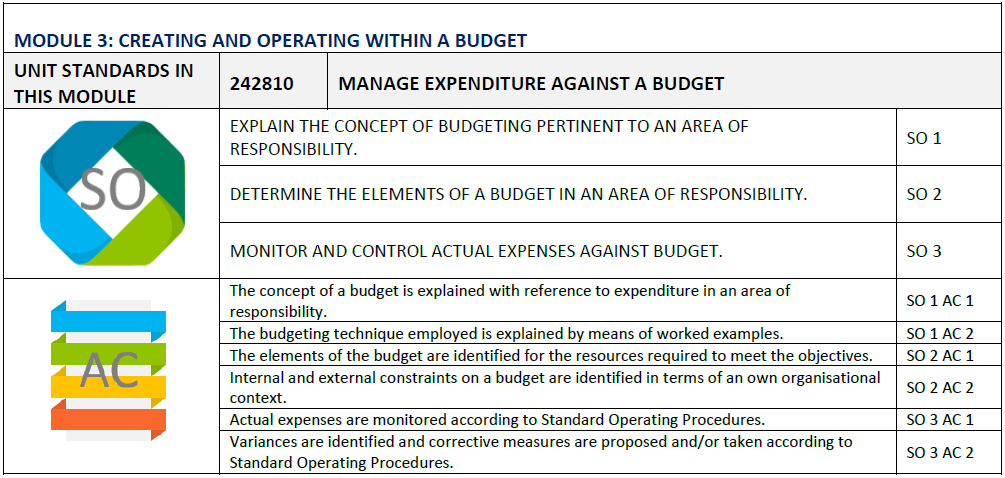

Developing and managing budgets in a business environment

MANAGE EXPENDITURE AGAINST A BUDGET

Budgeting is an art as well as a science. Often, one does not have enough money to do everything one wants. Therefore one has to prioritise those activities and expenses in order of importance. The art of budgeting is in squeezing the most out of available funds, so that as many objectives are attended to as possible.

A good budget realistically assesses expected incomes and expenses and is a tool that you can use to reach certain financial targets.

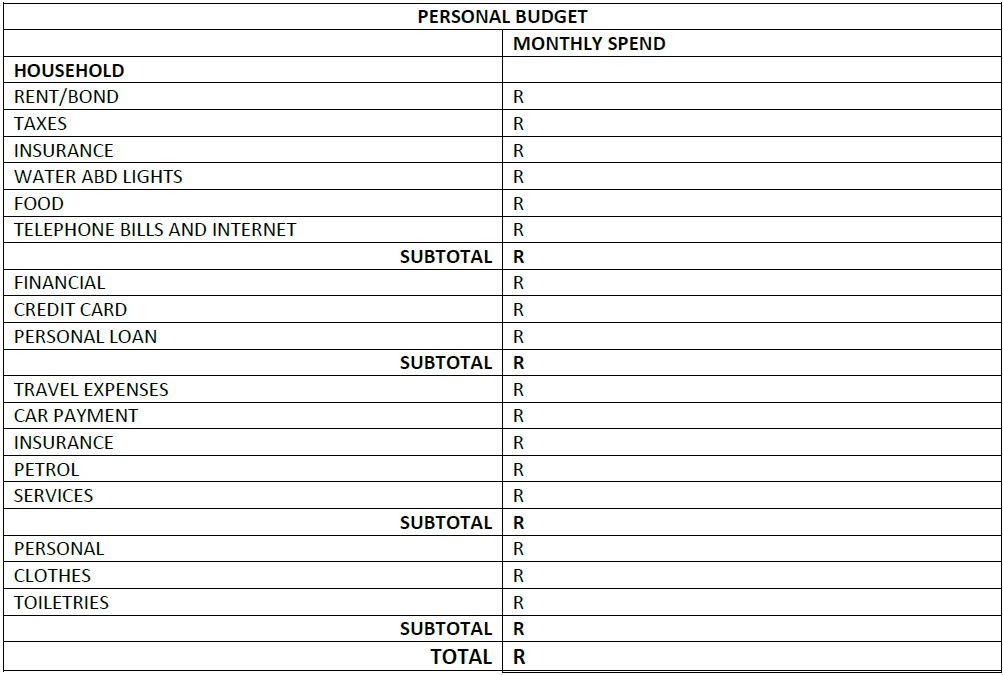

Personal Budget

The majority of people complain about being broke most of the time. This situation can be ascribed to lack of or poor personal financial management. This situation can be corrected by the drawing up of a personal budget and spending your income according to it.

Corporate Budget

Budgeting is a time-consuming process which may, depending on the company, involve all levels of the corporate hierarchy: from hourly wage earners, through supervisors and middle-level managers, to vice presidents, presidents and CEOs. Budgeting is only one aspect of corporate planning. Only after a discussion of corporate planning can budget be discussed in its proper place.

Corporate budgets have a wide variety of uses, all of which serve one main purpose: to save money and increase profitability. Money saved by a company can be used for a variety of purposes. For example, a corporate budget can help predict the money gained through sales which will then be useful in the determining the availability of funding for research and development during the same time period.

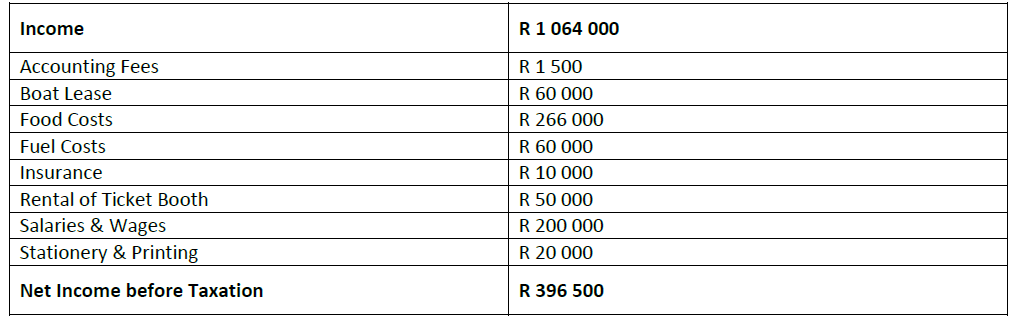

Chicken Ferries cc Budget for the year ended 28 February 201X

Advantages of Budgeting

Corporate (as well as non-profit and government) budgeting:

– coordinates activities of the various departments or divisions within an organisation.

– allows evaluation of performance based on prior guidelines.

– allows control of the working environment.

– allocates resources based on prior corporate planning.

– forces all levels of management to devise a cogent plan of operations.

The planning and budgeting processes are highly dynamic. Review of plans at ever higher management levels allows a stream of input and revisions to adequately reflect the needs of the various departments or divisions within the organisation.

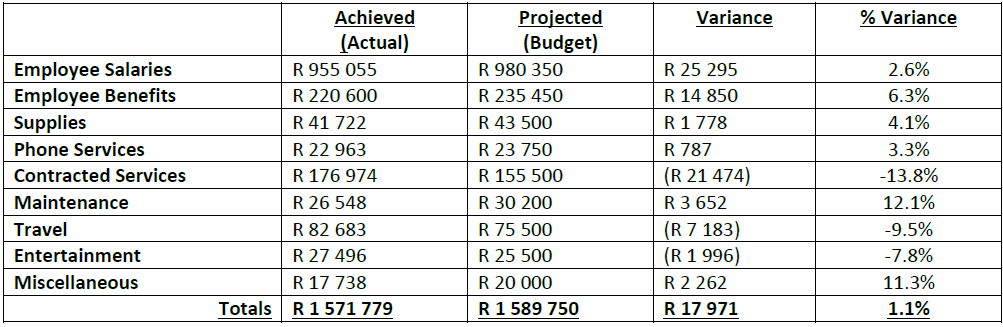

Budget Variance and Performance Reports

Budget variance is the difference in the projected budget and the achieved budget, and is usually expressed as a percentage. Analysis of budget variance allows such discrepancies to be identified and serves as the basis for corrective actions.

A comparison of projected and achieved budgets is stated in a performance report. Performance reports are usually compiled and released on a quarterly basis but may be done so more often.

