Part 3 – MANAGE BUSINESS ACCOUNTS AND MAINTAIN BUSINESS RECORDS

INTRODUCTION

Understanding financial statements is essential to the success of a small business. Financial statements can be used

as a roadmap on your business journey to economic success. Using numbers as navigation aids can steer you in the

right direction and help you avoid costly “breakdowns.”

IMPORTANCE OF FINANCIAL STATEMENTS

Many business experts and accountants recommend that you prepare financial statements monthly; quarterly at a

minimum. Some companies prepare them at least once a week, sometimes daily, to stay abreast of results. The

more frequently a company prepares their financial statements, the sooner timely decisions can be made.

There are four types of financial statements; compiled, reviewed, audited, and unaudited:

- A compiled statement contains financial data from a company reported in a financial statement format by a

certified public accountant (CPA); it does not include any analysis of the statement. - The reviewed statement includes an analysis of the statement by a CPA in which unusual items or trends in

the financial statement are explained. - An audited statement (also prepared by a CPA) contains any analysis which includes confirmation with

outside parties, physical inspection and observation, and transactions traced to supporting documents. An

audited statement offers the highest level of accuracy. - An unaudited statement applies to a financial statement prepared by the company which has not been

compiled, reviewed, or audited by an outside CPA

Small business owners must be aware that they may be required to submit financial statements in eight

circumstances:

- Virtually all suppliers of capital, such as banks, finance companies, and venture capitalists, require these reports with each loan request, regardless of previous successful loan history. Banks may need CPA compiled or reviewed statements and, in some cases, audited statements. They may not accept company or individually prepared financial statements, unless they are backed by personal or corporate income. Typically, as a condition of granting a loan, a creditor may request periodic financial statements in order to monitor the success of the business and spot any possible repayment problems.

- Information from financial statements is necessary to prepare State income tax returns.

- Prospective buyers of a business will ask to inspect financial statements and the financial/operational trends

they reveal before they will negotiate a sale price and commit to the purchase. - In the event that claims for losses are submitted to insurance companies, accounting records (particularly

the Balance Sheet) are necessary to substantiate the original value of fixed assets. - If business disputes develop, financial statements may be valuable to prove the nature and extent of any

loss. Should litigation occur, lack of such statements may hamper preparation of the case. - Whenever an audit is required–for example by owners or creditors–four statements must be prepared: a

Balance Sheet (or Statement of Financial Position), Reconcilement of Equity (or Statement of Stockholder’s

Equity for corporations), Income Statement (or Statement of Earnings), and Statement of Cash Flows. - A number of states require corporations to furnish shareholders with annual statements. Certain

corporations, whose stock is closely held, that is, owned by a small number of shareholders, are exempt. - In instances where the sale of stock or other securities must be approved by a state corporation or securities

agency, the agency usually requires financial statements.

INCOME AND EXPENDITURE STATEMENT

An income statement, otherwise known as a profit and loss statement, is a summary of a company’s profit or loss during any one given period of time, such as

a month, three months, or one year. The income statement records all revenues for a business during this given period, as well as the operating expenses for the business.

KEY TERMS IN INCOME AND EXPENDITURE

INCOME

For the purpose of this module, income is defined as money that has been made within the time period of the statement. It is an important accounting concept to correctly account for income within appropriate time period of the financial statement. This means that you should include your income figure in the month where it belongs even if money has not been received.

For example, you are a trader and sold goods to your customers on credit for R1 000 on 20 September In addition, as per the credit terms you agreed that the customer shall pay 6 months later.

Since a sales transaction has taken place in September, the income of R1 000 must be recorded as income in September even if the money will be received in another month.

EXPENDITURE

For the purpose of this module, expenditure is defined as the costs that have been incurred within the time period of the statement. As with the concept of income, you should include expenditure in the period in which it was incurred even if no money was paid. This ensures that you have an accurate statement of income and expenditure of real expenditures incurred within the period.

