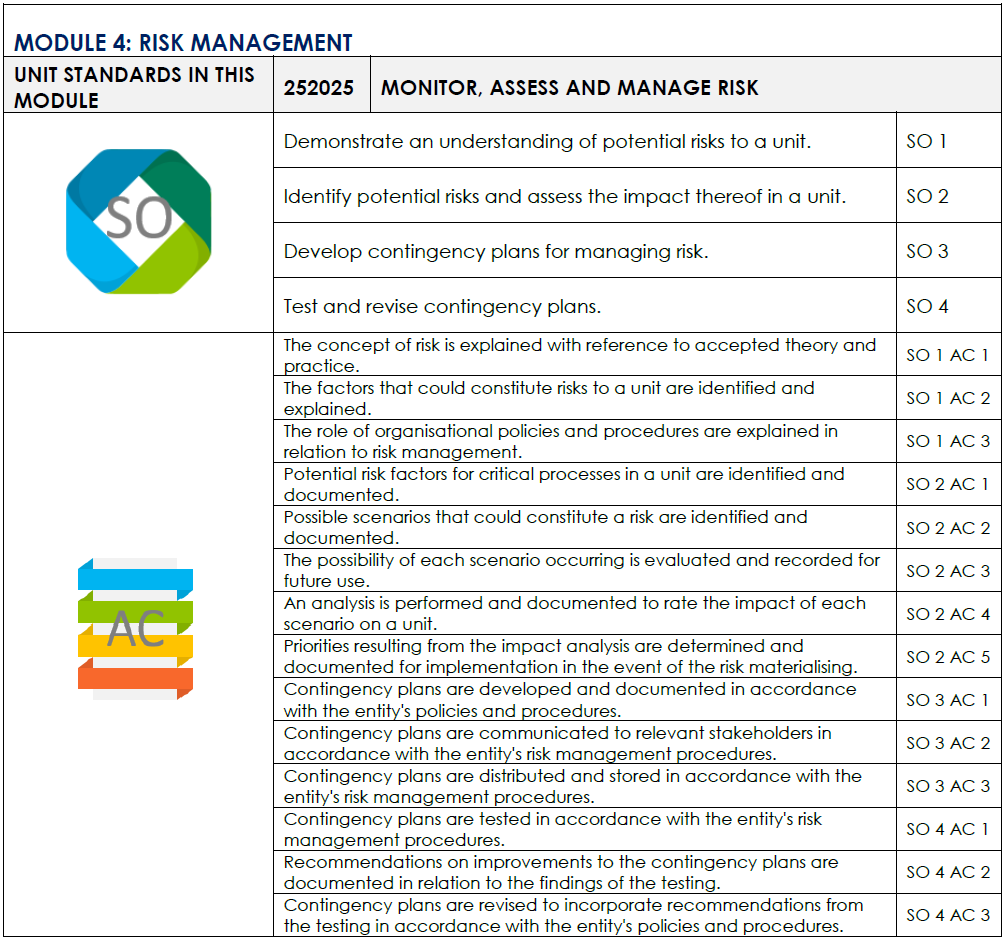

Demonstrate an understanding of potential risks to a unit.

MONITOR, ASSESS AND MANAGE RISK

There are many definitions and types of “risk’, but for the purposes of this module we will focus on risk in our business unit and say that “risk is anything that threatens the ability of an organisation or business unit to accomplish its goals”.

Risk is defined as the combination of the probability of occurrence of harm and the severity of that harm.

Severity is associated to a potential failure effect and indicates the related seriousness.

Occurrence is related to the causes of a potential failure mode and corresponds to the estimate of the number of failures that could occur. Hazard is a potential source of harm (physical injury to the health of people, damage to the property or to the environment).

Risk Management is the process of measuring, or assessing risk and then developing strategies to manage the risk. Risk management is a discipline for dealing with uncertainty. It enables people and organisations to cope with uncertainty by taking steps to protect vital assets and resources.

Risk Management is a systematic and structured decision-making process, focused on value creation, able to identify, assess and prioritise risks throughout the product life cycle.

Every organisation faces uncertainty and risk. Few, if any, operate in risk-free environments. From uncertainty about economic indicators to concerns about safety and the organisation’s ability to retain client support, managing a range of risks is required for both survival and success. Every organisation – even very small ones – can use risk management strategies and tools to protect vital assets.

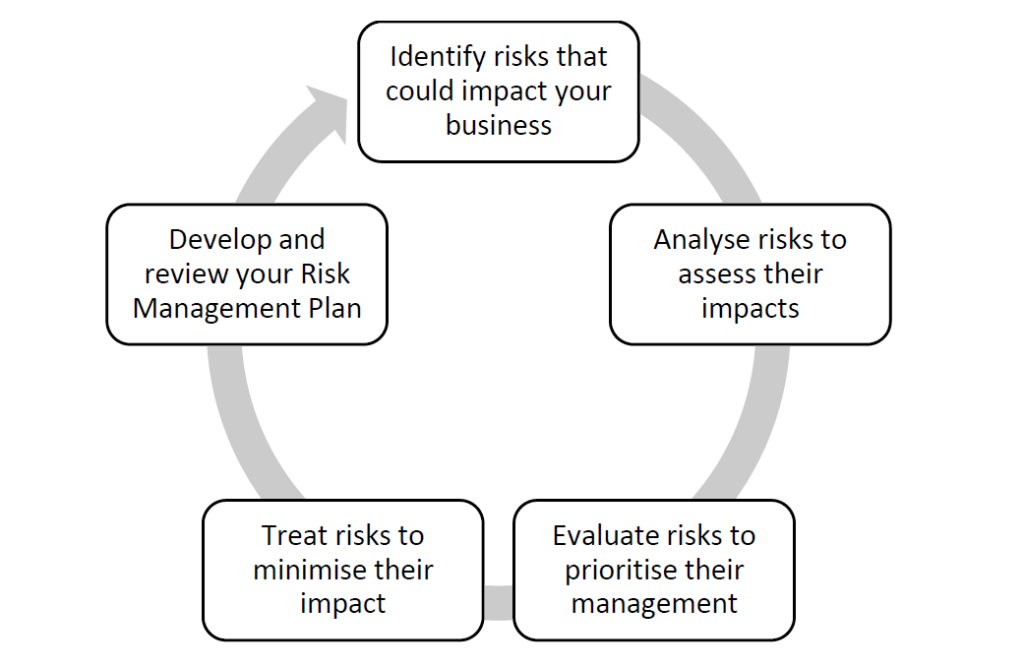

Risk Management is about identifying and analysing the things that may have a major effect on your business and choosing the best method of dealing with each risk. By developing a Risk Management Plan you ensure your business risks are managed.

The process of managing risks involves five steps:

Step 1: Identify risks that could impact your business:

Take a close look at each of your business operations and ask yourself:

What could have an impact?

How serious would that impact be?

What is the likelihood of this occurring?

Can it be reduced or eliminated?

For example, if you owned a cafe, your risks might include fire, food poisoning and floods (if you are located in a flood-prone area).

Step 2: Analyse risks to assess their impacts

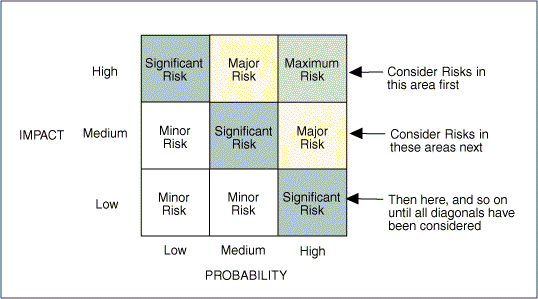

Determine which risks have a greater consequence or impact than others. Separate minor acceptable risks from major risks which must be managed immediately. This involves deciding on the relationship between the likelihood and impact of the risks you have identified.

In a cafe, the likelihood of a flood may be assessed as low, but the impact on the business would be very high. A flood could potentially destroy both equipment and stock and would lead to loss of trade and financial loss.

Step 3: Evaluate risks to prioritise their management

Compare the likelihood and impact of each risk to evaluate and prioritise the resources you are prepared to invest to treat these risks. The outcome of this step is a prioritised list of risks that require further action.

In the cafe example, your prioritised list may be:

Fire – your top priority risk. The likelihood is high and the potential impact of a fire on the business is very high.

Food poisoning – your second priority risk. Whilst the probability may be assessed as low, the impact on the business would be very high.

Flood – your third priority risk. The probability is assessed as very low, but again the impact on the business would be very high.

Step 4: Treat risks to minimise their impact

You will need to determine which risks are acceptable for your business to leave untreated and which risks need to be treated.

Risk treatment is about considering options for treating risks that are not considered acceptable, through a number of strategies including:

insurance

quality control processes

staff training

complying with government legislation and regulations

properly maintaining facilities, plant and equipment

using appropriate security devices

establishing systems and controls, e.g. segregation of duties (cash receipting, banking and accounting)

developing contingency plans.

Some of the treatment strategies for the risk of flood might include:

ensure flooding is covered by your existing insurance policy and the amount of cover is adequate

ensure stock and equipment are stored off the ground where possible

organise off-site storage for stock and equipment when a flood is forecast.

Step 5: Develop and review your Risk Management Plan

A Risk Management Plan indicates the chosen strategy for treatment of the identified risks. It details information about:

risks identified

level of risks

planned strategy

timeframe for implementing the strategy

resources required

individuals responsible for ensuring the strategy is implemented.

The final documentation should include appropriate objectives, a budget and milestones on the way to achieving those objectives.

Benefits of Risk Management

There are a number of benefits to having a solid risk management process, including:

Clear ownership and accountability for all risks

Creation of an environment where risks will be accepted by the business on an informed basis

An increased likelihood that the program will be a success, along with the increased likelihood that the objectives of the organisation will be met.

The discipline of risk management helps identify, assess and control risks that may be present in operations, service delivery, staffing, and governance activities. It is well worth the time to integrate risk management into your operations and there are many good reasons to do so:

The threat of litigation is increasing – Many organisations may never face a lawsuit, but those that do, know that it can be costly and time consuming. Good risk management can reduce these costs or perhaps help you to avoid a lawsuit altogether.

The risk of client/ staff harm – Your mission is to help people, not hurt them. Causing harm to a client, however unintentional, undermines your purpose and jeopardises your mission.

For your own safety and security – Sound risk management will help create a sense of confidence and safety about your operation. In an atmosphere where the threat of unnecessary risk is reduced, an organisation can be more creative in providing services to clients and achieving results.