Example:

Sales Department Performance Report of Controllable Expenses

(for Current Quarter):

Notice the Projected Budget for each category of expense. These represent the target amounts after extensive budget planning.

There were three areas over budget where losses were incurred:

– contract services (- 13.8 %).

– travel (- 9.5 %).

– entertainment (-7.8 %).

It is the function of the department manager to investigate these variances with an eye toward correcting them. The overall budget, however, did produce a surplus (R 17,971 or 1.1 % of the projected budget).

When we use mathematics to plan and control budgets, we must ensure that:

– Plans describe projected income and expenditure realistically.

– Calculations are carried out using computational tools efficiently and correctly and solutions obtained are verified in terms of the context.

– Budgets are presented in a manner that makes for easy monitoring and control.

– Actual income and expenditure is recorded accurately and in relation to planned income and expenditure. Variances are identified and explained and methods are provided for control.

Explain the concept of budgeting

After completing this section, the learner will be able to explain the concept of budgeting pertinent to an area of responsibility, by successfully completing the following:

– The concept of a budget is explained with reference to expenditure in an area of responsibility

– The budgeting technique employed is explained by means of worked examples

Budgeting is the process of planning financial activities for an upcoming accounting period, usually a year. It requires analysing how a business is currently performing and setting objectives for improving its future financial health. Specific revenue and expense expectations are identified with the intention of increasing a business’s profits while keeping expenses in check.

In some organisations the preference is for ‘top-down’ budgeting: Budgets are imposed by top managers with little or no consultation with lower-level managers. Most companies however prefer the process of “bottom-up” budgeting: Budgets are prepared by those who must implement them. The budgets are then sent for approval to higher level managers.

Supervisors have a more intimate view of their needs that do managers at the top, and they can provide realistic breakdowns to support their proposals.

The company procedures and roles for budgeting are as follows:

– Senior Management is responsible for setting goals and developing the strategic intent of the business. This may result in the design of a financial budget to provide for assets required for the long term development and the master budget.

– Operational Management must follow these goals set out in the annual business plan to develop the operational budget.

– Divisional/Departmental Management must follow the business plan to compile the divisional or departmental budget.

IMPORTANCE OF BUDGETING

IMPORTANCE OF BUDGETING

In order to strengthen a business’s financial health, budgeting is necessary. Since the financial activities of a business can become quite complex, a budget is needed to outline a plan that managers and employees can follow. Budgeting provides the structure that is required in order to implement effective pricing and spending efforts.

Budgeting offers five main benefits:

- Budgeting facilitates planning

Planning is the main key to budgeting. A business that plans its future financial activities is one that will have a vision for success. Budget planning requires a business to articulate its vision for the future and how it will accomplish it. Strategies are developed, and deadlines are identified to accomplish the established budget.

The planning aspect of budgeting also helps a business establish benchmarks that it can use to measure its progress toward achieving its financial objectives. - Budgeting enhances communication

Budgets communicate the spending and sales expectations of the managers and employees within an organisation. Communication is enhanced when the individuals responsible for enforcing and meeting financial expectations can find these guidelines in a budget. Managers and employees know what their boundaries are for the upcoming accounting period and can adjust their spending and sales activities accordingly. - Budgeting reinforces accountability

Since budgets are communicated to those individuals responsible for implementing them, accountability is reinforced. The responsible managers and employees can be consulted if any deviations from the budget occur. Budgets enable accountable individuals to make wise financial decisions by giving them the information they need. - Budgeting identifies problems

Budget planning requires a business to identify any financial problems that are developing. Since a budgeted financial statement is broken into months or quarters, deviations from the budget can alert members of management to potential problems. Assigning specific numbers to financial expectations helps draw attention to situations the business needs to investigate. - Budgeting motivates employees

The clear guidelines that are outlined in a budget provide a method by which managers and employees can be rewarded for their efforts. It is easy to evaluate managers’ and employees’ performance by identifying whether the financial objectives articulated in the budget are met. The compensation that individuals will receive if they meet the financial expectations in the budget will motivate them to adhere to it.

THE BUDGETING APPROACH

There are two basic approaches to budgeting:

- The centralised approach utilises the business acumen of an organisation’s top managers and officers to set the budgetary parameters. This approach promotes consistency, but allows little, if any, input from lower echelons of the organisation.

The centralised approach seems to work best in smaller companies where management is completely versed in all aspects of the business. - The decentralised approach allows participation of all management and employee levels. Information and ideas flow upward, but this approach is rather time-consuming and costly, usually involving numerous revisions.

One major advantage of the decentralised approach is that employees who have some input in determining the overall direction of the organisation are more likely to have a greater stake in its success. In addition, those employers closer to customers or suppliers may be more aware problems or concerns that need to be addressed.

Many organisations use a combination of the centralised and decentralised approaches. In effect, this method begins from the centralised, top-down approach and allows detailed input from various levels of the organisation.

Yearly budgets are normally finalised within 30 to 60 days of the end of the fiscal, or calendar, year for the next year (the planning process is described in more detail in Module 2).

Budgets, however, can be prepared by a continuous budgeting approach on a monthly, or more usually, a quarterly basis. With this approach, a budget is revised and extended for another quarter. A company will have a budget nine months ahead at the end of the quarter. The importance of quarterly reappraisal of budgetary aims is that it allows corporate or market changes to be incorporated into the budget four times a year rather than just once a year.

The managers of most units are directly responsible for certain financial aspects of the unit’s budgetary activities:

– Cost responsibility – only responsible for costs incurred.

– Revenue responsibility – primarily responsible for producing revenue.

– Profit responsibility – primarily responsible for both cost and revenue and to generate a profit.

A budget is a translation of your business plan into “numbers.” In its simplest form a budget is a detailed plan of future income and expenditures – a projected profit and loss statement.

Right from the beginning you can use your budget to validate the activities you have planned for the coming year:

– Will you be able to afford additional staff?

– Do you need to expand your facilities or equipment?

– When will be the best time to start your new sales campaign?

– Do you have a period where sales are slow and making ends meet is a challenge?

Knowing what all your business activities will cost and when such expenses will occur will help prevent any unexpected surprises that could lead to financial problems.

Once the period for which you have budgeted is completed, you can then compare actual results with anticipated goals. Get into the habit of making this a regular part of your business routine. You don’t have to do anything elaborate– just a simple comparison of your budgeted figures to your actual results. Then begin by asking yourself “why” are the figures different.

– If some of your expenses, for example, are higher than you expected, do you need to look for ways to cut them or has business increased?

– If your sales aren’t on track, what has happened to cause the difference?

Don’t fall into the trap of “blaming it on a bad budget.” Use the information constructively and improve your budget the next time around.

A manager would prepare a budget to determine whether he/she can achieve their profit goals. To do this, you must project your fixed costs and your variable costs. From these three figures — targeted profit, fixed expenses, and variable expenses — you can determine your required level of income.

– Many businesses start with a forecast of profits and work up to a forecast of sales.

– Even large corporations can determine the required return on investment that shareholders require, then work back to planned revenue goals.

– Alternatively, you can start with a sales forecast, but don’t forget the bottom line must still give you the required return.

EXPLAIN THE CONCEPT OF A BUDGET

A budget may be defined as a business’s financial plan that tells how resources will be acquired and apportioned in operations during a specific period of time (usually a one-year period).

A budget includes detailed financial statements and supporting schedules that project expected dollar amounts (usually by monthly or quarterly periods).

Budgeting allows a company to be cost effective by carefully monitoring operating expenses.

Weekly, monthly, or quarterly monitoring of budget projections through performance reports allows a company to take corrective measures on short notice where and when necessary.

Income and Expenditure

Every business will have money coming in and money going out. These transactions must be recorded and controlled. Before we consider the methods of control, let’s first have a look at some of the transactions that are classified as Income:

– Sales

– Rentals from property

– Interest received from Investments

– Money received from Debtors

– Discounts received

A business will receive most of its income from the sale of its products. Other sources of income may vary according to the type of business and the amount of capital/money available for investment etc.

Income – For the purposes of this module, income is defined as money that has been made within the time period of the statement. It is an important accounting concept to correctly account for income within the time period of the financial statement. This means that you should include in your income calculation money that you have made but not yet received. For example, if you were a trader and sold goods but had not yet received the money (because you had given your customer some credit terms) you should nonetheless include the sale as income for the period, even if the customer only pays you after the end of the period.