PROFIT OR LOSS

At the end of the income and expenditure statement, you should subtract expenditure from income, the amount remaining is your profit or loss. If the income items are more than the expenditure items we call that profit but if the expenditures and more than the income, then the difference is known as loss.

PURPOSE OF INCOME AND EXPENDITURE STATEMENT

The following are some of the purposes of an income and expenditure statement:

- To clearly show how much money was made and how much was spent within a given time period

- To know how much profit or loss has been earned within a given financial period

- Helps to pinpoint items that are causing unexpected expenditures

- If you compare income & expenditure statement for different consecutive periods, the enterprise can deduce whether the income is rising or stagnating

Legislation requires that when doing financial statements of a company, certain specific requirements regarding the disclosure of information must be met. According to Companies Act 61 of 1973 a company’s financial statements have to be drawn up in accordance with Generally Accepted Accounting Practice (GAAP).

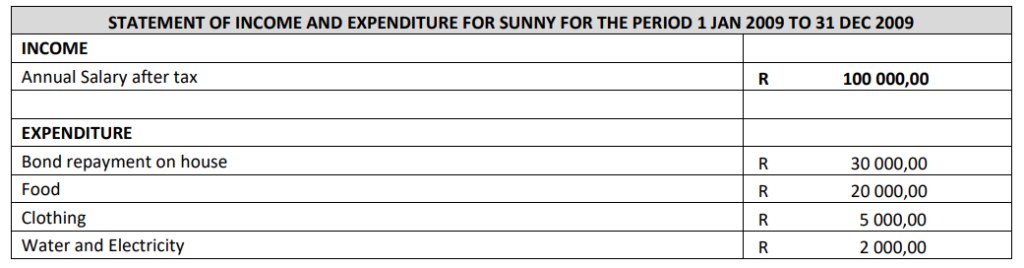

CASE STUDY 1: THE INCOME AND EXPENDITURE STATEMENT OF A PRIVATE INDIVIDUAL

Sunny is a private individual who works in an office as a consultant. She wishes to obtain a loan from FBC Bank to finance the purchase of a new car. Big Sharks has requested that Sunny produce an income and expenditure Statement to demonstrate to them that she has income necessary to meet the repayments of loan which amount to R1000 per month.

Sunny has drawn up the following statement:

From this statement, FBC Bank can easily see that Sunny has sufficient money left over after her expenses have been

deducted to meet the loan repayments of (12 X R 1000= 12 000 per annum)

Normally an individual is only required to produce a statement like this either for, as in the case study, a bank loan or

sometimes when completing a tax return. There is no requirement for an individual to produce the statement on an

annual basis as required for companies by Companies Act 1973.

It is, however, a good personal management tool and wise person would compile such a statement and keep a good

eye on it on a regular basis.

