decisions accordingly.

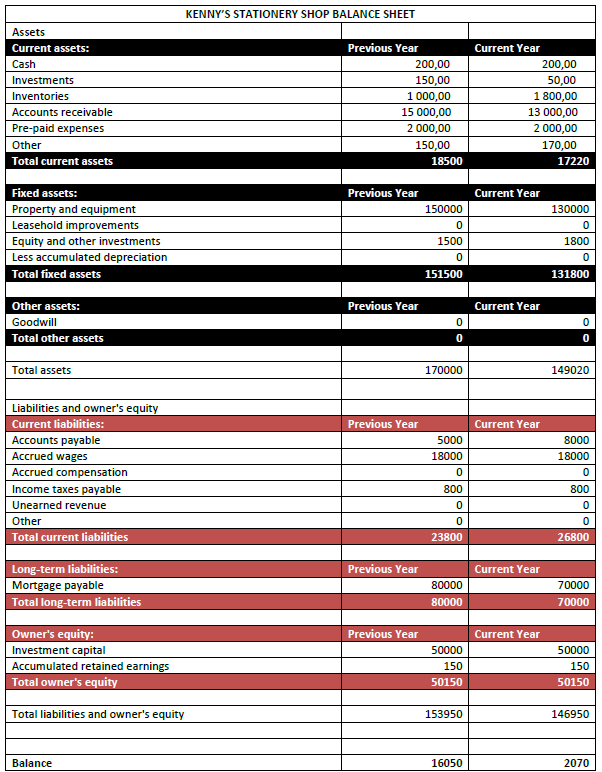

Case study Kenny’s Stationery Shop

The company is incorporated as a close corporation and has been trading for 8 years. The accountant has compiled the annual financial statements, which contains the following balance sheet.

QUESTION: HOW MUCH IS THE COMPANY WORTH??

CONCEPT OF AN ASSET

Assets are things that the business owns. The types include;

FIXED ASSETS

Fixed Assets, which are things, used in the production of income and they last longer than 3 months in the business, like office furniture, motor vehicles, Land, buildings, machinery and tools. Fixed Assets can either be physical assets or nonphysical and they are subject to depreciation (wear and tear). That is, things like patents, copy rights, goodwill are also regarded as assets. More so, fixed assets include both movable.

FIXED ASSETS DOES NOT MEAN THE ASSET DOES NOT MOVE!!

CURRENT ASSETS

The other type being Current Assets which are assets (things owned) that can be converted into cash quickly within a period of say 3 months. Examples include Debtors, cash at bank, trading stock, and Bank balance. Current Assets last less than 3 months meaning they can change forms in that time period. For instance, a Debtor can change to Cash when the debtor pays.

REMEMBER CURRENT ASSETS ARE NOT SUBJECT TO DEPRECIATION

THE CONCEPT OF LIABILITY

Liabilities are amounts that the company owes to other people or companies. These take two forms.

CURRENT LIABILITIES

These are amounts owing to others that must be repaid in a period of three months. Examples include bank overdraft, creditors, and short-term loans.

LONG-TERM LIABILITIES

These are debts that the company has incurred and they are expected to be paid off in a time period more than even a year. If you check the balance sheet section, they are included under the Capital employed section. Examples include bonds, debentures.

PREPARATION OF THE BALANCE SHEET

The process of preparing a Balance Sheet hinges on the ability to classify Trail Balance items into Assets, Liabilities and Capital. Let’s look at the following worked example:

MAKE A FINANCIAL DECISION BASED ON FINANCIAL STATEMENTS

All of us have to make decisions every day. Some decisions are relatively straightforward and simple: Is this report ready to send to my boss now? Others are quite complex: Which of these candidates should I select for the job? Simple decisions usually need a simple decision-making process.

ISSUES IN DECISION MAKING

Difficult decisions typically involve issues like these:

Uncertainty – Many facts may not be known.

Complexity – You have to consider many interrelated factors.

High-risk consequences – The impact of the decision may be significant.

Alternatives – Each has its own set of uncertainties and consequences.

Interpersonal issues – It can be difficult to predict how other people will react.

With these difficulties in mind, the best way to make a complex decision is to use an effective process. Clear processes usually lead to consistent, high-quality results, and they can improve the quality of almost everything we do. In this module, we outline a process that will help improve the quality of your decisions.

A SYSTEMATIC APPROACH TO DECISION MAKING

A logical and systematic decision-making process helps you address the critical elements that result in a good decision. By taking an organized approach, you’re less likely to miss important factors, and you can build on the approach to make your decisions better and better.