Expenditure – For the purposes of this module, expenditure is defined as the costs that have been incurred within the time period of the statement. As with the concept of income, you should accrue for expenditures incurred within the time-period even if you have not paid for them. If, for example, you were doing a household income and expenditure statement for the end of September and you had not received your water and lights account, nor paid it for September, you should nonetheless include it (or a reasonable estimate) in the income and expenditure statement for September. This ensures that you have an accurate statement of the real expenditures incurred within the period. Now, let’s have a look at a few transactions that would be classified as Expenditure:

Payment of Rentals

Payments to Suppliers

Tax

Salaries and Wages

Vehicle expenses

Telephone and Postages

Licences

Obviously there may be many more payments, but they would also vary according to the type of business.

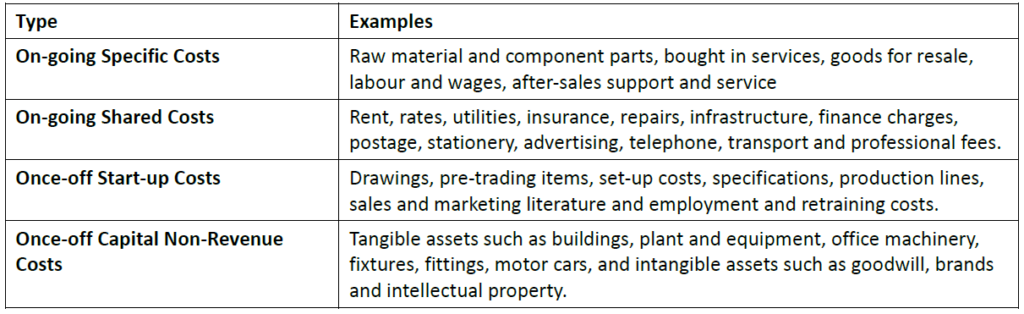

There are a number of different types of expenditure that need to be considered for a budget:

Ongoing Specific Costs – On-going specific costs are costs that are driven by particular products and services, e.g. raw material and component parts, bought-in services, goods for resale, labour and wages, after-sales support and service.

Ongoing Shared Costs – On-going shared costs are those that are shared by the whole organisation and are incurred by most organisations all the time on a routine basis. They can be easily estimated and controlled, e.g. rent, rates, utilities, insurance, repairs, infrastructure, finance charges, postage, stationery, advertising, telephone, transport, and professional fees.

Once Off Start-Up Costs – Start-up costs are those that are incurred when starting or growing a new operation – these costs will vary each time, e.g. drawings, pre-trading items, set-up costs, specifications, production lines, sales and marketing literature and employment and re-training costs.

Once Off Capital Non-Revenue Costs – Capital or non-revenue costs are one-off items. They are usually harder to estimate because they do not happen often – hen they do, they are likely to be different each time, e.g. tangible assets such as buildings, plant and equipment, office machinery, fixtures and fittings, motor vehicles and intangible assets such as goodwill, brands and intellectual property.

EXPLAIN THE BUDGETING TECHNIQUE EMPLOYED

Budgeting or setting a budget is the process of setting financial standards and targets for an organisation’s activities and agreeing them with individual managers who are responsible for the various budgets.

A budget is a bit like a road map: it sets out what direction we are going in and what route we are taking. It also tells us how many miles we will have to travel to get to our destination; we can also see when and how far, we have gone off the track.

So, the budget is a way of measuring the progress towards the achievement of the company’s overall objectives/goal and mission. For this reason, all departments within the organisation will be asked to participate in the preparation of the budget.

For a company’s budget to succeed there must be the approval and support of senior management. This is the point at which the budget becomes the guiding principle for the business. Senior management should make their support for the budget as visible as possible in order that those with the task of putting the budget into action know that their successes will gain the approval of their bosses. Their failures will also gain the bosses attention. Both of these are motivational in their own way.

The objectives of any budgeting system are as follows:

To set the goals and objectives of the business and to write them in terms so that management and budget holders are clearly aware of their responsibilities and limits of authority.

To calculate and draw up an agreed set of standards by which each department agrees to be measured

To agree the process that will measure the efficiency and effectiveness of the company

To show any variances; this will be the basis for deciding what action to take when the business is seen to be off the track.

There are different budgets and budgeting techniques used in most organisations. There are various types of budgeting techniques (e.g. forecasting based on historic data, and zero-based budgeting) that are available to a leader / manager to create a budget. Some of these techniques are often combined and customised to suit the needs of the organisation:

The Fixed Budget

As the name suggests, a fixed budget is for a fixed period and for a fixed amount of income and expenditure. Normally given for a year at a time, the fixed budget sets out the allowed total expenditure by month, quarter or whatever. This is then compared in detail to the actual expenditure. Monthly variances and cumulative variances are listed. A somewhat rigid system, it normally doesn’t take into account changes in activity or other factors affecting the financial results of the business.

The Flexible Budget

Using this system recognises the relationship between activity, fixed costs and variable costs. Accordingly, the budget, or at least certain items within the budget, are increased or decreased to take into account the increase or decrease in activity. For example: If a company’s sales increase by 8%, then the knock-on effect on distribution – transport, warehousing and packaging – is calculated pro-rata or to an agreed formula so that the departmental budgets are increased to finance the extra workload.

The advantage of a flexible budget is that the manager can explore more accurately the underlying reasons for the variations from original budgeted expectations.

Rolling Budget

This is not really a budgetary system in that it is more a method of updating the current budget on a continuous basis. The current budget may be for a 12 month period. It is considered active. Each month or quarter the budget is projected for a further twelve or maybe even an eighteen month period, depending on what management feel is appropriate. So, if the budget is split into quarters, then as quarter one is finished for that first year, so quarter one will be calculated for the following year. There is an advantage to rolling budgets and that is that they get away from the fixed budget type of thinking. This means that management do not and cannot take their eyes off the ball.

Static Budget

This variation on the traditional budget addresses the problem of budget rigidity in a somewhat different manner. The traditional model, a static budget, presents one set of forecasted numbers for a given time period and is not changed during the life of the budget.

Historical-Base Budgeting technique

Historical-base budgeting is the process of basing your objectives for the upcoming accounting period on the previous one’s actual performance. Some individuals automatically use the previous accounting period’s performance as the budgeted amount for the upcoming period.

The problem with this budgeting method is that consideration is often not given to whether the previous accounting period’s performance was good or poor. If the financial activities from the previous accounting period were inadequate, using these figures as a guideline for the upcoming accounting period will simply prolong poor performance.

Historical budgeting assumes:

– that all current expenditures are necessary and

– that only the amount of budget increase needs to be substantiated.

Zero-base budgeting technique

Zero-Base Budgeting (also known as priority based budgeting) re-evaluates all items of the budget each time a budget is created. This differs from historical (or incremental) budgeting which is based on increasing the current budget by a percentage amount (usually one that takes inflation into account). The historical budgeting process may be flawed because certain of the current budget’s expenses may not be justified. Zero based budgeting eliminates the ‘add-on’ assumed characteristics of historical budgeting.

With zero based budgeting, all expenditures are re-evaluated for each budget created. This method requires that each budget justifies a programme or expense or department’s existence each time a budget is prepared. Should the programme or expense or department’s existence not be justified then it could be eliminated or downscaled to budgetary constraints.

Zero-based budgeting involves four steps:

- Describe each separate organisational activity in a budget

- Evaluate and rank these activities in terms of a cost-benefit analysis

- Allocate funds as appropriate

- Monitor and Evaluate

Activity Based budgeting technique

Activity-based budgeting is a new way of approaching the budgeting process. Under traditional cost allocation, overhead costs are allocated to products using cost drivers such as direct labour hours and machine hours”. However, “activity-based budgeting (ABB) concentrates on the cost of resources required for producing and selling products and services.

– The main advantage of activity-based budgeting is that costs are more accurately associated with activities, making the budgeting process more accurate and effective.

The main disadvantage of activity-based budgeting is that it can be costly and complex to establish.