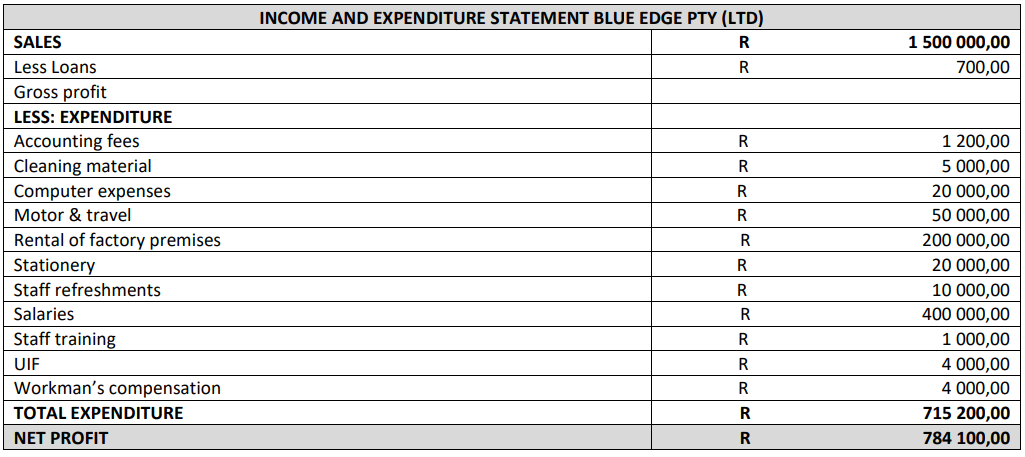

CASE STUDY 2: THE INCOME AND EXPENDITURE STATEMENT OF A COMPANY BLUE EDGE

Blue Edge LTD produces the chemical flavours used to flavour cakes. They have been in operation since 1940 and continue to run as family owned private business. Because they are incorporated as a company, they are required to produce client’s annual financial statements. Interested parties, such as the owners of the company, clients and suppliers who do business, with them and SARS (The receiver of Revenue) may review these financial statements and make decisions on the results accordingly.

The accountant for Blue Edge LTD is responsible for ensuring that the figures contained in the Statement of Income and Expenditure are accurate and reflect a true position of the finances of the company. The Accountant must also produce these financial statements annually after the year end (which in Blue Edge case is the 31 October).

SOURCES OF INCOME AND EXPENDITURE

Income and expenditure sources are as varied as the types of industries and business in operation. People too, derive their income and spend their money in all possible ways. The ways of income are many and varied; it is your task to identify these in the financial statements and be able to differentiate between the income and the costs.

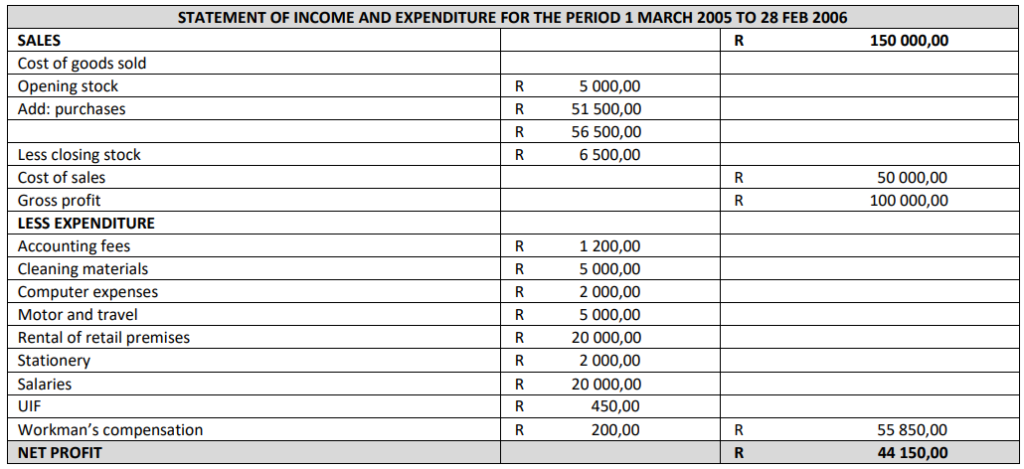

CASE STUDY 3: KEYS COMPANY

Keys Company has a shop in a shopping mall. They sell toys, educational devices, and children’s party tricks. Keys the owner, has had the following statement of income and expenditure prepared for tax purposes.

In case study above, expenditure incurred in generating sales include the purchases of goods for sale, called purchases. Note that purchases in accounting terms has a specific meaning: it means the cost incurred in acquiring goods for resale. It does not include other costs, such as the ones listed in the expenditure section. These must be disclosed separately.

The cost of sales calculation, which is opening stock plus purchases less closing stock, is calculated and subtracted from sales to give Gross profit. Gross profit is an indication of the profitability of operations, not including other expenses and overheads.

CASE STUDY 4 KELLY’S FAST FOOD

Kelly’s Fast foods is a vendor of pies, chicken, cold drinks, fish, chips, coffee and sandwiches. They cater for break fast and lunch time crowd in a nearby office park.

Below is Kelly’s Fast Foods Income statement prepared by the accountant for tax purposes. Now, identity the sources of income and expenditure for Kelly Fast Food.