The risks of not applying timeous and proper risk management are:

Not eliminating faulty practices

Reinforcing faulty practices

Blocking experimentation

Not encouraging experimentation

Blocking technical improvements

Not encouraging technical improvements.

Prioritising too highly the risk management process itself could potentially keep an organisation from ever completing a project or even getting started. This is especially true if other work is suspended until the risk management process is considered complete.

In general, the strategies employed in risk management include transferring the risk to another party, avoiding the risk, reducing the negative effect of the risk, and accepting some or all of the consequences of a particular risk. These will be discussed in more detail later.

Traditional risk management

Traditional risk management focuses on risks stemming from physical or legal causes (e.g. natural disasters or fires, accidents, death, and lawsuits).

Financial risk management

Financial risk management, on the other hand, focuses on risks that can be managed using traded financial instruments.

Intangible risk management

Intangible risk management focuses on the risks associated with human capital, such as knowledge risk, relationship risk, and process – engagement risk.

Knowledge risk occurs when deficient knowledge is applied.

Relationship risk occurs when collaboration ineffectiveness occurs.

Process-engagement risk occurs when operational ineffectiveness occurs.

These risks:

Reduce the productivity of knowledge workers

Decrease cost effectiveness

Reduce profitability

Impair service

Reduce quality

Damage reputation and brand value

Reduce earnings quality.

Intangible risk management allows risk management to create immediate value from the identification and reduction of risks that reduce productivity.

Regardless of the type of risk management, all large corporations have risk management teams and small groups and corporations practise informal, if not formal, risk management.

In the ideal risk management scenario, a prioritisation process is followed whereby the risks with the greatest loss and the greatest probability of occurring are handled first, and risks with lower probability of occurrence and lower loss are handled later.

In practice, the process can be very difficult, and balancing between risks with a high probability of occurrence, but lower loss vs. a risk with high loss, but lower probability of occurrence can often be mishandled.

Risk management also faces a difficulty in allocating resources properly. This refers to the concept of opportunity cost. Resources spent on risk management could instead be spent on more profitable activities. Again, the ideal risk management scenario entails spending the least amount of resources on the process of managing risks, while reducing the negative effects of the risks as much as possible.

Demonstrate an understanding of potential risks to a unit

Risk is exposure to loss as a consequence of uncertainty. The impact of risk can be measured by the likelihood of an unwanted event occurring and the consequences if it does occur. For planning purposes, the impact of risk could be the same for both small damage resulting from a highly probable recurring event and very large damage resulting from a rare event.

Concept of Risk

Risk can be defined as “the potential impact (positive or negative) to an asset or some characteristic of value that may arise from some present process or from some future event”.

Risk – The probable frequency and probable magnitude of future loss

There are three important things to recognise from this definition:

First and most obvious – risk is a probability issue. We’ll cover this in more detail throughout the learner guide.

Second – risk has both a frequency and a magnitude component.

And third – is that this definition for risk applies equally well regardless of whether we’re talking about investment, market, credit, legal, insurance, or any of the other risk domains (including information risk) that are commonly dealt with in business, government and life. In other words, the fundamental nature of risk is universal, regardless of context.

In everyday usage, “risk” is often used synonymously with “probability” and restricted to negative risk or threat.

In professional risk assessments, risk combines the probability of an event occurring with the impact that event would have.

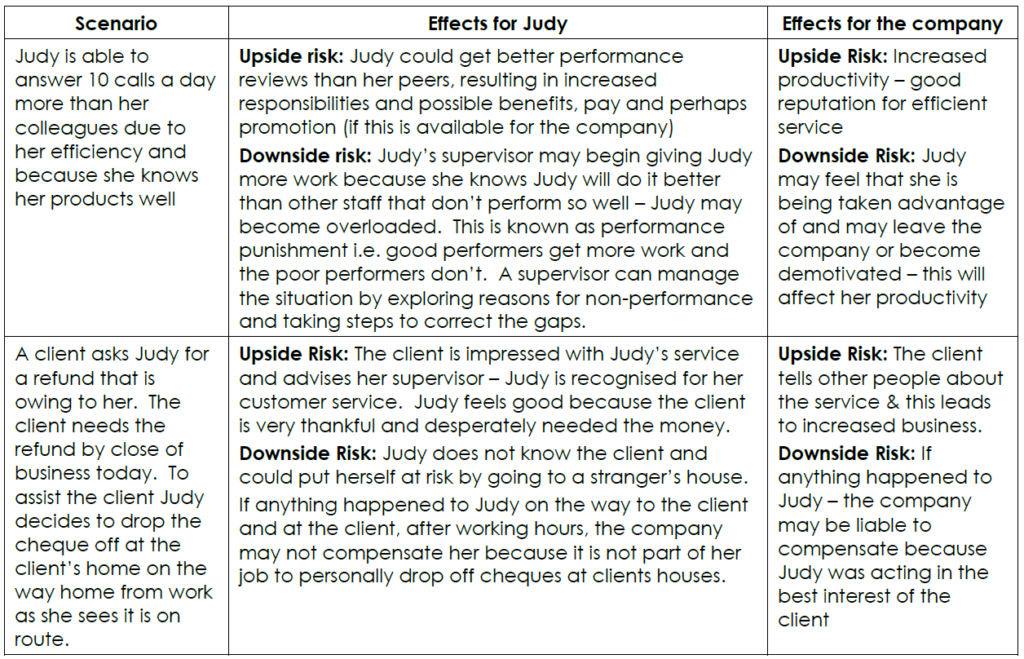

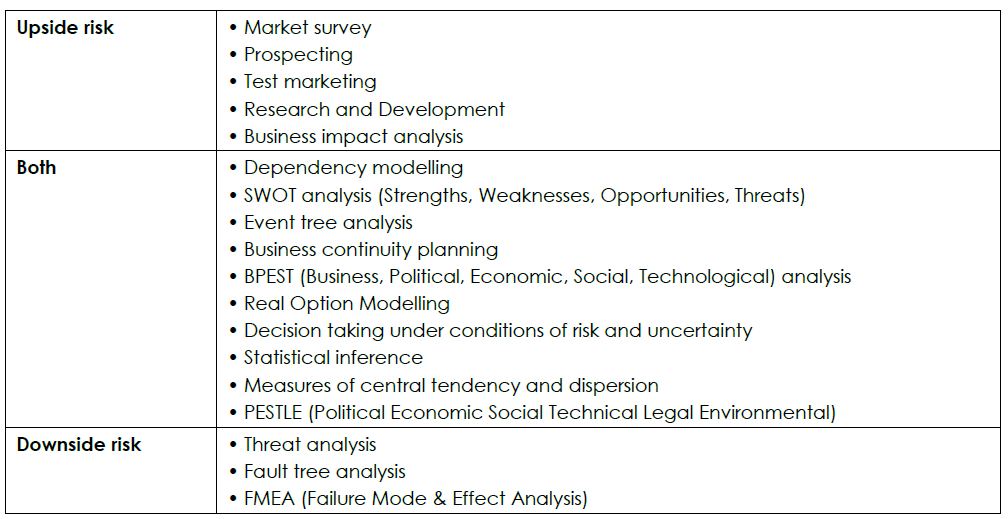

Risks can be defined as many things, but at the root of every definition is the fact that risks represent uncertain outcomes. These outcomes can be either negative or positive. They can represent positive opportunities (opportunities for excellence), as well as negative threats.

Types of Risk

Upside risk

An upside risk is something that might happen that’s better than some benchmark level. The benchmark is something we choose, but typically it is our planned or expected outcome, or the outcome we think ‘ought’ to happen.

In some areas of risk management the upside is more important than in others. In safety, for example, the natural benchmark is ‘total safety’ (one does not want to speculate about how many people one ‘expected’ or ‘planned’ to kill or injure.) Consequently there is no upside to speak of.

By contrast, in financial risk management it is natural to talk about expected returns and there’s nearly always an important upside to consider.41

Positive risk refers to risk that we initiate ourselves because we see a potential opportunity, along with a potential for failure. We have to be intelligent risk takers. For example, we have a project that is scheduled to take 90 days to complete. The client would rather the project be delivered earlier, and would get more value if it were delivered earlier, but understands that 90 days is how long the project will take. One of your team members has an idea: If you utilise a new machine, it’s possible that you can deliver the project in 60 days instead of 90. If this were a guaranteed solution, you would jump on it. However, there is risk, since it will be the first time you’ve used the machine. You have to deal with a lack of expertise and a learning curve. It’s possible that if the machine doesn’t work out, the project could end up taking 110 days to deliver. What would you do?

Downside risk

The risk that an asset will decline in value, including the implications of risk, e.g. a “worst case” scenario of the gradation of risk in which an investor will lose money in a business venture if the venture fails.

Negative risk is represented by potential events that could harm a project. In general, these risks are to be avoided, e.g. you have a supplier that you’re counting on to provide raw materials to build a prototype. The supplier has a union contract that expires in the next 60 days. There is a risk that the supplier will have a strike that will disrupt shipments. You need to identify this as a risk, estimate the probability of occurrence (perhaps this will increase or decrease over time), determine the impact to the build if it occurs, and then put together a plan to minimise the impact on the project if it occurs

Example:

The implications of meeting and exceeding or not meeting quality requirements are also referred to as upside and downside risk.

Upside risk is the potential gain for both the individual and the company if standards are met and exceeded.

Downside risk is the potential loss both the individual and the organisation may suffer if quality standards are not met.

The following examples will help you gain a better understanding of the upside and downside risks of the outputs of a job:

When outputs are produced according to quality requirements the employee, company and customers benefit. The business stays profitable and attracts more customers.

When outputs are not produced according to quality requirements, a lot of time is wasted fixing up errors, re-doing work which ultimately costs money and could even result in the business having to close down, customers being dissatisfied, employees being dismissed for poor ratings, etc. There is always a price to pay for not doing the job correctly.

Categories of Risk

There are many examples of risk in business. To identify your specific business risks, consider them in categories.

The link between RISK and LOSS is obvious – and it has produced during the past 50 years a group of specialised activities all devoted to reducing loss. Ironically – though each “petal of the RISK flower42” attempts to minimise corporate loss. Further, they are unaccountable for the resources management invests in them. Not one of them can provide “dollars saved per dollar invested.”

Risk categories should be considered one by one, providing a structured approach to risk identification. This enables greater focus on a particular category, stimulating thought, and increasing the opportunity of identifying a broader range of risks.

Common risk categories are:

Financial – includes cash flow, budgetary requirements, tax obligations, creditor and debtor management, remuneration and other general account management concerns.

Equipment – extends to equipment used to conduct the business and includes everyday use, maintenance, depreciation, theft, safety and upgrades.