Note: Most organisations combine Zero-base and Activity-based budgeting techniques to create their budgets

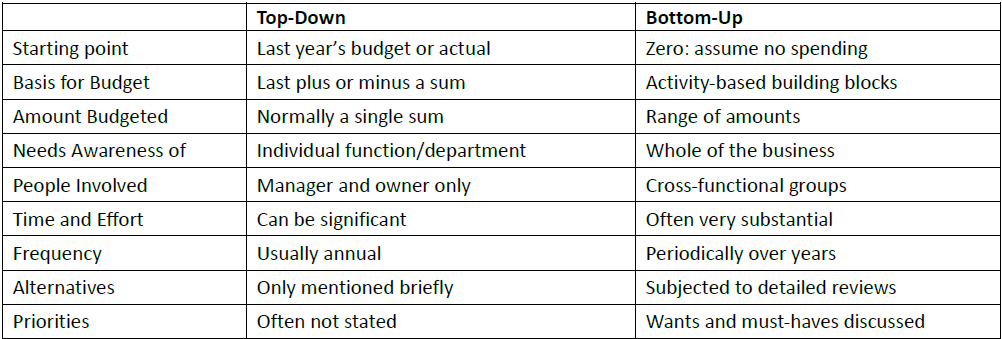

Top-Down Budgeting

In some organisations the preference is for ‘top-down’ budgeting: Budgets are imposed by top managers with little or no consultation with lower-level managers.

In this method senior management set the budget goals and inflicts these goals on the company. Senior management may have set rigid and specific objectives for budgeted items. This is a very simple method that works out what was spent the previous year and then a percentage is added or subtracted for the current year.

The problem with this is that the figures from last year may be incorrect and it is very unlikely to give the best possible resource allocations. It may also miss hidden gradual cost changes and can be responsible for inefficient practices. However, top-down budgeting is still the most common way to produce budgeted figures. Often a manager will have had the budget forms in the in-tray for several weeks, and yet, by using this approach, can still produce a budget in one day without any reference to any other part of the business.

In certain cases senior management may set ‘stretch’ or ‘challenge’ profit goals that seem almost impossible to achieve, leaving the lower level management to figure out how to attain them.

Companies use these ambitious budget goals as motivational tools; however, the results may vary, either an energetic management team will discover creative new solutions or a very discouraged management team may simply give up. The midpoint is the preferred target, revenue or profit goals that would allow enough flexibility for both positive and negative possibilities.

Bottom-Up Budgeting

Most companies however prefer the process of “bottom-up” budgeting: Budgets are prepared by those who must implement them. The budgets are then sent for approval to higher level managers. Supervisors have a more intimate view of their needs that do managers at the top, and they can provide realistic breakdowns to support their proposals.

In companies that do bottom-up budgeting, managers do not receive specific targets as with the Top-down method. Instead they begin by putting together budgets that they feel will best meet the needs and goals of their departments. These budgets are then ‘rolled up’ to create an overall company budget, which is then adjusted, with requests for changes being sent back down to the individual departments.

This system means that you have to justify all expenditure, from the group up. Bottom-up budgeting is best suited for discretionary and support costs, such as marketing costs, rather than tangible costs (easily measurable costs) such as production costs.

Bottom-up budgeting is very time consuming. The process can go through many interactions. Often it means working closely with other departments that may be in competition with yours for limited resources. It is best to be as co-operative as you can with these departments during this process, but that doesn’t mean you shouldn’t lobby aggressively for your own department’s needs.

Let’s now have a look at a comparison between Top-down and Bottom-up Budgeting:

THE MASTER BUDGET

There is only one master budget. All smaller budgets within the business are only part of that budget which is the financial model of the organisation. There is no limit to the number of smaller budgets that a company may draw up, but usually budgets are drawn up by function and/or organisational requirements. Let’s have a look at what the Master budget is made up of:

– Sales Budget: will include product budgets

– Production Budget: will include Materials, Labour, Expenses and Plant Utilisation budgets

– Marketing Budget: will include budgets for Advertising, Marketing and Promotion

– Distribution Budget: will include budgets for Transport, Warehouse and Packaging

– Administration Budget: will include budgets for Personnel, Accountancy, Occupancy and Office.

Let’s now go into a bit more detail for two of the budgets mentioned:

The Sales Budget

It is well known that a Sales budget is the most important budget within a business, but it is difficult to accurately project unless you are playing Monopoly. This may be true, but all companies still have to estimate what number of products or services will be sold. The person responsible for the Sales Budget would be the Sales Director. The Sales Director would, in turn consult with the area managers and both directly and indirectly with the Sales team or teams.

It is not enough to take last year’s budget and add on, say 10% to cover inflation. If budgeting is to be professional, then we need to take into account some or all of the following information:

- The sales objectives of the organisation, including the possibilities for growth, new markets and areas and new product introductions

- Financial analysis of past performance, split into product groups and/or sales representatives and/or customers

- Current information regarding the ability of the organisation to fulfil its objectives.

- External information, such as environmental issues, trading patterns and market research etc.

The Cash Budget

One of the more important budgets is the cash budget. This would be drawn up by the Financial Controller or Accountant within the business. A company’s ability to survive in the short term is its ability to have sufficient cash resources to meet all its debts – such as loan repayments. The shortfall of funds may have to be financed by overdraft or other borrowings; surplus funds will need investing so that the money is working for the company. The cash budget therefore is an action plan for management which warns when there are periods of shortfalls or surpluses of funds which will enable management to take further action.

So far we have looked at the different types of Budget and the methods of budgeting. Let’s now look at how they fit together.

The company may have specific budgetary needs in relation to the business plan. If a highly accurate and detailed budget is required, such as at a company start-up, the activity-based format will be required; in other cases an incremental budget may be sufficient.

DETERMINE THE ELEMENTS OF A BUDGET

After completing this section, the learner will be able to determine the elements of a budget in an area of responsibility, by successfully completing the following:

– The elements of the budget are identified for the resources required to meet the objectives

– Internal and external constraints on a budget are identified in terms of an own organisational context

So far we have looked at the different types of Budget and the methods of budgeting. Let’s now look at how they fit together.

The company may have specific budgetary needs in relation to the business plan. If a highly accurate and detailed budget is required, such as at a company start-up, the activity-based format will be required; in other cases an incremental budget may be sufficient.

Budgeting and the Business Plan

Each business will have a Business plan – this is the vision of where the organisation would like to be in say, three to four years’ time. This plan would include the setting of overall objectives so that the business can determine what it hopes to achieve.

So the business needs to analyse the environment in which it operates and the resources that it has, using the SWOT Analysis – an assessment of the business strengths, weaknesses, opportunities and threats.

The budget is the planned carrying out of the business plan. It is incorporated in both the business planning and control processes. The senior management of the business choose the considered options that will have the greatest chance of achieving the objectives of the business and create long-term plans to implement those options.

A business must be able to do the following:

– Tell the money where to go and not worry about where it went

– Make sure the business has clearly thought out long-term plans and strategies

– Consider the market trends of their products (Will it sell and how many will sell, at what price)

– Use budgets to judge performance and as an authority to spend.

Business Plan

The business plan is a written summary of what a business hopes to accomplish by being in business and how it will accomplish its objectives. It contains clear goals and objectives with an explanation of the business intends to manage all of its resources i.e. premises, equipment and staff, as well as finances, in order to achieve those goals and objectives.

The business plan should be seen as part of the planning process. It can never be complete because a number of factors can make it immediately out of date. These factors may include late payment by customers, or increased or unforeseen costs. The list may be endless.

The formal business plan should be seen as an important management tool by all businesses irrespective of size. It serves four critical functions:

– It helps clarify, focus and research the development of the business

– It provides a framework for the business strategy to be undertaken in order for the business to develop

– The document can be used as a basis for discussion with third parties who have either a potential or an existing interest in the business such as shareholders, banks or other investors

– It sets goals and objectives against which actual performance can be measured and reviewed.

The budget is a way of measuring the progress towards the achievement of the goals within the business plan. It is therefore important that you review your departmental business to compare actual results with ideal results and then prepare a budget plan to close that gap.