THE BALANCE SHEET

A Balance Sheet is a ‘snapshot’ of the financial position of the school at a specific point in time, usually the end of an

accounting period. This report lists assets and liabilities as current or non-current, as well as the organisation’s

equity.

PURPOSE OF A BALANCE SHEET

The purpose of a balance sheet is to reflect the financial position of a company or enterprise at a point in time. It is

different from a statement of income & expenditure in that the balance sheet is as at a specific date, whereas the

income statement is for a period of time. Usually, the income statement will cover, say, a financial year, and the

corresponding balance will reflect the financial position on the last day of the year under review.

REQUIREMENTS FOR PREPARING BALANCE SHEETS

- As part of Annual Financial Statements, companies are required to produce Balance Sheets every year.

- Individuals need not prepare balance sheet unless requested to do so by a bank or Receiver of Revenue.

ELEMENTS OF BALANCE SHEET

A balance sheet is separated into two distinct parts:

I. Capital employed section

II. Employment of capital

Based on the basic accounting equation;

TOTAL ASSETS = TOTAL LIABILITIES + OWNERS EQUITY

The two sections of the balance sheet reflect the calculation of the equation:

CAPITAL EMPLOYED SECTION

This section reflects the money the owner has put into the business. This side consists of the share capital of the business (if it is a company: certain forms of trading operations such as sole traders or partnerships, do not have share capital, but reflect the investment of the traders/partners)

SHARE CAPITAL

This is the equity of the business. Usually, a company is incorporated with an authorised share capital that is divided amongst the owners of the business. These shares, as in publicly traded companies on the stock exchange, are tradable in certain circumstances and can be bought and sold. They reflect the division of ownership and profit

sharing. If you own shares in a company, you are entitled to a share of profits in relation to the amount of shares that you

hold. Often, companies pay these profits to shareholders in the form of dividends. But, a company is not legally

forced to pay dividends.

EMPLOYMENT OF CAPITAL SECTION

The term “employment of capital” means what has been done with the money that the owners of the business have invested in the operations. This is the calculation of net Asset less Liabilities. A primary feature of a balance sheet, as indicated in the name of the statement, is that it MUST balance. If a balance sheet does not balance, it is not a balance sheet.

NOTES TO THE BALANCE SHEET

In terms of disclosure as required in the Companies Act 61 of 1973, there are many items that are disclosed in company’s Annual Financial Statements. Often, how the figures that appear on the balance sheet are arrived at are shown in Notes to the Balance sheet. An example of common note would be the calculation of depreciation for Fixed Assets.

THE ANALYSIS OF A BALANCE SHEET

Balance sheets are invaluable tools for analysis of companies’ net worth. By understanding and interpreting the clues within the balance sheet, the analyst can evaluate the value of the company, and make decisions accordingly.