There are six steps to making an effective decision:

- Create a constructive environment.

- Generate good alternatives.

- Explore these alternatives.

- Choose the best alternative.

- Check your decision.

- Communicate your decision, and take action.

HERE ARE THE STEPS IN DETAIL:

STEP 1: CREATE A CONSTRUCTIVE ENVIRONMENT

To create a constructive environment for successful decision making, make sure you do the following:

Establish the objective – Define what you want to achieve.

Agree on the process – Know how the final decision will be made, including whether it will be an individual or a team-based decision.

Involve the right people – Stakeholder Analysis is important in making an effective decision, and you’ll want to ensure that you’ve consulted stakeholders appropriately even if you’re making an individual decision. Where a group process is appropriate, the decision-making group – typically a team of five to seven people – should have a good representation of stakeholders.

Allow opinions to be heard – Encourage participants to contribute to the discussions, debates, and analysis without any fear of rejection from the group. This is one of the best ways to avoid groupthink. The Stepladder Technique is a useful method for gradually introducing more and more people to the group discussion, and making sure everyone is heard. Also, recognize that the objective is to make the best decision under the circumstances: it’s not a game in which people are competing to have their own preferred alternatives adopted.

Make sure you’re asking the right question – Ask yourself whether this is really the true issue. The 5 Whys technique is a classic tool that helps you identify the real underlying problem that you face.

Use creativity tools from the start – The basis of creativity is thinking from a different perspective. Do this when you first set out the problem, and then continue it while generating alternatives.

STEP 2: GENERATE GOOD ALTERNATIVES

This step is still critical to making an effective decision. The better options you consider, the more comprehensive your final decision will be. When you generate alternatives, you force yourself to dig deeper, and look at the problem from different angles. If you use the mind-set ‘there must be other solutions out there,’ you’re more likely to make the best decision possible. If you don’t have reasonable alternatives, then there’s really not much of a decision to make!

STEP 3: EXPLORE THE ALTERNATIVES

When you’re satisfied that you have a good selection of realistic alternatives, then you’ll need to evaluate the feasibility, risks, and implications of each choice. Here, we discuss some of the most popular and effective analytical tools.

Risk: In decision making, there’s usually some degree of uncertainty, which inevitably leads to risk. By evaluating the risk involved with various options, you can determine whether the risk is manageable.

– Impact Analysis is a useful technique for brainstorming the ‘unexpected’ consequences that may arise from a decision.

– Cost-Benefit Analysis looks at the financial feasibility of an alternative.

STEP 5: CHECK YOUR DECISION

With all of the effort and hard work that goes into evaluating alternatives, and deciding the best way forward, it’s easy to forget to ‘sense check’ your decisions. This is where you look at the decision you’re about to make dispassionately, to make sure that your process has been thorough, and to ensure that common errors haven’t crept into the decision-making process. After all, we can all now see the catastrophic consequences that over-confidence, groupthink, and other decision-making errors have wrought on the world economy.

STEP 6: COMMUNICATE YOUR DECISION, AND MOVE TO ACTION!

Once you’ve made your decision, it’s important to explain it to those affected by it, and involved in implementing it. Talk about why you chose the alternative you did. The more information you provide about risks and projected benefits; the more likely people are to support the decision.

FINANCIAL RATIOS

A financial ratio is a relationship that indicates something about a company’s activities, such as the ratio between the company’s current assets and its current liabilities or between its debtors and its turnover.

The basic source of these ratios is the company’s profit & loss account and balance sheet that contain all kinds of important information about that company. The ratios really help to bring those details to light and identify the financial strengths and weaknesses of the company.

When assessing ratios, it is important that the results are compared with other companies in the same industry and not to be taken in isolation. What may seem like a poor ratio at first glance may well be normal for that industry and, of course, the reverse applies, in that what may seem a good ratio on its own, could be below average for that industry.