The objectives set out in the Business Plan are broad based to give the business direction; they are not specific enough for department use. Your department objectives need to be activity based, taking into account the resources needed such as time, people, equipment and finances etc. Remember that the strategic plan sets out the major long-term business and financial plans for the organisation and is the basis on which you will set your department’s objectives.

Budgets

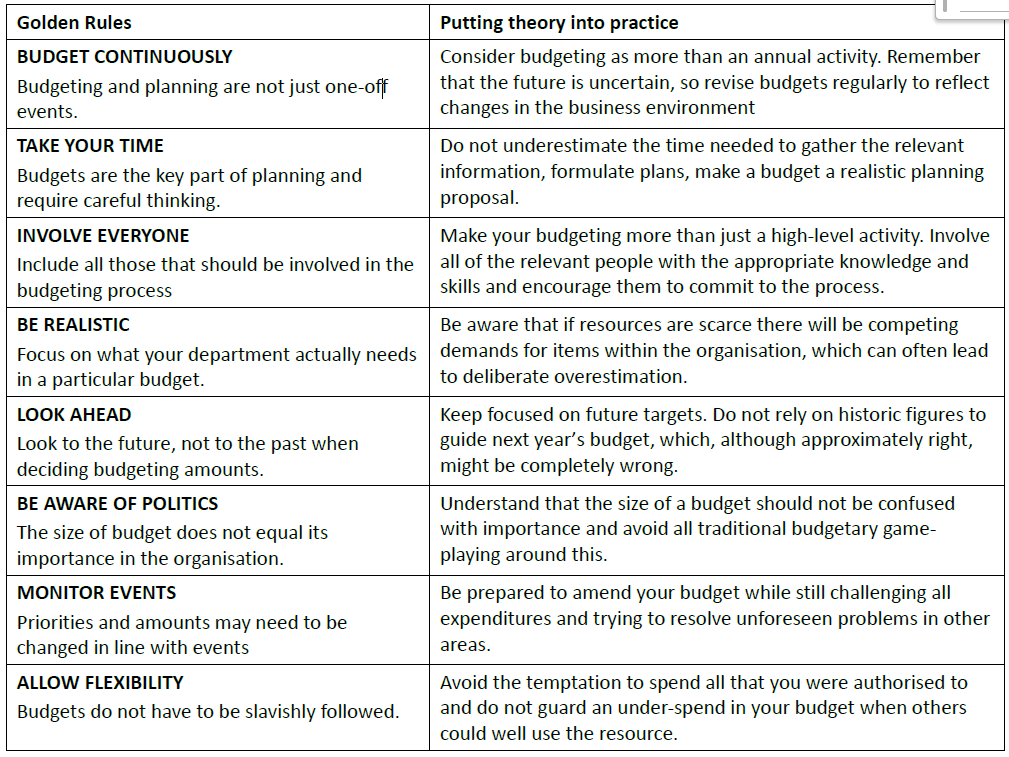

Budgets should be flexible and tailored to suit the departmental circumstances. You should double check that your budget is well-matched to others and that there is a degree of consistency throughout the organisation. This can be done by making sure that everyone involved in the process keeps to the same principles of budget preparation. Keep following a list of rules (8 golden rules for effective budgets) for the whole budgeting process to make sure the budget is consistent and realises its full potential.

Identify the elements of the budget for the resources required

It is important that you understand costs fully so that you can turn out a clear-cut budget that contains accurate forecasts and provides a better basis for analysis and decisions. A cost can be defined as the amount of money which has been spent or will be spent in the normal course of business in bringing a product or a service to the customer.

You should understand what drives costs to be clear on cause-and-effect; (have you spent more because you are busier, or just less efficient?) as well as to gain more accurate expenditure estimates and more useful analysis.

Think about this: If an organisation doubles its sales will, all, some or none of its costs also double? Will bought-in Raw Materials double? Probably they will, but will head office costs double? Almost certainly, they will not. Why are certain costs incurred: is it for one, or for many purposes? How should the cost then be allocated between the goods, services, and departments use the cost?

Let’s now have a look at some of the terms use when referring to costs:

Cost Centre: A cost centre can be a location, such as a factory, office, department or an item of equipment e.g. a Scanner or an entity such as a film production unit; or a person such as a rock star, where costs may be collected and related to cost units.

Cost Unit: A cost unit is a quantity produced (e.g. a motor car) or a service undertaken (e.g. a dental treatment) or a time spent (e.g. an hour with your solicitor), in relation to which the costs of the operation may be conveniently collected.

Costs should be looked at from two standpoints; fixed or variable and direct or indirect. Let’s have a look at these costs:

Fixed Costs – Fixed costs are those costs that tend to remain unchanged in total for the short term, even if activity increases. Examples of fixed costs are rend, rates, salaries and some insurance costs.

Let’s say that each person in the department is paid a salary of R5000.00 per month. This amount will not change in the next 12 months. The budget has been set for those twelve months – this would then be considered a Fixed Cost.

Another example of a fixed cost would be: The rent that is paid for the building in which the business is housed. This rent will not increase in the short term, say 12 months and is not set according to the amount of activity that takes place within the building.

Variable Costs – Variable costs are those costs which change directly in relation to changes in activity and volumes. Examples of variable costs are electricity, water and raw materials.

These costs are easier to understand. If we live in a house or a flat we have to pay for our electricity and water and so does a business. The accounts that we receive every month are never for the same amount. Therefore these are variable costs.

Direct Costs – Direct costs are those which can be charged to or allocated to cost centres or cost units specifically concerned with production of goods or services. Examples would be: raw materials, labour, production equipment.

Indirect Costs (also known as shared costs) – All the other costs brought about in supporting the production and sale of the product or service. Examples would be: administration costs, distribution, marketing and sales effort.

Management Costs/Expenses

Various costs can also be found in the Profit and Loss Account and are deducted to determine operating profit. These costs are called Selling, General and Administration Costs or Operating Expenses. They cover any expenses not listed under Cost of Sales. They include: marketing and advertising which are listed under selling expenses. General and administration costs would cover head office and administration costs.

Once you have completed your budget, it will need to be sent to top management. It is important that you are well prepared so that you can put forward the best possible case for your department.

In summary: A direct cost is incurred for the benefit of just one product or service, whereas an indirect cost is incurred for the benefit of many. It is important to know how to allocate costs back to products and services. For example, you will need to decide how much of the head office cost each item will bear. This will affect each product’s profitability and can be used by senior management to assess its viability.

Applying Zero Based Budgeting

The Zero-based budget is normally used in times of financial crisis or after a company has been taken over or merged with another company. All existing budgets would be suspended and all budget holders would be asked to question and justify any expenditure not directly related to the core activities of the business. The idea is to reduce the expenditure for the master budget so that senior management can establish the minimum requirements to run the business. This system deliberately ignores all history that could contain some false assumptions and starts from fresh.

To prepare a Zero based Budget, you need to follow four steps:

- Describe each activity separately

If you want accuracy in your budget, then you need information about the activities that will take place and the resources needed to support those activities and finally, and most important, the costs. The information on these activities is important for without it you may find you have omitted a cost for a small but really important item.

So, let’s say we have been asked to install a drinking vending machine in the office. We need to draw up a budget – this budget would not be based on historical data.

Our list of activities may look something like this:

– Supply Machine

– Select location

– Provide Electrical power

– Provide potable water

– Provide waste water drainage

– Provide storage facility for consumables

– Provide solid waste facilities (cups etc) - Conduct a Cost-benefit analysis for these activities – then rank them in order of the results

You may have a rough estimate of how much this is going to cost you, say in the region of R5000. Remember, this is a rough estimate, so it could be more or it could be less.

We now have to find out from the suppliers of such machines the actual cost of the machine itself.

We then have to analyse how this will benefit the staff that will be using it.

We must analyse how installing such a machine will benefit the company; say in terms of productivity. For example time may be wasted by staff disappearing from their workstations to walk down to the shop to buy cool drinks.

We must then work out how much cups and other accessories are going to cost the company on an on-going basis.

– How is the machine going to affect our water account, if at all?

– What are the possible maintenance costs involved?

– How much is it going to cost for work such as: drainage system, storage facilities and waste disposal facilities?

Once we have calculated the costs of obtaining and installing the machine, plus the amount of time wasted by staff having to leave the office, we will be able to establish the cost vs. benefit to the company.

