MODULE 2 – PART 1: Explain the free market system in terms of perfect and imperfect competitive markets.

INTRODUCTION

Every society must answer difficult economic questions, such as “How should people use resources?”, “What goods should people produce, and in what quantities?”, “Who should get the goods that are produced?”, and “How much should they pay for these goods?” How a society answers these questions depends on its economic system. An economic system is a way of producing and distributing goods and services. This section will provide you with basic knowledge of the free market system.

DEFINITION OF KEY TERMS

Economic system: an economic system is loosely defined as country’s plan for its services, goods produced, and the exact way in which its economic plan is carried out

Free market: is a market economy based on supply and demand with little or no government control.

Business venture: is a start-up entity developed with the intent of profiting financially. A business venture may also be considered a small business. Many ventures will be invested in by one or more individuals or groups with the expectation of the business bringing in a financial gain for all backers. Most business ventures are created based on demand of the market or a lack of supply in the market. Needs of consumers are identified for a product or a service and the entrepreneur and investors will proceed to develop the idea, market the idea, and sell the product or service developed.

CHARACTERISTICS OF DIFFERENT ECONOMIC SYSTEMS

There are four major economic systems in the world today:

▪

Capitalism/ market economy

▪

Socialism

▪

Command economy, and

▪

Mixed economy.

CHARACTERISTICS OF MARKET ECONOMIES (CAPITALISM)

▪

Individuals and businesses own most of the natural and capital resources. These are the factories, farms, machinery, land, minerals, and other resources used to produce goods.

▪

Individuals and businesses also buy and sell goods freely.

▪

Economic decisions are made by individuals competing to earn profits

▪

Individual freedom is considered very important

▪

Economic decisions are made by the basic principles of supply and demand

▪

Profit is the motive for increasing work rather than allowances

▪

Also called capitalist economies

▪

There are many economic freedoms

▪

There is competition among businesses

▪

Competition determines price which increase the quality of the product

▪

Capitalism is the economic system in the United States.

CHARACTERISTICS OF A SOCIALISM ECONOMY

▪

The people, through their government, own many of the resources and manage the economy.

▪

Representatives of the people decide what to produce and how much.

▪

The government then plans how to carry out these decisions.

▪

The government also distributes most goods and services, especially with regard to housing, food, medicine, and other basic necessities.

▪

Many nations today engage in limited socialist programs, such as socialized medical or education systems.

▪

However, only a few nations can be said to operate entirely under socialist principals.

CHARACTERISTICS OF A COMMAND ECONOMY

▪

The government owns nearly everything that is used to produce goods.

▪

Government planners, rather than the people, make the decisions about what to produce and how to distribute it.

▪

Change can occur relatively easily

▪

There is little individual freedom

▪

There is no competition

▪

Businesses are not run to create a profit

▪

Consumers have few chooses in the market place

▪

Factories are concerned with allowances

▪

Shortages are common because of poorly run factories and farms

▪

The government dictates the job in which you work

▪

The government sets the prices of goods and services

▪

Examples of Command economies: Cuba and North Korea

CHARACTERISTICS OF A MIXED ECONOMY

▪

In a mixed economy, individuals, businesses, and the government own some parts of the economy.

▪

All of these groups play a role in making economic decisions about what to produce and how to distribute it.

▪

Government guides and regulates production of goods and services offered

▪

Individuals own means of production

▪

Protects consumers and workers from unfair policies

▪

Most effective economy for providing goods and services

▪

Russia is an example of a mixed economy

Another type of economic systems includes the traditional system.

CHARACTERISTICS OF TRADITIONAL ECONOMIES

▪

Are found in rural, non-developed countries

▪

Some parts of Asia, Africa, South America and the Middle East have traditional economies

▪

Customs govern the economic decisions that are made

▪

Technology is not used in traditional economies

▪

Farming, hunting and gathering are done the same way as the generation before

▪

Economic activities are usually centred toward the family or ethnic unit Men and women are given different economic roles and tasks

ROLE OF A COMPETITION IN A FREE MARKET SYSTEM

A free market economy allows competition. Competition results in goods and services being provided to consumers at competitive prices. Without competition, prices would be a lot higher. This is due to the fact that companies compete for more customers. A way to gain more customers is lower prices. This is the advantage over having a free market economy rather than a command economy. In a command economy, there is no one to compete against so you can charge as much as you want for your products. In a free market economy, you can only survive if you lower your prices. This is because consumers have a

choice of what company to buy from.