Organisational – relates to the internal requirements of a business, extending to the cultural, structural and human resources of the business.

Security – includes the business premises, assets and people. Also extends to security of company information, intellectual property, and technology.

Legal and regulatory compliance – includes legislation, regulations, standards, codes of practice and contractual requirements. Also extends to compliance with additional ‘rules’ such as policies, procedures or expectations, which may be set by contracts, customers or the social environment.

Reputation – entails the threat to the reputation of the business due to the conduct of the entity as a whole, the viability of products/services, or the conduct of employees or others associated with the business.

Operational – covers the planning, daily operational activities, resources (including people) and support required within a business that results in the successful development and delivery of products/services.

Contractual – meeting obligations required in a contract including delivery, product/service quality, guarantees/warranties, insurance and other statutory requirements, non-performance.

Service delivery – relates to the delivery of services, including the quality of service provided, or the manner in which a product is delivered. Includes customer interaction and after-sales service.

Commercial – includes risks associated with market placement, business growth, product development, diversification and commercial success. Also to the commercial viability of products/services, extending through establishment, retention, growth of a customer base and return.

Project – includes the management of equipment, finances, resources, technology, timeframes and people involved in the management of projects. Extends to internal operational projects, business development and external projects such as those undertaken for clients.

Safety – including everyone associated with the business: individual, workplace and public safety. Also applies to the safety of products/services delivered by the business.

Workplace safety – Every business has a duty of care underpinned by legislation. This means that all reasonable steps must be taken to protect the health and safety of everyone at the workplace. Occupational health and safety is integrated with the overall risk management strategy to ensure that risks and hazards are always identified and reported. Measures must also be taken to reduce exposure to the risks as far as possible.

Stakeholder management – includes identifying, establishing and maintaining the right relationships with both internal and external stakeholders.

Client-customer relationship – potential loss of clients due to internal and external factors.

Strategic – includes the planning, scoping, resourcing and growth of the business.

Technology – includes the implementation, management, maintenance and upgrades associated with technology. Extends to recognising critical IT infrastructure and loss of a particular service/function for an extended period of time. It further takes into account the need and cost benefit associated with technology as part of a business development strategy.

Knowing your risk categories can assist you in risk planning and communicating risk information. They provide a structure for identifying risk and are often initially identified through a brainstorming exercise.

Factors that could constitute Risks to a Unit

The risks facing an organisation and its operations can result from factors both external and internal to the organisation. The risks can be categorised into types of risk such as strategic, financial, operational, hazard, etc.

Financial risks are typically well controlled and are part of the routine focus of management risk discussions, with increased regulatory, accounting and financial audit focus. As financial information is a key element of stakeholder communications, performance measurement and strategic delivery, management risk discussions will devote considerable time to these risks. Financial risk is often defined as the unexpected variability or volatility of returns, and includes both potential worse than expected as well as better than expected returns. We know that organisations require a steady stream of reliable income in order to operate and grow

Operational risks are typically managed from within the business and often focus on health and safety issues where industry regulations and standards require. These internally driven risks may affect your organisation’s ability to deliver on its strategic objectives.

Hazard risks often stem from major exogenous43 factors, which affect the environment in which the organisation operates. A focus on the use of insurance and appropriate contingency planning will help address some of these. However, there is often a danger that as many of these risks cannot be controlled, boards and senior management will not reflect these in their strategic thinking. Confining strategic management to controllable factors will leave your business at risk of failing to address these factors.

Strategic risks are typically external or affect the most senior management decisions. As such, they are often missed from many risk registers. Your senior management has a responsibility to make sure all these types of risks are included in their key strategic discussions.

Asset Risk

Some organisations prefer to look at factors related to asset when identifying factors that could constitute risks to a unit.

We can categorise asset risk according to four major categories of assets:

Property risk – Property includes:

o Buildings

o Office furniture and fixtures

o Computers (hardware and software)

o Intellectual property (trademark, logo, copyright, patent, etc.)

o Motor vehicles

o Other equipment (lawn maintenance equipment, contractors’ equipment, audio-visual equipment, laptops, exhibits, etc.)

Property also includes cash and securities, financial assets and even borrowed property. Property risks come in various forms, including those caused by nature (flood, earthquake, hurricane, forest fires, wind/tornadoes, extreme heat or cold) and others resulting from human intervention (fire, theft, vandalism, collision, carelessness). The risks of loss associated with property and income assets could devastate an organisation. Imagine what would happen if your organisation’s computers and accounting records were lost in a fire, or if a significant sum of money were embezzled.

Income risk – Depending on the type of organisation, common sources of income include:

o Donations

o Grants

o Government contracts

o Fees for services

o Investment income

o Merchandise sales

o Loans

o Proceeds from special events

o Sponsorship fees

o Registration/ participation fees

o Membership dues

Most managers have come face to face with an income risk, such as the loss of budget, sales falling shy of projections, contract cancellations and more. A disaster such as a fire or flood can also curtail operations, resulting in an interruption of the income stream. Consequences of a loss can range from inconvenience to devastation. While income ups and downs are arguably part and parcel of the business world, it’s possible to use risk management techniques to reduce the likelihood that a loss of income will destroy an organisation.

Some techniques for reducing income risk include:

o Business interruption insurance

o Establishing a reserve fund

o Implementing sound financial controls

o Diversifying income sources

Goodwill risk – Goodwill is an asset that is difficult, if not impossible, to quantify. A more descriptive word might be “reputation.” Every organisation understands that its reputation is key to recruitment of staff and customers, retention of those staff and customers, and overall good organisational health. Damage to reputation can be devastating, and many organisations would have a hard time recovering from a blow to their reputation. In many cases, damage to reputation occurs in the wake of a crisis, such as a scandal involving maladministration or widely publicised client injury. In some cases there may be guilt by association if a corporate partner comes under fire. Even an incident of tax evasion by a major shareholder could have repercussions for an organisation

Operational risk – Operational risk is defined as the risk of loss resulting from inadequate or failed internal processes, people and systems, or from external events.

Examples of operational risk include:

o Technology failure

o Business premises becoming unavailable

o Inadequate document retention or record-keeping

o Poor management

o Lack of supervision

o Lack of accountability

o Poor control

o Errors in financial models and reports

o Attempts to conceal losses

o Attempts to make personal gains

o Third party fraud

A delict is an act (or omission) which in a wrongful and culpable way causes loss to another – responsibility toward society at large. This is where potential losses are most difficult to estimate. You may have heard of the Thalidomide disaster. In the 1960’s a drug meant to relieve morning-sickness in pregnancy resulted in babies being born deformed. It is thought that a similar disaster under today’s conditions could result in awards as high as R5bn. (This is an example of Products Liability).

A boiler explosion might cause tremendous physical damage, and interrupt production, but the liability claims for physical injury and damage to third party property can be even bigger.

An organisation can suffer loss even without legal liability being established:

o The cost of investigation, and documenting their defence;

o Legal fees;

o Out of court settlements, where it is considered more cost effective to settle with the claimant, than risk everything on the outcome of an expensive court action.

o Where disputes actually go to court, legal costs are much greater, as are the actual awards handed down.

People risk – People are the heart and soul of an organisation. They represent the talent, commitment and community your organisation serves. The people assets in your organisation include staff, clients and shareholders.

Examples of people risk include:

o Risk of Staff Loss: Each person is a unique individual with a unique set of skills. In a very real sense, each is irreplaceable. So the first risk in terms of employees is the risk of loss of talent/ expertise when a trained and skilled employee leaves the organisation.

o Health and safety: Another risk is that of loss due to injury or death. Unlike damage to property or loss of income, injuries sustained by employees may never be fully repaired and could lead to expensive litigation. In the workplace, an organisation’s priority must be the health and safety of all. The goal is the prevention of occupational health risks, accidents and injury. This means that all must work to legal health and safety standards and improve on these wherever possible. All employees must constantly be on the alert against possible hazards and hazardous behaviour. The organisation must minimise such hazards with well-designed procedures, processes, equipment and safety training programmes. The organisation must ensure that all employees are aware that irresponsible or careless activities place themselves and others at risk.

o Employee turnover: In terms of employee decision-making, Andrew Wong44 says it is natural for an employee to aspire to earn a better salary. Financial gain not only helps to meet the financial needs and improve the lifestyle of the person and his/her family, it may also reflect greater capability of the employee to take up greater scope of work or responsibilities. An opportunity may arise whereby there is a significant financial gain (e.g. higher salary, or allowances or both), but with higher occupational hazards, or perhaps s/he has an opportunity to work in a foreign country which has security risks, or entails harsh living conditions for the employee and the family. Of course, each person has his or her own tolerance level with respect to the above-mentioned risks. Rationally and emotionally, he or she will make decisions based on certain criteria, making the necessary evaluation and assessment. The general rationale is “suffer a few years for that extra significant financial gain” and this then becomes the governing principle or reason to make the decision to take up a new job or transferred position. However, in the scenario described by Wong, there is also a significant risk to the organisation: if the employee perceives the payoff to be “not worth it” after a while and cannot handle the increased workload or strain, s/he can become demotivated and unproductive, even though it was his/her own choice. That is why organisations have Wellness or Employee Assistance Programmes (EAP) in order identify, interact with and refer troubled employees before they affect productivity and team morale.

o At Risk Behaviour: As a manager, you will be held accountable for your subordinates’ behaviour – good or bad. You can take a proactive approach to eliminating at risk behaviour by recognising its causes in the workplace. The possible sources of at risk behaviour are endless and will vary on its degree of severity and the impact it will have on the performance of your team. Some sources of at risk behaviour could relate to the following:

Ignorance – Ignorance could create at-risk behaviour when your subordinates don’t know all they should about a situation. As a result, they might not be able to recognise, diagnose, or fix a dilemma. You should make sure that your subordinates are educated about your company and its current activities, goals, vision, values policies and procedures. By training your employees on these issues you could pro-actively avoid future high risk situations.

Lack of recognition by management – Recognition by management is an important form of reward for an employee. If a manager does not recognise an employee who needs recognition, the employee can become frustrated and might change his/her behaviour patterns to gain the manager’s attention. Although this attention could be negative, the employee would rather be recognised this way than not at all, e.g. an employee might start coming in late regularly or fail to submit reports or start to verbally abuse others, simply to get attention. This could in the long term impact negatively on conduct, productivity, performance and capacity.