It may be that the time spent by staff leaving the office costs the company far more than it will for the machine to be installed.

- Allocate funds appropriately

The funds for the installation of the machine are then allocated to each activity. Remember each activity will have a cost. You may need a plumber and an electrician, as well as a handyman for the installation work. You need to know how much time and money is to be spent on each. You also may have to provide equipment for these people to do their work. - Monitor and Evaluate

It is important that you monitor each step taken in the installation of the machine. There may be discrepancies between what you budgeted for and the actual performance results.

Although this is a very small project used as an example, it points out the important steps in Zero-based Budgeting.

PREPARING A BUDGET BREAKDOWN

There are various ways of compiling a Budget Breakdown. One way of completing this exercise is to use a spreadsheet format to list items that are to be included in the Budget. This is known as a Budget Form.

A budget form is the standardised actual layout that is used to collect and display all the information that goes into the budget. While most companies should insist on standard forms, some do allow a degree of flexibility appropriate to the specific individual circumstances. Keep the following five principles in mine to make sure that the forms looks good and is easy to read and understand.

Keep the form simple and straightforward, with only the necessary details.

– Avoid amateur and over-enthusiastic artwork.

– All forms should be consistent, with similar layout, typeface and design

– The form should be logically presented, well-organised and be understandable without instructions.

– Wherever possible, use spreadsheets or tables to ensure easy capture of information and ease of subsequent processing.

When filling in the form, ensure you have inserted figures accurately and that they have been added or subtracted correctly. Check that the information is correctly arranged in columns and rows and that decimal points and commas are in the right places. Try to make the form as intelligible as possible. Correct all grammar, spelling, and punctuation and avoid using any jargon, slang, technical or vague language. Keep the words and phrases short.

Once you have completed the form, give it to someone else, such as a Manager to check that they can understand what you have written.

Remember that time spent on a well created form is never wasted. Not only will it portray a well-presented and professional image, it can be understood easily by others and importantly, can be easily referred to during later budget discussions.

A Departmental Budget will only require the expected expenses and revenue of that Department. This budget will then be consolidated into the Master Budget.

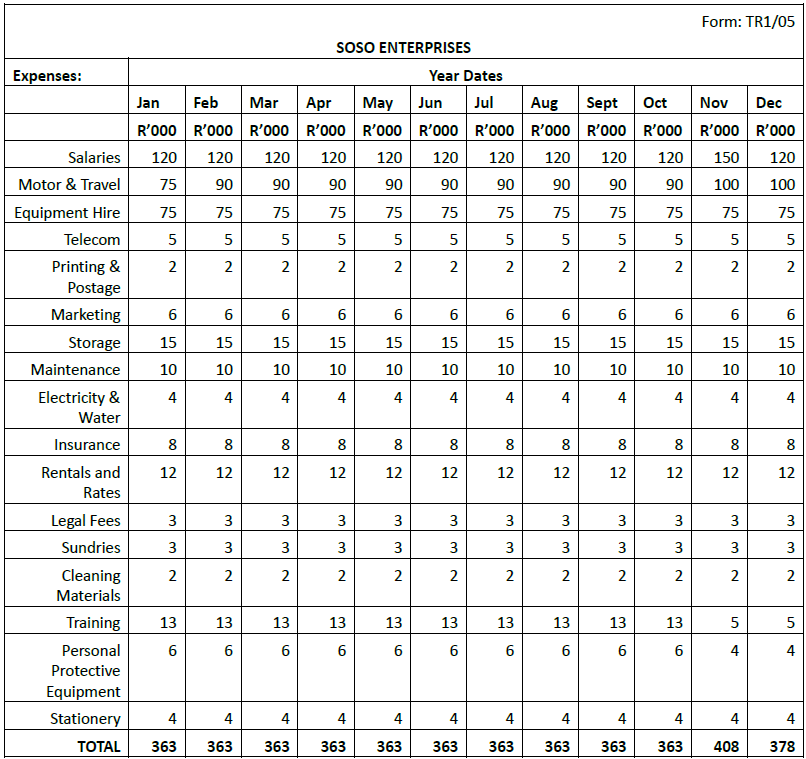

Let’s now look at an example of a Budget Form – Next page

In this example you will notice that the figures every month for each line remain unchanged until November and December. This assumes that during these two months, bonuses will be paid, for example, to the staff. Training costs will come down due to people going on holiday during this period, but travelling expenses will increase due to extra travel required to customers – to complete their requirements for the year.

The amounts shown for each commodity or expense is the maximum amount allocated to the Department for expenditure. Careful monitoring of spending within the department should be done to make sure that the department stays within the budget.

Substantiating Estimated Amounts

Actual expenditure is usually greater than that budgeted for. Businesses need, therefore to ensure an accurate forecast is made. They need to focus on the types of expenditure, the amounts and the timing – in other words when the expenditure will take place.

Expenditure must be estimated in terms of both quantities used and prices paid. There is no doubt that a list of possible activities and costs may appear to be endless. Ask every relevant department and colleague about the probable quantities needed, prices payable, and total amounts for all the different possible costs. Remember to allow for the impact of inflation on these estimated costs. Although all the estimates will largely be based on past budgets, your imagination will play a significant part.

Remember to check the previous year’s expenditure to prevent omitting costs from this year’s budget. It is also important to remind yourself that not everything in a budget has to be spent.

Identify internal and external constraints on a budget

In order to write a budget you must gather information, estimate figures for expenditure and income and bring everything together in one agreed overall document.

By gathering information on all the possible internal and external influences on your budget, you will be able to determine what can and what cannot be achieved and what limiting factors may constrain your department/organisation’s activities.

It is important that you are aware of the changing business laws and requirements.

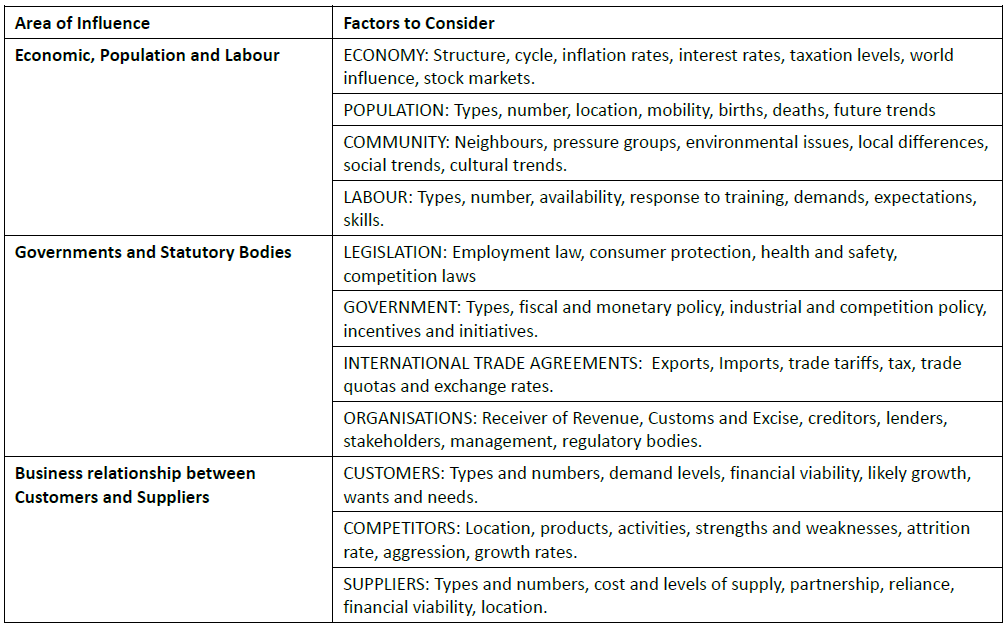

External influences can have a greater effect on the success of a business than internal influences, so pay them close attention. Many companies fail because they simply do not take the time to understand what is happening and what is about to happen around them. The main external influences that can affect your budget can be grouped into three areas: economic, population and labour matters; governments and statutory bodies; and the business relationship between customers and suppliers.