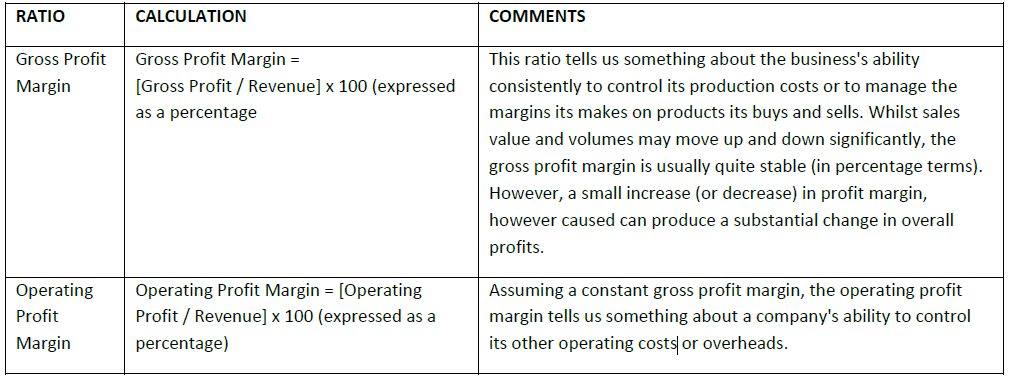

PROFITABILITY RATIOS

These ratios tell us whether a business is making profits – and if so whether at an acceptable rate. The key ratios are:

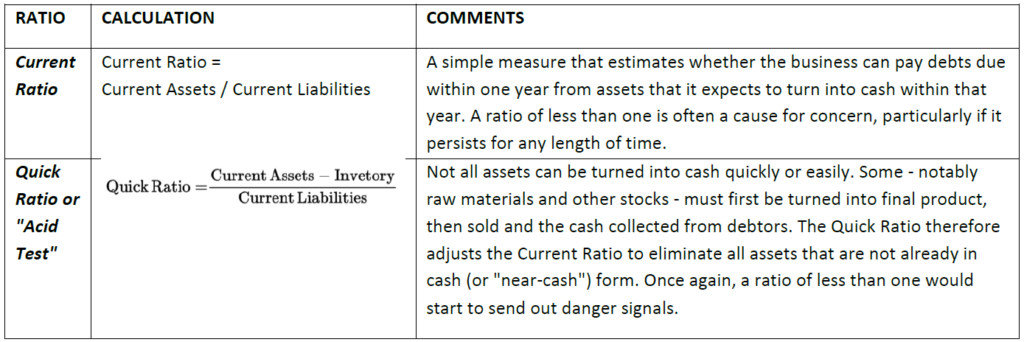

LIQUIDITY RATIOS

Liquidity ratios indicate how capable a business is of meeting its short-term obligations as they fall due:

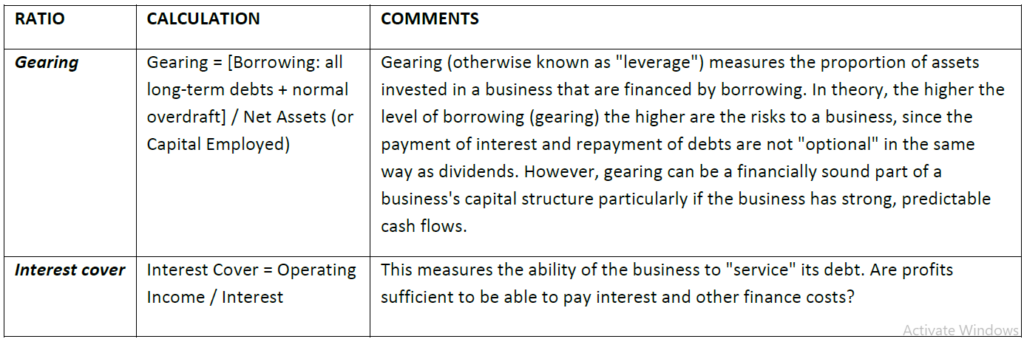

STABILITY RATIOS

These ratios concentrate on the long-term health of a business – particularly the effect of the capital/finance structure on the business:

COST INCOME RATIO

The cost to income ratio is an important indicator of the value of the company. It is used a lot in investment analysis to ascertain how easily the company can increase profits. The cost-to-income ratio shows the efficiency of a firm in minimizing costs while increasing profits. The lower the cost-to-income ratio, the more efficient the firm is running. The higher the ratio, the less efficient management is at reducing costs. Cost-to-income ratio equals a company’s operating costs divided by its operating income.

CASE STUDY

- Determine a firm’s operating costs. Operating costs are those which are directly related to running the firm, such as salaries and administrative expenses. For example, Firm A has R500,000 of operating expenses each month.

- Determine the firm’s operating income. Firms disclose operating incomes on their income statements. Operating incomes are cash inflows from the firm’s operation. In the example, a firm has operating income of R900,000 each month.

- Divide the firm’s operating expenses by the firm’s operating income. In the example, R500,000 divided by R900,000 equals Firm A’s cost to income ratio of 0.555.

Example

Vermin PLC has an annual income of R200 000, derived from sales at a cost of R100 000.

Then their cost to income ratio is;

100 000

200 000 = 1:2

To interpret this: for every R100 worth of sales, Vermin PLC makes a profit of 50c.