Personal financial burdens – When an employee does not earn enough money to cover personal expenses, he might become a high risk, especially if he/she works with money. In this instance at risk behaviour can have two objectives: to take revenge on the organisation, or to obtain enough money to cover their personal expenses. As a manager, you might have the authority to determine salary levels for your subordinates. It is unrealistic for managers to grant subordinates all the salary they might want. Yet it is realistic to pay employees a salary based on industry standards. If your organisation’s salary levels fall below such standards, you can expect to encounter at risk behaviour.

Substance Abuse – This includes drugs and alcohol and has, in recent years become a serious social and business problem. The substance abuser poses a major threat to an organisation in terms of productivity, performance and conduct. The condition is often not apparent but manifests itself with poor performance issues, absenteeism and financial burdens.

o Environmental and Corporate Social Responsibility: Outside of the workplace, an organisation’s priority must be to act responsibly by protecting the environment and the communities around it. In addition, organisations must ensure that they act responsibly at all times in the disposal of waste and in pollution control.

Acts and Regulations related to Risk Management

In terms of the South African Compensation for Occupational Injuries and Disease Act, applicable to most classes of employees, automatic compensation is paid from a state administered fund. This relieves employees from having to prove negligence by the employer, but also means that they cannot sue the employer.

This does not free the employer of the need to take suitable precautions.

Requirements have been laid down, some of the principal statutes being:

The Occupational Health and Safety Act No 85 of 1993 (as amended)

The Mines and Works Act No 27 of 1956 (as amended)

The Electricity Act No 40 of 1958 (as amended)

all as read in conjunction with the Criminal Procedure Act No 51 of 1977 (as amended).

Failure to meet these requirements will result in criminal action against the person responsible. Special audit sheets are needed to check that the requirements are met.

Note: These are also regulations relating to specific trades and types of hazard.

Role of Organisational Policies and Procedures

Quality standards are defined in terms of company, legislation or industry standards. Company policies and procedures are developed as a result of interpreting industry standards and/or legislation. The company policies and procedures form part of the risk management process in that they provide guidelines to ensure that the company adheres to industry standards and Statutory Requirements, e.g. Acts, Bills

Regulatory Requirements, e.g. Regulations, Rules

Supervisory Requirements, e.g. Directives, Codes, Standards, Procedures, Rulings

Company codes, policies and procedures

Risk Management Policy

An organisation’s risk management policy should set out its approach to and appetite for risk and its approach to risk management. The policy should also set out responsibilities for risk management throughout the organisation.

Furthermore, it should refer to any legal requirements for policy statements e.g. for Health and Safety.

Attached to the risk management process is an integrated set of tools and techniques for use in the various stages of the business process. To work effectively, the risk management process requires:

commitment from the chief executive and executive management of the organisation

assignment of responsibilities within the organisation

allocation of appropriate resources for training and the development of an enhanced risk awareness by all stakeholders.

Quality Standards

Quality standards are the measurable quality requirements for each work responsibility or duty, often referred to as the output of your work.

Outputs are the products and services that individuals in an organisation provide to one another or to the customer, such as:

An answered telephone

A clean floor

A serviced car

A completed report

An issued policy document

A teamwork plan.

Listing responsibilities as outputs is useful, because there are many ways to produce an output even though the standards that need to be maintained are the same. By listing outputs you encourage a process of continuous improvement, because you create a certain amount of freedom, to the person producing the outputs, to experiment with different ways of doing the work in an attempt to improve the way the outputs are produced.

Example: The receptionist is required to answer the telephone within 3 rings in a polite professional manner.

As the standard has been set, the receptionist can now be measured accordingly.

The receptionist would have been informed why this is important (image of the company) and would now understand why she has to comply with the standard.

Quality standards provide guidelines in terms of requirements that need to be met to make sure that the outputs are produced according to set standards. Quality standards are often defined in terms of regulatory compliance, cost, time, quantity and quality.

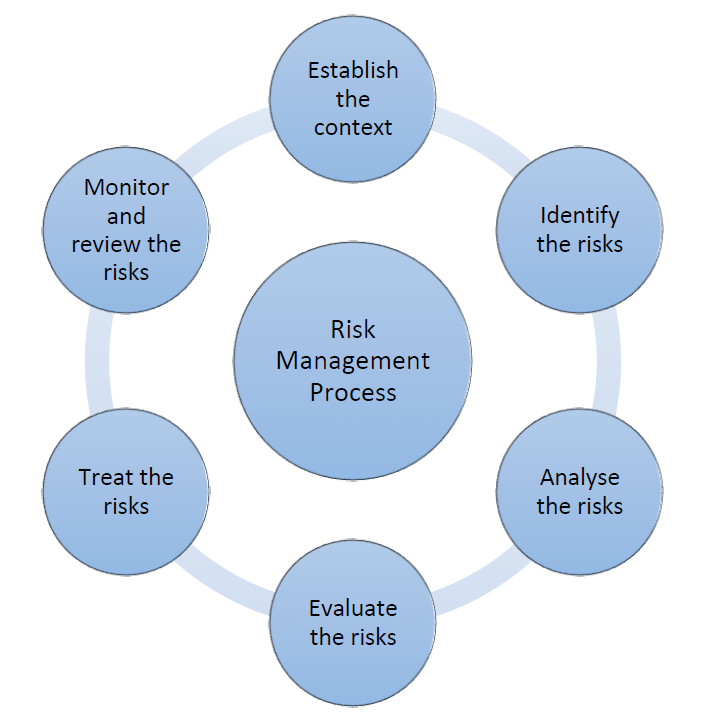

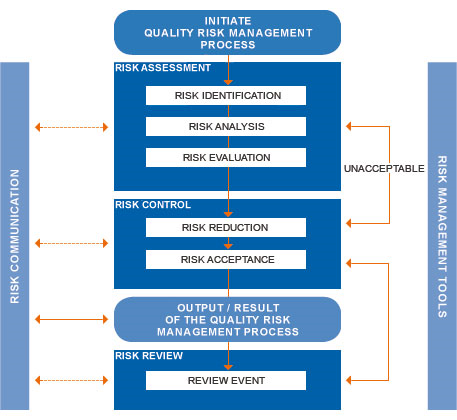

The risk management process is the series of steps that enable initial and continual review of risk, and help to ensure that the business is on-track for meeting its objectives.

The risk management process helps to put in place and review the risk management plan.

The elements of the risk management process are:

establish the context

identify the risks

analyse the risks

evaluate the risks

treat the risks

monitor and review.

- Establish the context

When considering risk management within a small business, it is important to establish boundaries for the risk management process. For example, a business owner may be only interested in identifying financial risks so information collected will only cover that area of risk.

In establishing the context, consider:

the objectives of the business

key stakeholders and impacts

risk categories.

It is generally more productive to break down the risks into categories, rather than identify risks for the company as a whole. - Identify the risks

Risk cannot be managed unless it is identified. Once the context of the business has been defined, the next step is to use this information to identify as many risks as possible.

The aim is to identify the risks that may affect, either negatively or positively, the objectives of the business and all its activity.

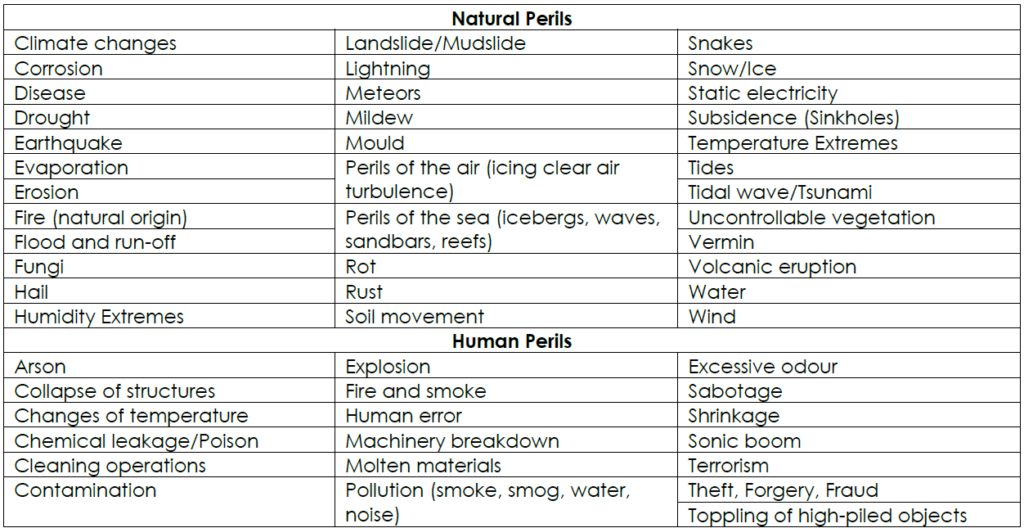

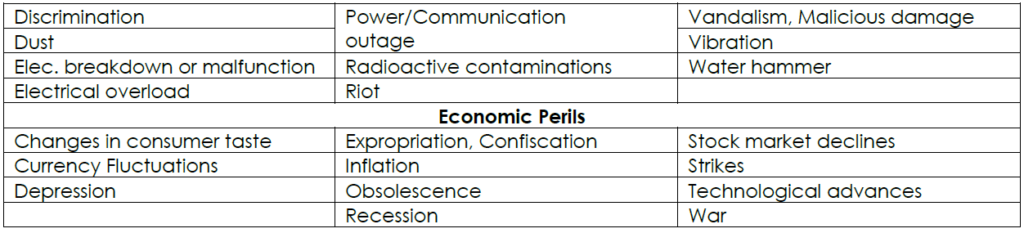

Identify the range of hazards, threats, or perils that impact or might impact:

your organisation.

your infrastructure.

the surrounding area.

You will need to:

Identify retrospective risks – Retrospective risks are seen in incidents or accidents that have occurred in the past. Retrospective risk identification is the most common way to identify risk and the easiest. A risk is easier to understand if its impact has already been experienced. It is also easier to quantify its impact and to evaluate the damage. There are many sources of information about retrospective risk including:

o hazard or incident logs or audit reports

o customer complaints

o accreditation documents and reports

o staff or client surveys

o newspapers or professional media, such as journals and websites.

Identify prospective risk – Prospective risks are harder to identify. These are things that have not yet happened, but might happen in the future. Identification should cover all risks, whether or not they are currently managed. The plan will be to record all significant risks and monitor the effectiveness of their treatment. Methods for identifying prospective risks include:

o brainstorming with staff and external stakeholders

o researching the economic, political, legislative and operating environment

o interviewing staff and clients to identify potential problems

o flow charting a process

o reviewing system design or preparing system analysis.

Risk categories will help break down the process for prospective risk identification. It is important to remember that risk identification will be limited by the experience and perspective of those conducting the risk analysis. Problem areas and risks can be best identified by the use of reliable sources.