Possible external influences on a budget:

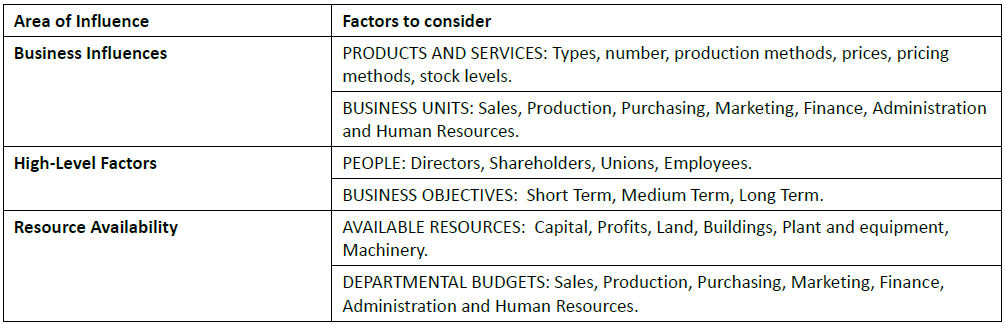

Assessing the influence that internal factors will have on a budget may seem simple enough but, because the focus is now looking inwards, sometimes obvious matters can be overlooked. There are three main areas of influence: business influences such as products and services; higher level factors such as directors or shareholders; and resource availability. Since the checklists cannot be too long, always consider what other factors may apply, from the volatility of the business, through restructuring or change initiatives, to quality of management. Remember, internal factors may change and should be assessed continuously. Internal discussions can be the best source of information and significant events should be anticipated.

Possible internal influences on a budget:

There is another influence that has a restricting effect on your department and organisation. This is known as a Limiting Factor. Identify limiting factors early in the budgeting process because they will determine the order in which you prepare individual budgets. If you fail to recognise a limiting factor you may set yourself targets that are just not achievable. There will probably be only one limiting factor; usually it is sales or the capacity to produce, though sometimes the marketplace may be the limit, especially if it is stagnant or not competitive.

Other limiting factors include shortages in raw materials, labour investment and machinery or there may be physical constraints on property and premises.

It is therefore important that you read all the internal business communications available to you so that you are aware of activities.

The budgeting constraints can be summarised as:

Losing sight of your objectives – Sometimes the process of budgeting becomes overwhelming resulting in the focus becoming more on the process of budgeting than the objectives of the budget. It is therefore important that you focus every decision toward the achievement of your objectives.

Failing to keep objectives realistic – Often people overstate income and or expense projections and then become disappointed when the numbers on the budget do not match actual performance. Therefore, it is crucial that you compare all objectives for the upcoming accounting period with actual performances from previous periods. Also, carefully examine all assumptions made about the organisation and the economic environment for the upcoming accounting period.

Using an incorrect approach – Historical-base budgeting is the process of basing your objectives for the upcoming accounting period on the previous period’s actual performance. Some persons automatically use the previous accounting period’s performance as the budgeted amount for the upcoming period, adding an inflationary increase.

The problem with this budgeting approach is that consideration is often not given to whether the previous accounting period’s performance was good or poor. If the financial activities from the previous accounting period were inadequate, using these figures as a guideline for the upcoming accounting period will simply prolong poor performance.

Accepting arbitrary changes – Objectives are set for a reason: to guide the financial activities for an upcoming accounting period. Therefore, any deviations from the plan for achieving a budget objective should be investigated and, if found to be inappropriate, stopped.

Believing that sales have to increase – It is often believed that sales have to increase with each new accounting period. In fact, some individuals think that if sales do not significantly increase each accounting period, the company’s efforts have been a failure. However, this is not always true.

Inflexible budgets – Another difficulty with budgets is that they are often inflexible. Sometimes situations change beyond the control of those responsible for the budget. For example, an operating budget based on annual sales of R10,000,000 may be completely unrealistic if sales are reforecast to R15,000,000 by the time half the accounting period has passed. Since the cost of operations generally increases when more items are produced to meet increased demand, it would be unreasonable to expect those responsible for the operating budgets to keep to the original budget.

To overcome this potential problem, organisations use variable budgeting. Variable budgets show how each item should vary as the level of activity or output varies.

JUSTIFYING THE BUDGETED AMOUNTS

Before departmental budgets are brought together you must review your own budget and ensure the following steps were taken:

– Limiting factors were correctly identified

– Relevant background information was gathered

– Both external and internal influences were recognised and considered

– Other material sources of information and advice were taken into account

– Types, amounts, and timing of income, expenditure and significant one-off items were conservatively predicted.

Only when you are satisfied that you have extensively reviewed your budget, tested the figures and made any necessary amendments should you submit it to the budgeting committee.

Once your budget has been confirmed, the budget committee will be ready to finalise the master budget. Be well prepared for dealing with the committee so that you are in a position to put forward the best possible case for your department or team.

The budgeting committee should comprise senior managers from the major business segments, the management accountant and the heads of all departments involved in the budget preparations. The committee is set up to review departmental budgets by studying budget forecasts at meetings, create a master budget, be a general budgeting trouble-shooter and ensure that the whole process is completed effectively and on time.

The budget committee’s role is to review the figures and assess their viability. You must be prepared to answer questions. For example: What if the sales rise or fall more than you anticipated? Or How will costs for Human Resources, Purchasing, Production, Marketing, Finance and Administration affect the budget?

You will need to decide which factors could affect your budget, in what ways and whether there are any other circumstances that may be relevant to your department and to the whole organisation.

As your individual department budgets are brought into the negotiation process, they are examined in relation to each other. You may simply not be aware of other plans, conditions and constraints that could affect what your department has budgeted for. Remember that high level executives will be present at any budget meetings, representing the major parts of the organisation as well as the chairperson and accountant. The chairperson advises and liaises with departmental heads and coordinates the final agreements. Accountants are there to help you with your budget preparation rather than to determine the actual content of all the various budgets.

MONITOR AND CONTROL ACTUAL EXPENSES AGAINST BUDGET

After completing this section, the learner will be able to monitor and control actual expenses against budget, by successfully completing the following:

– Actual expenses are monitored according to Standard Operating Procedures

– Variances are identified and corrective measures are proposed and/or taken according to Standard Operating Procedures

To co-ordinate budgets within any organisation, managers should use a standard budgeting format. This will help with teamwork over budget content and enable budgets to be compared and linked throughout the organisation. When an organisation uses a standardised format for their budgeting, past budgets for the department may be used to ensure correct completion.

The preparation of identical reports in the same format from one time to the next helps the reader to identify important facts or information. Standardising the report format also helps the reader to compare the information contained in one report with related information contain in others.

If you are new to the budgeting task, it is always a good idea to pull copies of previous budgets and accounting reports and compare the budgeted numbers to actual numbers. If no historical information is available, find other sources of information that can help guide the development of figures for your budget.

Check over your draft budget and see whether it makes sense to you. Are you missing any anticipated sources of revenue or expenses? Are the numbers realistic? Do they make sense when you compare them to any historical budgets that you have sourced? Most importantly, will you be able to support your figures when you present your budget to senior management?

Monitor actual expenses

You need to use your Standard Operating Procedures to monitor the actual expenses against the budgeted expenses.

To monitor your organisation’s actual performance against the budgeted performance it is necessary that you keep every record and document from every activity every month. The actual performance compared with the budgeted performance will give you both positive and negative variances as we have described. We now need to use the information that we have so that we can project the on-going effects of these variances or how things will change if we take corrective action.

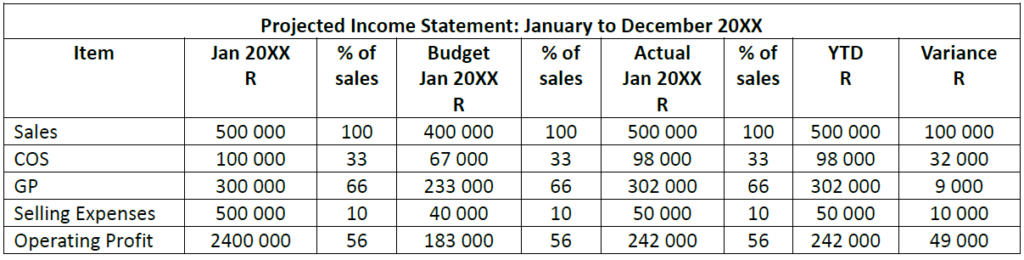

The projected Income Statement is the most useful and the most common method of presenting a projection. This may be a single projection for the business as a whole or it could be split into various areas of responsibility.