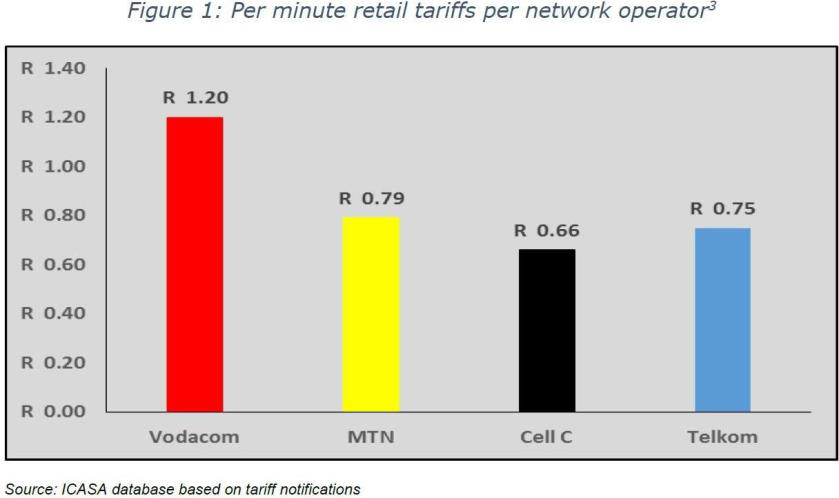

Let’s assume a consumer want to buy a new mobile phone from one of South Africa’s major telephone service providers. The consumer can compare different prices each telephone service provider charges per minute as illustrated.

▪

Who would you choose to use as a service provider?

▪

Is it about price only?

A second benefit of competition is its effect on efficiency and productivity. Companies that are faced with vigorous competition are continually pressed to become more efficient and more productive. They know that their competitors are constantly seeking ways to reduce costs, in order to increase profits or gain a competitive advantage. With that constant pressure, firms know that if they do not keep pace in making efficiency and productivity improvements, they may well see their market position shrink, if not evaporate completely. It is exactly this process of fierce competition between rivals that leads firms to strive to offer higher quality goods, better services and lower prices.

A third benefit of competition is its positive effects on innovation. In today’s technology-driven world, innovation is crucial to success. Innovation leads to new products and new production technologies. It allows new firms to enter into markets dominated by incumbents, and is critical for incumbent firms who want to continue their previous market successes and stimulate consumer demand for new products. Competition drives innovation. Without competition, there would be little pressure to introduce new products or new production methods. Without this pressure, an economy will lag behind others as a centre of innovation and will lose international competitiveness.

A fourth benefit of competition is that it fosters restructuring in sectors that have lost competitiveness. It is difficult for governments to determine which sectors of the economy need to be restructured, which firms in those sectors should remain or should cease to exist, and when it is best to engage in such restructuring.

Governments are subject to political constraints and pressures, which more often than not lead to sub- optimal decisions. The competitive process, on the other hand, is unbiased. It forces decisions to be based on market factors, such as demand, product uses, costs, technologies, rather than the incomplete information in the possession of government bureaucrats.

The competition for capital and other resources by firms throughout the economy leads to money and resources flowing away from weak, uncompetitive sectors and firms and towards the strongest, most competitive sectors, and to the strongest and most competitive firms within those sectors. In these ways, the very operation of the competitive process makes decisions on restructuring clear, and leads to the strongest and most competitive economy possible.

The biggest and the most successful business organisations in the world today are the ones that face the most competition in their respective industries domestically. These organisations are still growing strong because they provide quality goods and services to consumers at competitive prices. Such organisations include; Eskom, Colgate, Nokia, Adidas, LG, TATA, Dell, Hyundai, Telkom, Microsoft, Hyundai, Lays and Bata.

In addition, nations and states that practice economies that comes closest to being “Perfect Competitions” have, not just the most satisfied and prosperous consumers, but also the best overall gross outputs and growth rates.

REASONS FOR IMPERFECT COMPETITIVENESS

Imperfect competition is the real world’s competition that is less effective in lowering price levels nearer to the cost levels than the theoretical perfect competition. Conditions that help cause imperfect competition include:

I.

restricted flow of information on costs and prices

II.

near monopoly power of some suppliers

III.

collusion among sellers to keep prices high, and

IV.

discrimination by sellers among buyers on the basis of their buying power.

Competition comes in two basic varieties, both of which are found in imperfect competition-competition among the few and competition among the many.