In addition, understanding categories assists business owners to select the best tools and techniques for risk identification and analysis. For example, if a particular risk category is technical in nature, the risk identification methodology used will involve significant research and collection of existing information about risk exposure.

- Analyse the risks

During risk identification, a business owner may have identified many risks but it is often not possible to address all of them.

Determine the potential impact of each hazard, threat, or peril by estimating the:

relative severity of each hazard, threat, or peril (danger).

relative frequency of each hazard, threat, or peril.

vulnerability to each hazard, threat, or peril of your people, your operations, your property, and your environment.

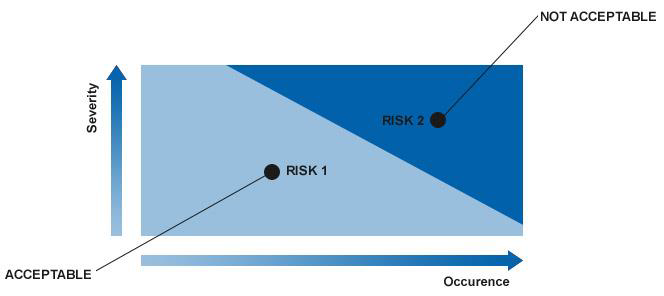

Risk analysis will determine which risks have a greater consequence. This will provide better understanding of the possible impact of a risk, and the likelihood of it occurring. That leads to decisions about resources required to control the risks.

Risk analysis involves combining the possible consequences, or impacts, of an event, with the likelihood of that event occurring. The result is called a ‘level of risk’.

Risk = consequence x likelihood.

The risk analysis should be documented in the risk management plan. - Evaluate the risks

It is important to determine how serious the risks facing a business are. The business owner must determine the level of risk that a business is willing to accept. Risk evaluation involves comparing the level of risk found in the analysis process with previously established risk criteria. From there it must be decided if these risks require treatment.

Categorise each hazard, threat, or peril according to how severe it is, how frequently it occurs, and how vulnerable you are.

The result of a risk evaluation is a prioritised list of risks that require further action. This step is about deciding whether risks are acceptable or need treatment.

Low or tolerable risks may be accepted. ‘Accepted’ means the business chooses to accept that the risk exists, either because the risk is low and the cost of treating it would be uneconomic, or there is no reasonable treatment that can be implemented.

A risk may be accepted if:

the cost of treatment exceeds the benefit, so that acceptance is the only option (applies particularly to low risks)

the level of the risk is so low that specific treatment is not called for

the opportunities presented outweigh the threat to such a degree that taking the risk is justified

there is no treatment for the risk – for example, the risk that the business may suffer storm damage.

If the risk is medium or high and therefore not acceptable, the risk must be mitigated or treated. Specific actions to treat the risk should be outlined in the risk management plan.

- Treat the risks

Risk treatment is about options for dealing with risks that are not acceptable. Risk treatment involves identifying controls for risk. The aim is to either reduce or eliminate negative consequences, or to reduce the likelihood of an adverse occurrence. Risk treatment should also enhance positive outcomes.

It is often not possible, nor cost-effective to implement all treatment strategies. A business owner should choose, prioritise and implement the best combination of risk treatments.

Develop strategies to deal with the most significant hazards, threats, or perils. Develop strategies (risk treatments) to:

prevent,

mitigate,

prepare for,

respond to, and

recover from hazards, threats, or perils that impact or might impact your organisation and its people, operations, property.

The steps to this are:

identify – develop and design treatment options

evaluate – do the options satisfy treatment objectives and are they cost effective?

develop and implement a risk treatments and controls.

For businesses, many of the treatments are often part of establishing everyday business practices and procedures such as:

staff training and development

financial reporting systems

good customer management

ensuring compliance.

Therefore, ensuring good management practices are already in place will help you control risks from the outset.

A quality assurance program can also help to control risk. Quality assurance is the process that continues from risk treatment through monitoring and review to a cycle of continuous improvement.

All risk treatments should be documented in your risk management plan.

- Monitor and review the risks

Monitoring is an essential step in the risk management process. A business owner / manager must monitor risks and review the effectiveness of treatments and strategies that have been set up to manage risk.

Risks need to be monitored regularly to ensure changing circumstances do not alter risk priorities. Very few risks are static, therefore the risk management process needs to be repeated often, so that new risks are captured into the process and can be effectively managed

A risk management plan should be reviewed at least annually. The best way to make sure this occurs is to combine the review with annual business planning.

The risk management plan

The risk management plan is a document which outlines the risks faced by the business and provides guidance on risk mitigation strategies.

The risk management plan should contain:

identified risks

rating of the impact of the risk for the business (i.e. low, medium, high)

rating of the likelihood of the risk occurring (i.e. low, medium, high)

actions taken or to be taken to mitigate the risks

timeframes for review.

Risk management in a business should not be a stand-alone plan. There are relationships between risk management and many of the management processes and techniques that may be employed to ensure the successful operation of a business.

Good practice is to ensure that all of the following business areas are considered when developing the risk management plan:

business planning

occupational health and safety

human resources management

compliance

financial management

client management

contract management

quality assurance.

The risk management plan should be reviewed regularly and updated as needed to ensure all risks in the business are being covered.

Example:

We will be exploring the main parts of the risk management process in more detail in the rest of this learner guide, whilst learning more about monitoring, assessing and managing risk.

IDENTIFY POTENTIAL RISKS AND ASSESS THE IMPACT THEREOF IN A UNIT

All organisations need to manage risks but the good news is that many of the risks that face organisations on a daily basis are those that are within their own control. Many organisations have adopted a structured approach to risk assessment45. Risk assessment does not necessarily require sophisticated tools. They can be conducted simply by asking some key questions. Even for those events that are outside your control, there are steps you can take to avoid, contain or reduce adverse impact on the organisation.

If you were to ask your management team about risk, would your management team know:

What factors affect the organisation’s ability to accomplish its mission or its objectives?

What provisions had been made to contain, reduce or control risk?

In which processes were these controls installed?

How the effectiveness of these provisions is being measured?

What recent changes have been made to these processes to improve their robustness in preventing the risk having a detrimental effect on the business?

If you were also to ask your management team about the provisions it has made to mitigate against risk would it be able to explain what provisions had been taken to safeguard the organisation from:

Attack by competitors, disgruntled employees, computer viruses

Losing customers, suppliers, employees, reputation

Decline in orders, revenue, profit, market share

Dissatisfying customers, shareholders, employees

Prosecution by regulators, customers, employees

Delayed delivery

Delayed receipt of product or payment

Hazards injurious to health of personnel and/or the environment

Accidents to personnel and equipment

Breakdown of equipment, plant, machinery, relationships

Disruption to business continuity by computer failure, loss of information, strikes, weather.

Certain techniques can identify potential risks and assist in their elimination, reduction or control if the provisions are built into process design.

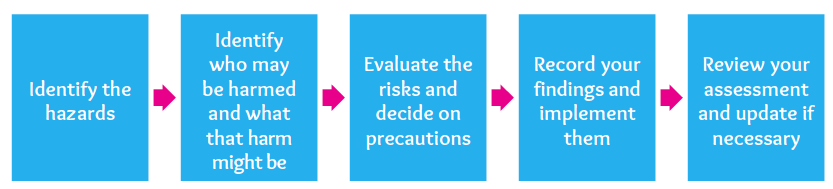

A risk assessment is simply a careful examination of what, in your work, could cause harm to people, so that you can weigh up whether you have taken enough precautions or should do more to prevent harm. Workers and others have a right to be protected from harm caused by a failure to take reasonable control measures.

Accidents and ill health can ruin lives and affect your business too if output is lost, machinery is damaged, insurance costs increase or you have to go to court. You are legally required to assess the risks in your workplace so that you put in place a plan to control the risks.

Use the Risk Management Process

Risk Assessment consists in the hazards identification and the analysis and evaluation of risks associated with exposure to the identified hazard. In this phase a comparison of the identified and analysed risk against given risk criteria will be done.

Risk Control includes risk mitigation which may include actions taken to reduce the severity and probability of harm for risks that fall into the “intolerable” category.

The implementation of risk mitigation measures can introduce new risks into the system or increase the significance of other existing risks. Hence, a revision of the risk assessment to identify and evaluate any possible change in risk after implementing a risk control measure will be done.

Every risk control measure will be verified for proper implementation as well as effectiveness in achieving the intended degree of risk mitigation, usually through an on-going validation process.

Risk Communication is the exchange or sharing of information about risk and its management between the decision makers and others. Parties can communicate at any stage of the risk management process. The included information might relate to the existence, nature, form, probability, severity, acceptability, treatment, detect ability or other aspects of risks to quality. This exchange need not be carried out for each and every risk acceptance.

The output of the quality risk management process should be documented when a formal process has been utilised.

Risk Review consists of the continuous improvement of the risk management results. The risk management approach will be introduced in the system and it might be used when new risks arise.

Example: Health and Safety Risks

If you work in a larger organisation, you could ask a health and safety adviser to help you. If you are not confident, get help from someone who is competent. In all cases, you should make sure that you involve your staff or their representatives in the process. They will have useful information about how the work is done that will make your assessment of the risk more thorough and effective. But remember, you are responsible for seeing that the assessment is carried out properly.

When thinking about your risk assessment, remember:

a hazard is anything that may cause harm, such as chemicals, electricity, working from ladders, an open drawer, etc. and

the risk is the chance, high or low, that somebody could be harmed by these and other hazards, together with an indication of how serious the harm could be.

Risk assessment is probably the most important step in the risk management process, but may also be the most difficult to accomplish and the most prone to error.

Uncertainty in the measurement of risk is due to the fact that no single metric embodies all of the information in the measurement. Normally, two quantities are being measured, e.g. extent of loss and probability of loss. A risk with a large potential loss and a low probability of occurring will be treated differently from one with a low potential loss but a high likelihood of occurring. In theory, both are of nearly equal priority, but in practice it can be very difficult to manage when faced with the scarcity of resources, especially time, in which to conduct the risk management process.

Means of measuring and assessing risk vary widely across different professions, e.g. a doctor manages medical risk and a civil engineer manages risk of structural failure.

If risks are improperly assessed and prioritised, time can be wasted in dealing with risk of losses that are not likely to occur. Spending too much time assessing and managing unlikely risks can divert resources that could be used more profitably.

Unlikely events do occur, but if the risk is unlikely enough to occur, it may be better to simply retain the risk, and deal with the result if the loss does in fact occur.