Let’s take a look at how this is done:

The preparation requires seven steps; four of which would usually be carried out by the Finance Department. You would then be given a form and a blank template to complete for the balance of the document.

- List all the budget items

- Now enter the Rand value of the historical performance

- Enter the historical value as a percentage of the sales volume

- Enter the new amounts for the new accounting period.

- Create data for the column for the actual performance. This may be per month or quarter: You will need all your information of your department’s financial performance for the period (month/quarter). This will be the results of your activities during that period and is recorded in your financial reports. Record these figures in Rand values and percentages.

- Create data for the Year to Date column: These figures would be the totals for the activities for the Year. These will be compared with the annual budget.

- Calculate the variances and enter them into the Variance Column: Now you need to subtract the actual from the budgeted performance. If you have a positive variance it means that the figure is higher than it should be. This is not necessarily good. If you have a negative variance the figure is lower than it should be which is not necessarily bad.

It could be that you are using a manual system. If so, the negative variance should be shown in brackets, for instance: (R3000.00). Should you be using a computerised version, the software would show the variance either in black with a minus sign in front of it or in red with a minus sign in front of it.

It is important to investigate a variance to find the cause and take the necessary corrective action.

Identify variances and propose/take corrective measures

There will always be discrepancies between your budget and actual performance results. To make constructive adjustments for the future, provide for a framework with which to understand and analyse all such discrepancies.

It is important to understand why there are discrepancies, no matter how small, between your budget and actual performance. What might seem an insignificant discrepancy to you and your department could be crucial to the whole organisation, especially if other departments are also not meeting their budgets. By assessing why discrepancies have occurred, you will be able to ensure that the chances of them happening again are reduced and that future discrepancies are more efficiently anticipated.

Comparing actual performance with budget is the traditional tool used by senior management to measure managerial and business performance. A good business management system asks questions such as “Do I have the correct plans in place?” and “How is each part of the business contributing?” A budget managed properly and taken seriously becomes a more forward-looking document that can assist senior management to identify trends, predict year end results and avoid any unpleasant financial surprises.

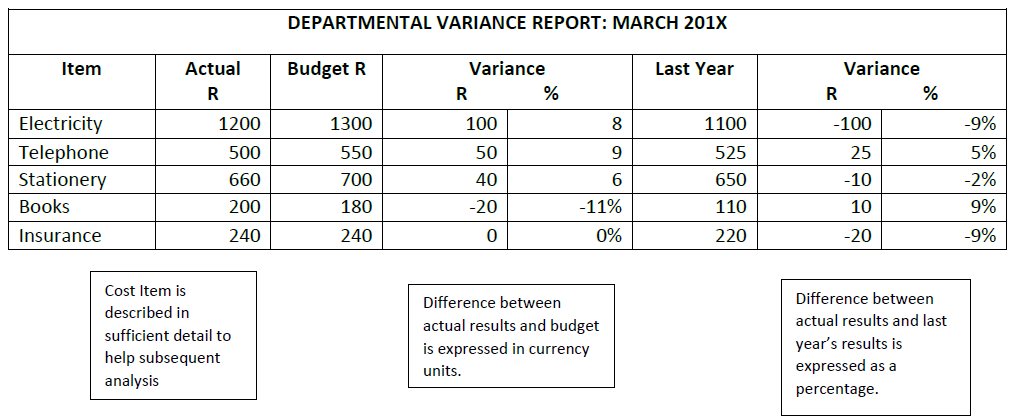

The report has a heading showing the month of the year of the variance report.

You will see from the example that the actual results are compared to the budget and expressed as a variance. The results from the current year are then compared to the previous year and the variance is shown as a percentage.

It is important to continually monitor the discrepancies and understand how they have arisen. Variances are generally categorised as either budget errors or unexpected variances. Constant monitoring helps to promote a greater overall understanding of cost behaviour, which will help you produce a more accurate budget next time around. However, to do this well you must establish suitable monitoring procedures. Experience shows that to be truly effective, your procedure must be regular, easy to administer and sufficiently detailed.

Let’s look at how this is done:

Identify significant variances so that you can make sure that your budget is adhered to as closely as possible. To select which variances to look at further, consider the likelihood of the variance being controllable, the probable cost of investigating the variance and the chance that it might arise again in the future.

Once you have identified the variances there may be a lot that you can do about them. A controllable cost is one that can be influenced by the budget holder. If a cost is controllable then senior management will expect you to exercise your influence and adjust your expenditure where appropriate. Consider the situation where the cost price of a raw material has increased significantly during the budget period. Although you cannot change the price of the raw material, perhaps you could use a cheaper alternative. If skilled labour shortages drive up rates, consider using other grades or even lowering the skills needed for the job to avoid this constraint. Using alternative is not the only type of control you can exercise. You could for example, consider reducing your discretionary costs by choosing not to spend money on advertising, staff parties and bonuses.

Providing Feedback

When presenting feedback on the budget of your department, it is important to follow these guidelines:

– Make certain that you understand the business budgeting process.

– Read through the guidelines that you need to follow and make sure you understand them

– In your report make sure you show how the budget is used in the company in terms of timing and duration of the budget.

– Communication is important: while compiling the report it is essential that you keep in close contact with the financial person within your department or the Finance Department. Remember to ask questions about anything that you do not understand. Ask advice about any assumptions you may be making.

– To report back successfully you need to make sure that you know the real concerns driving the people making the decisions about the budget and address them.

– It is also important that you substantiate budget items in terms of the cost to benefit returns.

– Buy in from the decision makers in the company is vital. Spend as much time as you find necessary to inform these people about your department. This will form the ground work for making any changes at a later stage.

– Know the lines in the budget that you are working on. If you are unsure then make certain you find out. It is important that you what something means and where any particular number comes from.

– Involve your team. Consult with them continuously throughout the budget process. Remember, the more you plan the better you will be able to respond to questions and unplanned variances.

– Whenever possible compare actual to budget amounts. If there is a major or unexpected variance, it is important you find out why. Notify the finance person as soon as possible.

Proposing Control Systems

After the budget has been prepared and approved, budgetary control becomes important. While the preparation process takes place one during the financial year, budgetary control is a continual process.

The budget report is used frequently as a mechanism to coordinate, assess and control various operations. The detail needed in the budget report of the office function for instance will be determined by the report’s intended use.

Because department reports are frequently consolidated to make a larger budget report, less detail will perhaps be needed than if such a consolidation does not take place.

A fundamental purpose of budgeting is the enhancement of the organisation’s profitability. In many instances, the organisation’s profit is improved because of the use of skilfully written, carefully prepared budget reports.

Budget errors happen as a result of poor preparation of the original budget. Sales will be lower than expected while costs will be out of control. It is vital that you understand where you went wrong so that you do not make the same mistakes again.

Actual budget errors may be due to insufficient research into budgeted amounts, lack of understanding of what drives the business financially or insufficient questioning of the figures. The obvious solution to low income and high costs would be for you to reverse the situation and increase sales and reduce costs.

You need to analyse why things went wrong and ask the following questions:

– What are the commonest variances encountered when monitoring costs, their cause and effects and possible remedies?

– In particular, what are the main variances in sales revenue, likely causes and effects and possible remedy?

– It can help to understand where errors have crept in by categorising revenue and expenditure variances into price, volume and timing.

Once these questions have been answered you are ready to report on the Budget, its variances and the measures that can be taken to control them.

A meaningful way of looking at unexpected variances is by considering the variance as a planning variance or as an operational one. A typical budget contains information that was thought to be correct at the time of the preparation. A post budget is written after the period to which it relates. It is used to produce, with hindsight achievable budget. A planning variance is a variance generated by the original budget that is changed to a post budget. An example of this may be the variance that happens when an original budget does not take into account a significant increase in raw material prices due to a world shortage. The post budget builds in this factor for the original time period. An operation variance is where a post budget is compared with actual performance in the current time period. It shows how the department might be currently performing in line with hindsight which is all that might be reasonably expected.