Competition among the few: This form of competition occurs with only a handful of participants. Each participant usually knows the other competitors quite well. Many markets operate with competition among the few. In such markets, one seller can gain a competitive advantage by offering a product that is just a little better than other sellers-not the best product, only a little better product. Such competition seldom leads to an efficient use of resources.

Competition among the many: This form of competition occurs with hundreds, thousands, or even millions of participants. Each participant is lost among the masses. In this case, the only way for a seller to gain a competitive advantage is to produce the best possible product. Competition among the many brings out the best, that is, the most efficient use of resources.

The theoretical extreme of competition among the many is perfect competition. The key characteristics of perfect competition are:

▪

a large number of small firms

▪

identical products sold by all firms

▪

freedom of entry into and exit out of the industry, and perfect knowledge of prices and technology.

These four characteristics are virtually impossible to match in the real world. Some markets come close to one or two, but none match all four completely. As such, in its purest, perfect form, perfect competition does NOT exist in the real world. All real world markets are by definition, imperfect and those facing any degree of competition fall into the category of imperfect competition.

For example, some industries rely on heavy initial capital investment, such as industrial manufacturers and telecom providers for example, Eskom. This makes the prospect of having many competitors practically impossible. In the real world, markets are evaluated by their relative closeness to perfect competition, and efforts are made to approach it.

BUYING AND SELLING IMPERFECTION

The four market structures that are technically included in the category of imperfect competition are monopolistic competition, oligopoly, monopsony competition, and oligopsony. The first two are the most noted participants. The second two are often overlooked, but justifiably included.

1.

Monopolistic Competition: This market structure is characterised by a large number of relatively small competitors, each with a modest degree of market control on the supply side. A key feature of monopolistic competition is product differentiation. The output of each producer is a close but not identical substitute to that of every other firm, which helps satisfy diverse consumer wants and needs.

2.

Oligopoly: This market structure is characterised by a small number of relatively large competitors, each with substantial market control. Oligopoly sellers exhibit interdependent decision making which can lead to intense competition among the few and the motivation to cooperate through mergers and collusion.

3.

Monopsony Competition: This market structure is characterised by a large number of relatively small competitors, each with a modest degree of market control on the demand side. Monopsony competition represents the demand-side counterpart to monopolistic competition on the supply side. A key feature of monopsony competition is also product differentiation as each buyer seeks to purchase a slightly different product.

4.

Oligopsony: This market structure is characterised by a small number of relatively large competitors, each with substantial market control on the buying side. Oligopsony represents the demand-side counterpart to oligopoly on the supply side. Oligopsony buyers exhibit interdependent decision making which can lead to intense competition and the motivation to cooperate.

THE ADVANTAGES AND DISADVANTAGES OF COMPETITION

Below are some advantages and disadvantages of competition

ADVANTAGES OF COMPETITION TO CONSUMERS

▪

Lower prices for consumers

▪

A greater discipline on producers/suppliers to keep their costs down

▪

Improvements in technology- with positive effects on production methods and costs

▪

A greater variety of products giving more choice to consumers

▪

A faster pace of invention and innovation

▪

Improvements to the quality of service for consumers

▪

Better information for consumers allowing people to make more informed choices

▪

Stops monopolies developing and taking advantage of the consumers

DISADVANTAGES OF COMPETITION

▪

There might be too much choice and not enough product differentiation causing confusion for the consumer Consumers often get bombarded with advertising: lots of companies will be trying to differentiate themselves in order to sell their products

ADVANTAGES OF COMPETITION TO THE BUSINESS

▪

Competition forces companies to increase their efficiency and continually seek ways to improve their production process for maximum efficacy.

▪

New business problems and consumer problems are created every day, providing opportunities for companies to innovate new products that solve these problems.

▪

Healthy competition, when free of monopolies, can also attract investments from other countries, thereby increasing a nation’s gross domestic product.

▪

It allows anyone with a specialised skill set to create something better than what the market currently offers and clean up. Many of the large brands with which we are familiar today were started by a small team dedicated to solving a customer pain point.

▪

Competition gives producers an incentive to produce goods that consumers want.

▪

Competition pushes businesses to be efficient: keeping costs down and production high.

DISADVANTAGES OF COMPETITION TO THE BUSINESS

▪

Investment wealth can be disproportionately allocated into what earns the highest profit, leaving less money for services or goods with less demand.

▪

Business may simply satisfy the wants they have created through advertising.