The fundamental difficulty in risk assessment is determining the rate of occurrence since statistical information is not available on all kinds of past incidents. Furthermore, evaluating the severity of the consequences (impact) is often quite difficult for immaterial/ intangible assets.

Asset valuation is another question that needs to be addressed. Thus, best educated opinions and available statistics are the primary sources of information.

Nevertheless, risk assessment should produce information for the management of the organisation in such a way that the primary risks are easy to understand so that the risk management decisions may be prioritised.

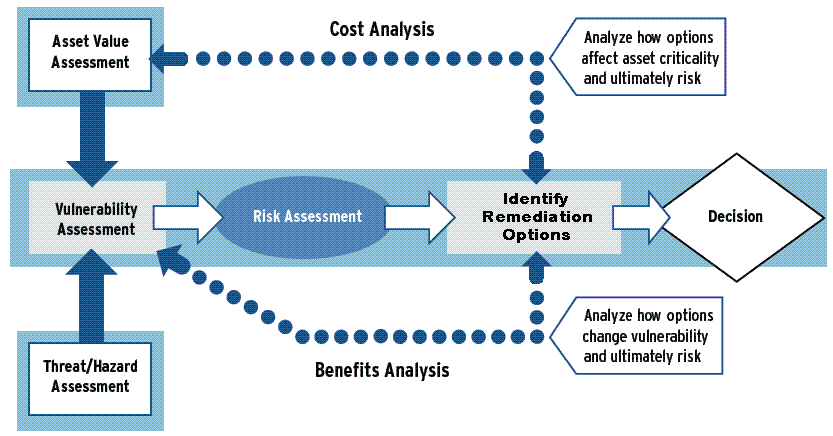

Identify Potential Risk Factors for Critical Processes

Risk identification sets out to identify an organisation’s exposure to uncertainty. This requires an intimate knowledge of the organisation, the market in which it operates, the legal, social, political and cultural environment in which it exists, as well as the development of a sound understanding of its strategic and operational objectives, including factors critical to its success and the threats and opportunities related to the achievement of these objectives.

Risk identification should be approached in a methodical way to ensure that all significant activities within the organisation have been identified and all the risks flowing from these activities defined. All associated volatility related to these activities should be identified and categorised.

Business activities and decisions can be classified in a range of ways, examples of which include:

Strategic – These concern the long-term strategic objectives of the organisation. They can be affected by such areas as capital availability, sovereign and political risks, legal and regulatory changes, reputation and changes in the physical environment.

Operational – These concern the day-today issues that the organisation is confronted with as it strives to deliver its strategic objectives.

Financial – These concern the effective management and control of the finances of the organisation and the effects of external factors such as availability of credit, foreign exchange rates, interest rate movement and other market exposures.

Knowledge management – These concern the effective management and control of the knowledge resources, the production, protection and communication thereof. External factors might include the unauthorised use or abuse of intellectual property, area power failures, and competitive technology. Internal factors might be system malfunction or loss of key staff.

Compliance – These concern such issues as health & safety, environmental, trade descriptions, consumer protection, data protection, employment practices and regulatory issues.

Whilst risk identification can be carried out by outside consultants, an in-house approach with well-communicated, consistent and co-ordinated processes and tools is likely to be more effective. In-house ‘ownership’ of the risk management process is essential.

The identification of the hazards in all aspects of work should be approached by:

walking around the workplace and looking at what could cause harm

consulting workers and/or their representatives about any problems they have encountered. Often the quickest and surest way to identify the details of what really happens is to ask the workers involved in the activity being assessed. They will know what process steps they follow, whether there are any short cuts, or ways of getting over a difficult task, and what precautionary actions they take

examining systematically all aspects of the work, that is:

temporary and part-time workers.

looking at what actually happens in the workplace or during the work activity (actual practice may differ from the policies and procedures manual)

thinking about non-routine and intermittent operations (e.g. maintenance operations, changes in production cycles)

taking account of unplanned but foreseeable events such as interruptions to the work activity

considering long-term hazards to health, such as high levels of noise or exposure to harmful substances, as well as more complex or less obvious risks such as psychosocial or work organisational risk factors

looking at company accident and ill-health records

seeking information from other sources such as:

manufacturers’ and suppliers’ instruction manuals or data sheets

occupational safety and health websites

national bodies, trade associations or trade unions

legal regulations and technical standards.

The identification of all those who might be exposed to the hazards:

For each hazard it is important to be clear about who could be harmed; it will help in identifying the best way of managing the risk.

Account should be taken of workers interacting with the hazards whether directly or indirectly, e.g. a worker painting a surface is directly exposed to solvents, while others workers in the vicinity, engaged in other activities, are inadvertently and indirectly exposed.

This doesn’t mean listing everyone by name, but identifying groups of people such as ‘people working in the storeroom’ or ‘passers-by’. Cleaners, contractors and members of the public may also be at risk.

Particular attention should be paid to:

gender issues and to,

groups of workers who may be at increased risk or have particular requirements:

workers with disabilities

young and old workers

pregnant women and nursing mothers

untrained or inexperienced staff

It is important to identify how these people might be harmed, i.e. what type of injury or ill health may occur.

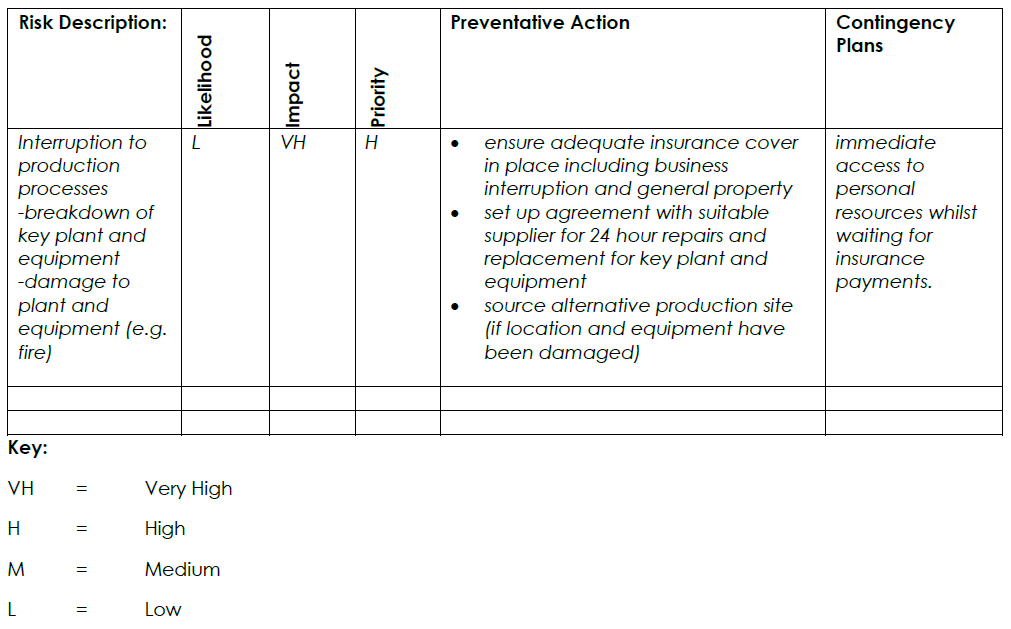

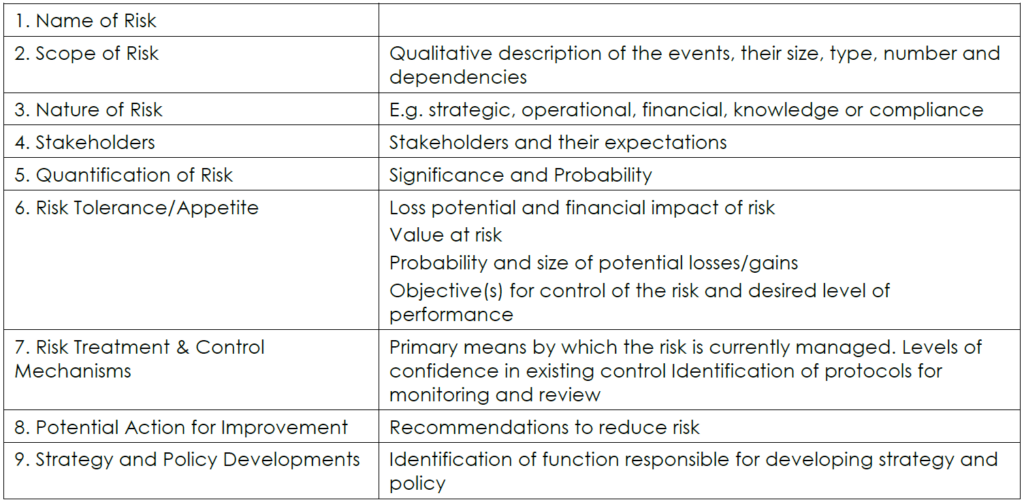

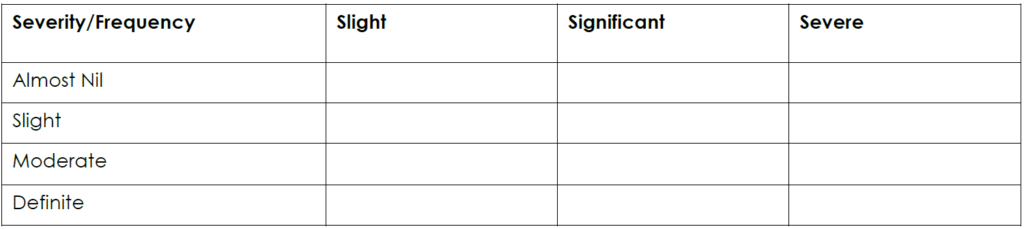

Risk Description

The objective of risk description is to display the identified risks in a structured format, for example, by using a table. The risk description table overleaf can be used to facilitate the description and assessment of risks. The use of a well-designed structure is necessary to ensure a comprehensive risk identification, description and assessment process.46

By considering the consequence and probability of each of the risks set out in the table below, it should be possible to prioritise the key risks that need to be analysed in more detail.

Identification of the risks associated with business activities and decision making may be categorised as strategic, project/tactical, operational. It is important to incorporate risk management at the conceptual stage of projects as well as throughout the life of a specific project / unit.

Methods and Techniques for Conducting Risk Assessment

There are various risk identification techniques that could be used, such as:

Brainstorming

Questionnaires

Business studies which look at each business process and describe both the internal processes and external factors which can influence those processes

Industry benchmarking

Scenario analysis

Risk assessment workshops

Incident investigation

Auditing and inspection

HAZOP (Hazard & Operability Studies)

There are various risk analysis methods and techniques that can be used, such as:

The risk assessment techniques can broadly be categorised into 4 areas:

Issue-based risk assessment – Looks at technical, commercial and managerial aspects and how their risks may impact on the plan. This could include a simple checklist to complete.