▪

Product differentiation can result in significantly higher overhead costs for production

▪

Due to tough competition, some business may fail because consumers may not buy their products

INTERACTION OF ROLE-PLAYERS IN THE ECONOMIC SYSTEM

Different role players interact in the economic system. Role-players include consumers, producers and the government. The list and the elements below provide a visual presentation of the interaction between role- players in the economic system.

1.

Consumers’ buying behaviour, as determined by their:

▪

Motivation in purchasing.

▪

Buying habits.

▪

Living habits.

▪

Environment (present and future, as revealed by trends, for environment influences consumers’ attitudes toward products and their use of them).

▪

Buying power.

▪

Number (that is, how many).

2.

The Trade’s Behaviour- wholesalers’ and retailers’ behaviour, as influenced by

▪

Their motivations.

▪

Their structure, practices, and attitudes.

▪

Trends in structure and procedures that portend change.

3.

Competitors’ Position and Behaviour, as influenced by:

▪

Industry structure and the firm’s relation thereto.

✓

Size and strength of competitors.

✓

Number of competitors and degree of industry concentration.

✓

Indirect competition that is, from other products.

▪

Relation of supply to demand-oversupply or undersupply.

▪

Product choices offered consumers by the industry- i.e., quality, price, service.

▪

Degree to which competitors compete on price vs.non price bases.

▪

Competitors’ motivations and attitudes-their likely response to the actions of other firms.

▪

Trends technological and social, portending changes in supply and demand.

4.

Governmental Behaviour-Controls over Marketing:

▪

Regulations over products.

▪

Regulations over pricing.

▪

Regulations over competitive practices

Consumer role in the economy

Purchase Goods and Services: The main role of the consumer is to spend money. How much money she spends is primarily based on her income. How she spends it, however, depends on her needs and preferences. For instance, if she has R1 000 to spend, she might buy R750 worth of groceries and R250 worth of clothes. Or she might buy R500 worth of groceries and R500 worth of clothes. Her spending habits impact different sectors of the economy in different ways.

Maximize Utility

Utility is an economic term for a person’s overall well-being and satisfaction. Consumers play a role in the economy by maximising utility, which means allocating their scarce resources, such as limited time or money, most efficiently. Utility maximisation is different for every person. Some purchase high-end cars; others find a bargain in the discount produce bin. When consumers act in a self-interested manner and maximise their utility, the nation as a whole also operates more efficiently. If consumers don’t waste money on buying unnecessary goods, companies will not waste resources producing those goods.

Make Rational Purchasing Decisions

Economic consumer theory hinges on consumers making rational buying decisions. Though that’s not always the case, consumers sometimes make irrational buying decisions out of fear or greed- the role is the always the same: to measure all possible outcomes of their choices and use this knowledge to make an informed decision. Economists use the theory that consumers make rational purchasing decisions to forecast trends in the market. For example, a rise in the price of meat used to make sandwiches means economists will assume consumers will switch to eating something else.

Government role in the economy

The government guides the overall pace of economic activity, attempting to maintain steady growth, high levels of employment, and price stability. By adjusting spending and tax rates or managing the

money supply and controlling the use of credit, it can slow down or speed up the economy’s rate of growth- in the process, affecting the level of prices and employment.

Business role in the economy

Businesses contribute to the society by selling their products to customers, products that people need. They also provide employment opportunities to people, which can become reasonable career paths and choices.

THE CONDITIONS FOR THE EXISTENCE OF PERFECT AND IMPERFECT MARKERS

An imperfect market exists when any one condition necessary for a perfect market is missing.

PERFECT MARKET CONDITIONS

Perfect Competition (PC): no increasing returns, many buyers and sellers, all are price takers, not price makers.

Perfect Information (PI): buyers and sellers know all they need to know about what they are buying and selling to make the right decisions.

Complete Markets (CM): no externalities or public goods, no transactions costs, “thick” markets

IMPERFECT MARKET CONDITIONS

▪

In an imperfect market information is not quickly disclosed to all participants in it

▪

The matching of buyers and sellers isn’t immediate.

▪

An imperfect market that does not adhere rigidly to perfect information flow, and

▪

Provide instantly available buyers and sellers.

Although imperfect markets differ from perfectly competitive markets in the way prices are established, they trigger similar forces and have similar effects.

▪

In imperfect markets businesses are price makers or price setters.

▪

Imperfect markets are classified into 3 main markets:

✓

Monopoly

✓

Monopolistic competition

✓

Oligopoly

MONOPOLY

It exists when there is only one seller of goods or services for which there is no close substitute, e.g. Eskom.