Checklist risk assessment – Checklists, whilst simple, in general suffer from drawbacks.

Qualitative risk assessment – Different systems exist like scoring and ranking or the use of high / low / medium assessments of impacts. Scoring requires a degree of subjectivity. As the name suggests, points are awarded according to the perceived degree of risk involved. The points are then totalled and an overall assessment of the risk established.

Quantitative risk assessment – We have already seen many techniques for assessing the impact of two activities with a range of values.

Issue-based Risk Assessment

Issue-based risk assessment has an advantage of being straight forward and generates potential problems largely based upon experience.

Being a method that is based upon previous experience there is a danger that old ground is covered and the obvious areas are investigated:

Opportunities for more creative thinking may be limited.

It is easy to compartmentalise your thinking in the relevant areas of commercial, technical etc and miss the relationships between the departments.

Whilst useful in some circumstances as they are simple you will need to be aware of their limitations.

Good review procedures from previous procedures will provide lessons that may well apply to other projects. You should be aware of these.

This method does not promote creativity and can encourage a narrow approach. Hence, many risks may well be missed.

This risk management method does not allow you to assess the impact of risks in a meaningful way that can be aggregated over the project or at interim points.

The aim is to cover the areas like financial, regulatory, etc. over the project lifecycle.

You would brainstorm each area to try and add some degree of creativity.

This method may just lead to a check list of ‘issues’ without much understanding of them in terms managing your unit’s risks, response and impact on the project / unit.

Checklists Risk Assessment

The checklist is a general result of the ‘issue’-based method of assessment and the typical items to be aware of are:

Can end up concentrating on historical experience perhaps at the experience of new or future risks.

Can be considered as exhaustive with the danger of becoming complacent.

Does not easily assess the total project risk.

In addition:

Interdependence of schedule activities are hard to visualise

Risks identified are not readily prioritised

If it’s not on the list it is likely to be ignored

The list may be orientated to a particular project and miss the experiences of others

Necessary detail may be lacking

Can promote a simple view of risks and the risk management process.

Any checklist used should be considered as an initial help to a more formal project / operational management procedure:

You should be trying to generate a list that is not so long that it becomes difficult to manage or starts to include trivial risks.

As well as looking at the internal risk of activities you should also consider potential external problems.

These sort of check lists tend to generate perceived risks based upon historical events. This is a good thing as you don’t want to repeat yesterday’s mistakes.

However, be aware of trying to encourage the ‘brainstorm’ used to generate the list to consider new and future events.

One problem with a list is that the project management team can see it as exhaustive. Beware of complacency.

This method is not very good at trying to assess the overall impact of risk on the total project / operational management plan.

Qualitative Methods of Risk Assessment

Qualitative methods try to compare ranges in a simple fashion. Specific values are not given to the impacts.

Methods include a simple scoring system and the use of low / medium / high.

Even so, qualitative methods have numerous advantages over the issue based method but there are a few pitfalls in the interpretation of the data.

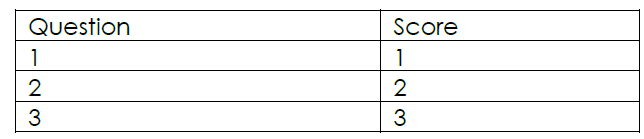

Risk analysis is based upon some form of set question system that tries to attribute a particular value to the impact if the risk materialises. Very simplistically it could be:

- Set up a series of questions. If the answer is yes score as shown, if no score zero.

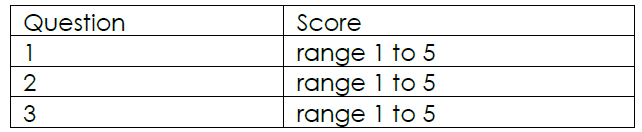

2. Alternatively, a series of questions could be set that require a degree of interpretation and subjectivity to choose a score within a possible range.

- The choice of 1 might be low risk and 5 high risk. Naturally, the questions that you attribute to the project management task could be quite detailed in their description of the level of risk.

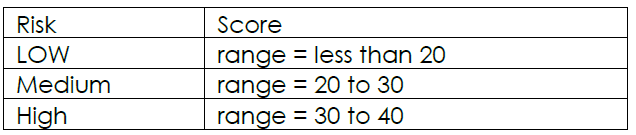

- Eventually, for a given task, the total score is calculated. For example, if the total score is 23 it could be interpreted as:

In this case the risk could be considered to be medium. What medium means in practice would require some agreement within the management team.

The major problem with the ‘score’ based system is that it depends on the individual’s interpretation of the scoring system. It can be too subjective.

In addition, there may be some confusion with the likelihood of the risk occurring and its impact on the project. The risk management system could show a high impact but have virtually no chance of occurring and may therefore not be a problem. You must be aware of this when using these methods.

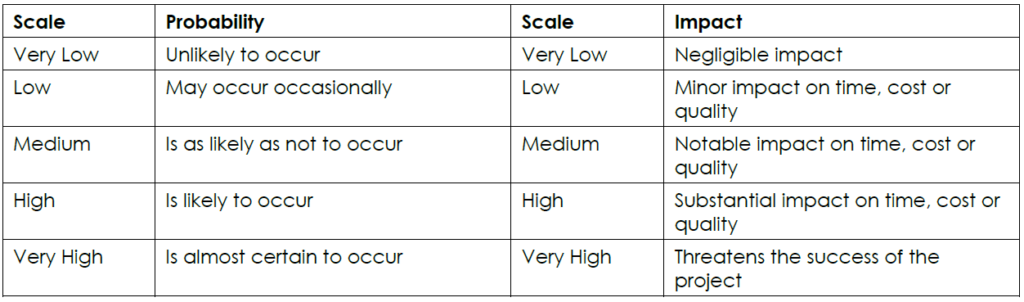

Use enough categories so that you can be specific but not so many that you waste time arguing about details that won’t actually affect your actions. Experience suggests that a five-point scale works well for most projects. A suggested scale is:

Example:

The total risk of the project can be confused with the total score achieved by adding up the individual scores. This is a very simplistic view and is another drawback of this approach.

The risk of individual project management tasks is not additive. Many tasks depend upon others in the schedule.

So, whilst the simple nature of this method may have its uses there are still disadvantages.

In summary:

These methods try simply to determine the size of the effect based upon threshold:

o less than a particular value (safe)

o in between (medium risk)

o higher than a particular value (high risk)

Can be seen as meaningless or subjective

Can confuse likelihood with impact and obscure priorities – may miss new high risk activities

Quantitative Methods of Risk Assessment

This approach is based upon the project / operational management plan (schedule) which has been put together by considering not only all of the individual tasks, but including their relationships.

The qualitative definition of risk is one with which most managers will be both familiar and comfortable. However, at the risk of introducing a degree of circularity into the reasoning, none of this means anything at all in real terms unless you have set some kind of thresholds for your qualitative definitions.

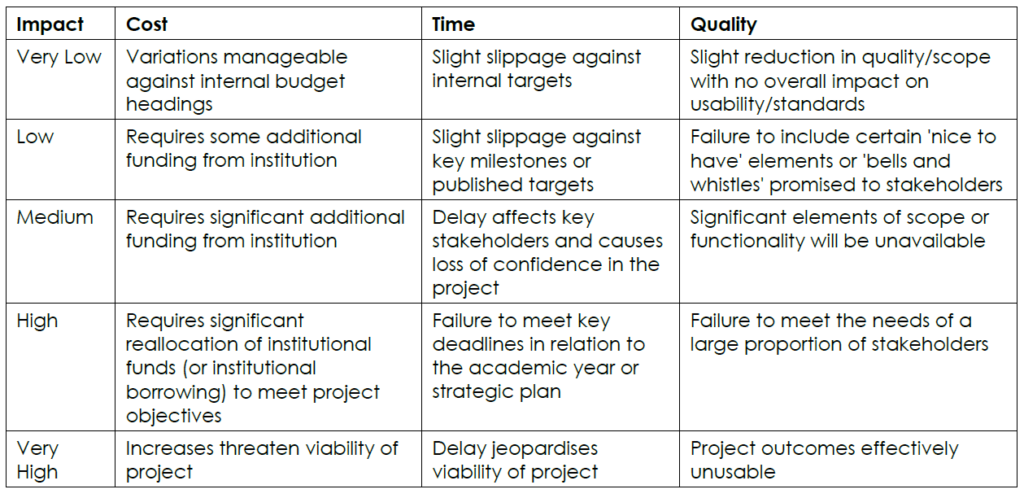

What do we mean by a medium risk? If a risk is likely to cause a five-week delay to your project or cost you R10k where does that sit on the scale of ‘very low’ to ‘very high’ in relation to your particular project? You must do these threshold definitions and understand what are high cost and time implications for your project before you can assess risks in a meaningful way. The following table suggests a general measure of impact in the education environment.

There are many variations on this table. In the commercial world percentage scales are often used for the cost and time components. The scale frequently goes from less than 5% variation (low) to greater than 20% variation (very high).

The risk management process will begin with the summary initial plan and develop the ‘reference’ and base plan (agreed, accepted initial plan for implementation).

It uses data that already exists in assessing the risk of not completing a task and the potential costs.

The units of risk measurement will be the same as for the durations and cost measurements.

This makes it much easier for individuals to gauge the risk and to come to informed decisions.

In summary:

Based upon plans already in use

Uses cost and schedule breakdown information

Measures risk in the same units as task durations and costs

Easily informs decision making for milestone dates and budgets.

Adapted from: www.risk-management-basics.com

Please see Appendix A for notes about how to map information gathered.

Risk Assessment Tools

We will explore a few of the Risk Assessment tools below, namely:

What-if analysis

Checklist of known hazards

Hazard and operability study (HAZOP)

Failure mode and effect analysis (FMEA)

Fault Tree Analysis (FTA)

Ishikawa

Preliminary Hazard Analysis (PHA)

What-if Analysis

Use a what-if analysis to identify specific hazards and hazardous situations. What-if questions are asked about what could go wrong and hazardous consequences are identified and analysed. This type of analysis is a brainstorming activity and is carried out by people who have knowledge about the areas, operations, and processes that may be exposed to hazardous events and conditions.

Checklist of Known Hazards

Use a checklist of known hazards to identify your hazards and hazardous situations. The value of this type of analysis depends upon the quality of the checklist and the experience of the user.