TYPES OF MONOPOLIES

Legal monopoly: It is based on laws preventing other companies from competing (State monopoly).

Local monopoly: A local monopoly will control the market in a particular area or town, e.g. if there is only one petrol station.

Natural monopoly: This arises in industries where economies of scale are so large that a single business can supply the entire market, e.g. electricity.

Horizontal monopoly: This occurs when a parent company takes control over several smaller companies,

e.g. Naspers in the printing business.

Vertical monopoly: This occurs when 1 firm will supply and produce the product, e.g. Eskom.

Coercive monopoly: This occurs as a result of any activity that violates the principles of a market economy.

CHARACTERISTICS OF A MONOPOLY

▪

No competition: one business controls the supply of goods or service.

▪

No substitutes: no substitutes on the market for the consumer to choose from.

▪

Price makers: one business controls the price of the goods or services.

▪

Barriers to entry: e.g. technology or patents, may keep new companies out.

▪

Imperfect information: the consumer doesn’t have all the information, e.g. profit margin.

▪

No homogenous products: they will produce only one product or different varieties.

▪

Large amount of starting capital is needed.

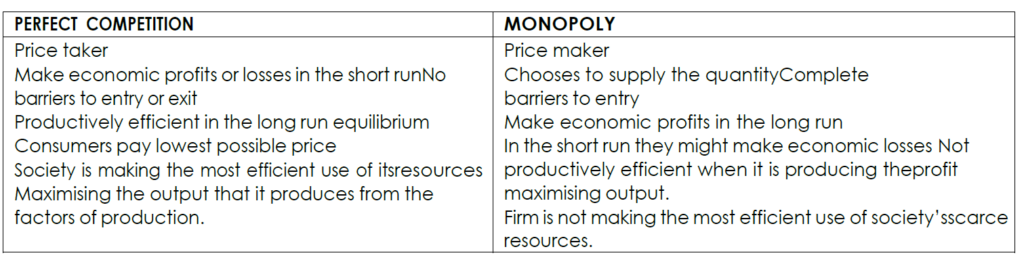

Legal considerations: new inventions are protected by patent rights. COMPARISON WITH PERFECT COMPETITION

OLIGOPOLY

Oligopoly is a market in which a small number of relatively large businesses supply most of or all the output in the market, e.g. oil industry, telecommunication industry, car industry, etc.

CHARACTERISTICS OF AN OLIGOPOLY

▪

Limited competition: Only a few suppliers of the same product dominate the market.

▪

Interactivity: If one company makes a decision, it influence the decisions the other companies make.

▪

Price changes: They will more frequently change their prices in order to increase their market share.

▪

Cost advantage: They have an absolute cost advantage over the rest of the competitors.

▪

Joint decision making: It is a key instrument to make decisions together in order to dominate the market.

▪

Difficult entry; New firms will experience high barriers to enter.

▪

High profits: Abnormal high profits may be result of joint decisions.

INTERDEPENDENCE

▪

Another key characteristic of oligopoly firms is that they are interdependent.

▪

The decisions that an oligopoly firm makes with respect to quantity, marketing strategies and location, for example, depend largely on what it thinks the other firm in the industry will do in response to its actions.

COLLUSION

▪

Explicit collusion is usually illegal between firms within countries.

▪

However, firms are still tempted to practice implicit collusion. In other words, they act together to produce the profit maximizing output but they do it in such a way that it is very difficult to prove that they have colluded.

NON-PRICE COMPETITION

Non-price competition includes the following:

▪

Product differentiation: product is slightly different from the others.

▪

Product proliferation: different range of products to cater for many different markets.

▪

Advertising: oligopoly firms advertise their products heavily.

In South Africa, like many other countries in the world, the perfect market, is not a truly achievable goal, but is still a beneficial model that provides a starting point for observation of our present market status.

Practically, the imperfect market is the only kind that really exists. Even in the United States, the most advanced financial market in the world, there are still numerous cases of price corruption, improperly

disseminated information and other market inefficiencies. Governments in many countries use competition policies to protect consumers and to promote the efficient use of resources.

SUMMARY

SYNOPSIS

In this section you learnt how to explain the free market system in terms of perfect and imperfect competitive markets.

Note what you have learnt in this section in relation to:

▪

Characteristics of different economic systems

▪

The role of competition in a free market system

▪

Illustration of competition

▪

Reasons of imperfect competitiveness

▪

The advantages and disadvantages of competition

▪

Interaction of role-players in the economic system

▪

The conditions for the existence of perfect and imperfect markets.