Use a combination of checklists and what-if analysis to identify your hazards and hazardous situations. Checklists are used to ensure that all relevant what-if questions are asked and discussed, and to encourage a creative approach to risk assessment.

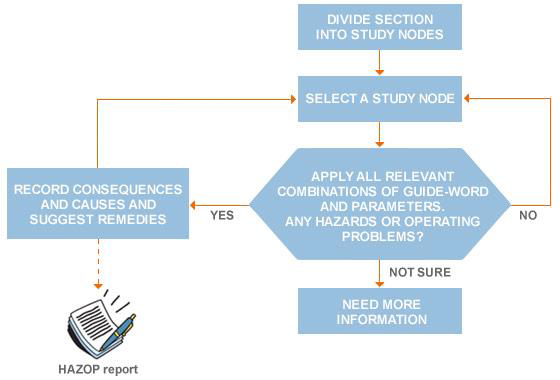

HAZOP

Use a hazard and operability study (HAZOP) to identify your hazards and hazardous situations. If you need to do a very thorough analysis, this method is for you. However, it requires strong leadership and is costly and time consuming. It also assumes that you have a very knowledgeable interdisciplinary team available to you, one with detailed knowledge about the areas, operations, and processes that may be exposed to hazardous events and conditions.

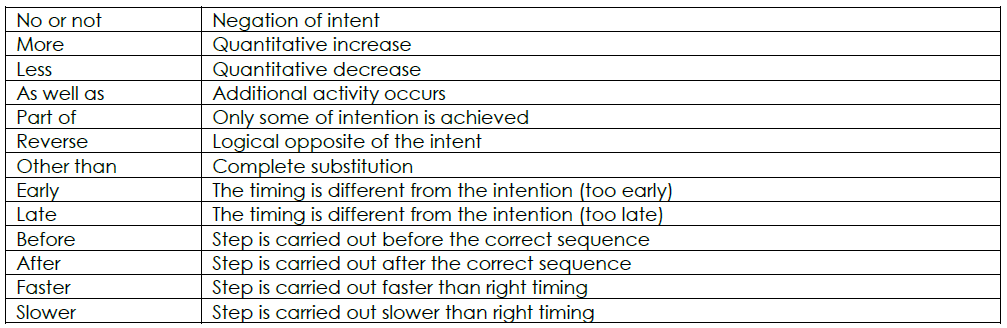

Hazard and Operability (HAZOP) analysis is a technique that allows you to identify and evaluate, caused by deviations from the design or operating intentions problems that may represent risks to personnel or equipment. These deviations are recognised by using so-called “guide-words” applied to process parameters.

The main “guide-words” are listed in the following table.

HAZOP technique was originally developed to study plants and process systems. It also often applied to operators, software and procedures.

HAZOP is realised by using a work-sheet that generally includes the following columns:

ID number

Guide-word

Type of deviation

Potential causes

Consequences

Safeguards/controls

Actions required/recommendations

Responsibility

In order to apply HAZOP technique, process flow and layout diagrams, data sheets and operating instructions should be available.

A HAZOP study is very often used as a systematic technique for identifying hazards or operability problems throughout an entire facility. One (usually a team of people) examines each segment of a process and lists all possible deviations from normal operating conditions and how these might occur.

What deviations could arise?

How can these arise?

What are the implications?

Any surrounding implications?

Example:

A pipe could break, if the supports are not adequate.

Gas will escape from the break.

A massive explosion will ensue.

Damage to plant and surrounding property, risk to life and limb.

A node is a specific location in the process in which the deviations of the design/process are evaluated.

The first step is to collect documents and drawings as mentioned before. After that it is possible to divide the facility into different nodes and for each one evaluate deviations, all potential causes and related consequences, also listing controls and recommendations.

HAZOP studies are very often used in practice and in America it is estimated that half of the chemical industry used the HAZOP technique for all new facilities. The normal time between reviews of existing facilities is 1½ – 5 years and the use of the technique is increasing.

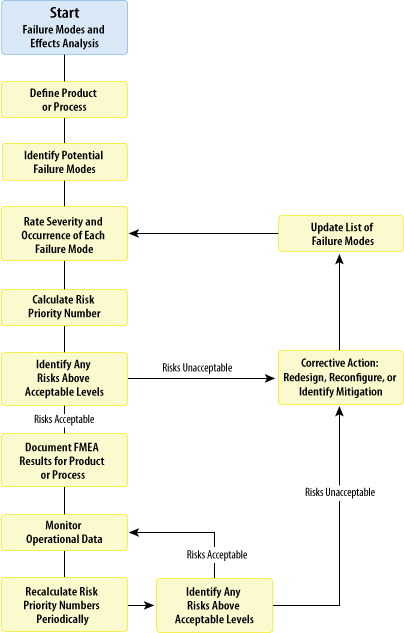

FMEA

Use a failure mode and effect analysis (FMEA) to identify potential failures and to figure out what effect failures would have. This method begins by selecting a system for analysis and then looks at each element within the system. It then tries to predict what would happen to the system as a whole when each element fails. This method is often used to predict hardware failures and is best suited for this purpose.

Key concepts which characterise FMEA and define the risk are:

Function (or process step) – the task that the system, design, process, or service must perform

Failure – functional defectiveness that does not meet the customers’ requirements. It is the inability of the system to perform based on the design intent

Failure mode – the physical description of the manner in which a failure occurs

Cause of failure – the root cause of the listed failure

Effect of failure – the outcome of the failure of the function from a local or global point of view.

Current controls – implemented controls to prevent causes of the failure from occurring

In order to categorise and prioritise risk level three parameters need to be defined:

Severity – it indicates the seriousness of the effect (consequences) of the failure mode

Occurrence – it represents the estimate number of failure that could occur for a given cause

Detection – it corresponds to the likelihood that the proposed control will detect a specific cause of a failure

Risk priority to identify a corrective action implementation order is calculated through combination of these three parameters after defining a threshold of risk acceptability.

FMEA/FMECA is frequently used in combination with other techniques to reach multiple benefits, e.g. in order to identify causes of failure a specific Fault Tree Analysis (FTA) can be developed.

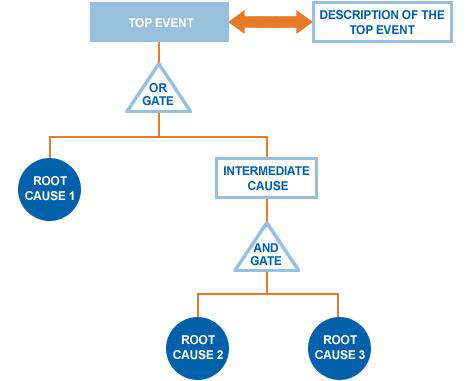

Use a fault tree analysis (FTA) to identify all the things that could potentially cause a hazardous event. It starts with a particular type of hazardous event and then tries to identify every possible cause.

Main steps for build FTA following:

- System definition: the definition of the system is essential to understand the environment and the process involved in the system itself and can be obtained using a mapping technique.

- Top event identification: the top event must be clearly and unambiguously identified together with the definition of the boundaries that edge the analysis.

- Tree development: the tree is developed by the definition of the events and conditions that can generate the defined top event, the connection of these events by logic gates, proceeding until the appropriate level (i.e. the level where root events are independents or where no data exist for that event).

- Fault tree evaluation: the evaluation of a fault tree is based on the identification and classification of minimal cut sets, i.e. the minimal set of root events whose simultaneous occurrence ensures that the top event occurs.

- Top event probability estimate: the estimation is based on statistical calculations that combine the probability of failure of the different basic events.

ISHIKAWA

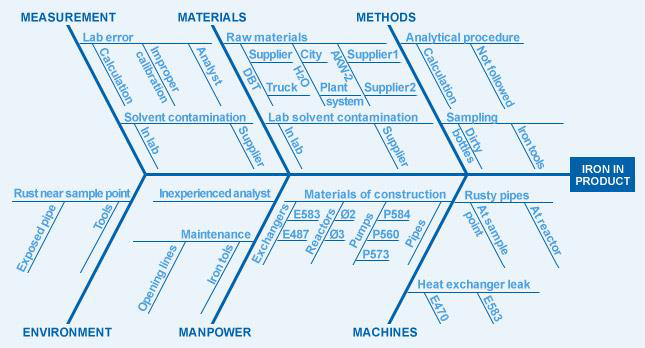

This technique was developed in 1969 by Kaoru Ishikawa, who pioneered quality management processes in the Kawasaki shipyards, and in the process became one of the founding fathers of modern management.

The Ishikawa diagram, also called “Fishbone” or “Cause-and-Effect diagram”, is a graphic tool used to identify potential causes (i.e. sources of variation in a process) for an effect or a problem.

It is most effective if made by a team (brainstorming) rather than by individuals and is used for product design and quality defect prevention.

The potential causes identified by the team are usually grouped into categories that identify sources of variation. Generally these categories could be the 6 M’s:

MAN: personnel involved in process

MOTHER NATURE: environmental conditions

METHODS: procedures, instructions, etc.

MACHINES: equipment

MEASUREMENTS: data generated from the process

MATERIALS: anything used in the process

The problem of interest is inserted on the right of the diagram at the end of the main “bone”. The identified categories related to the problem are drawn as bones off the main backbone. Brainstorming is typically done to add possible causes to the main “bones” and so on. This subdivision into ever increasing specificity continues as long as the problem areas can be further subdivided. The practical maximum depth of this tree is usually five levels.

PHA

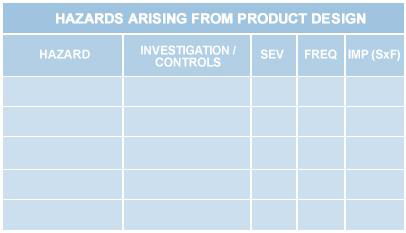

Preliminary Hazard Analysis (PHA) is based on exploiting prior experience or knowledge of a hazard or failure to identify future hazards, hazardous situations and events that can cause harm and estimate their probability of occurrence for a given activity, facility, product or system.

The objective of the PHA is to identify as early as possible the main hazards and accidents that may arise during the life of the product.

After hazard identification and quantification in terms of severity and frequency of the event / consequence, it is necessary to associate a possible remedial measures to reduce risk in an acceptable area.

This technique can be used as initial risk assessment either when the analysed system is not yet clearly defined or when exhaustive information is not available. It can be useful when analysing existing systems or prioritising hazards where circumstances prevent a more extensive technique from being used.

Hazard identification can be made through:

- Evaluation of similar systems

- Review of other hazard analyses (for similar systems)

- High level risk assessment