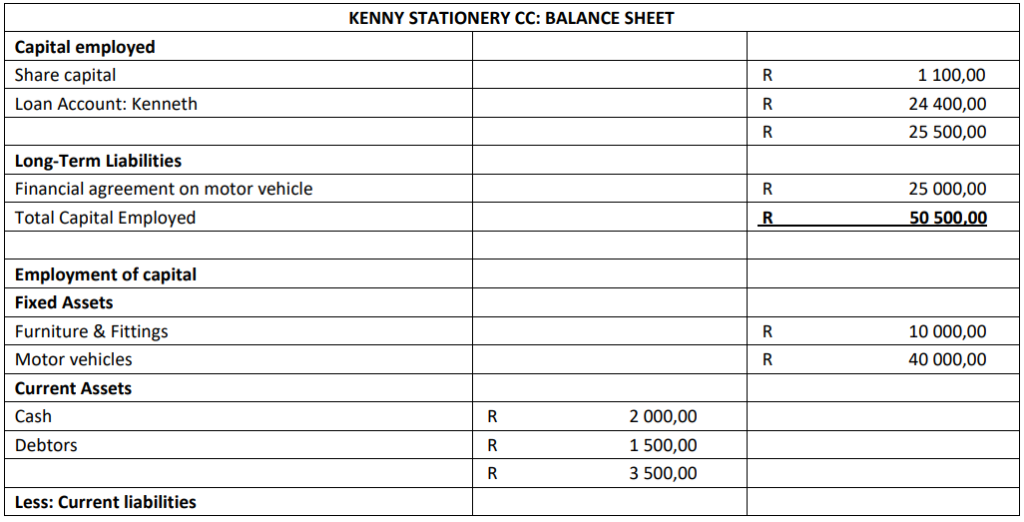

Case study Kenny’s Stationery Shop

The company is incorporated as a close corporation and has been trading for 8 years. The accountant has compiled

the annual financial statements, which contains the following balance sheet.

QUESTION: HOW MUCH IS THE COMPANY WORTH??

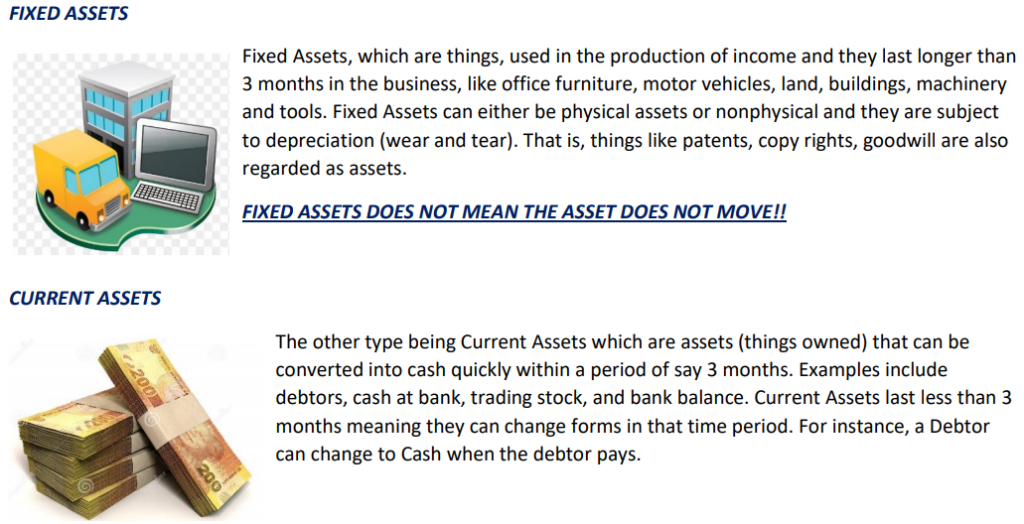

CONCEPT OF AN ASSET

Assets are things that the business owns. The types include:

REMEMBER CURRENT ASSETS ARE NOT SUBJECT TO DEPRECIATION

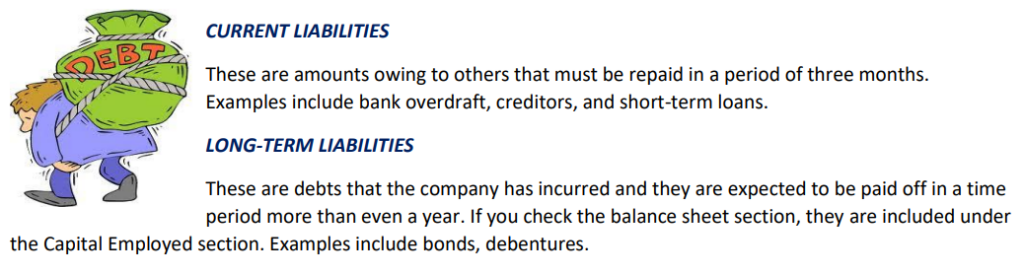

THE CONCEPT OF LIABILITY

Liabilities are amounts that the company owes to other people or companies. These take two forms:

CASH FLOW STATEMENTS

Cash flow is difficult for small business and business planning, thus you should have cash flow statements. Treated with such reverence and explained in such elaborate

terms it’s no wonder we’re all a little bit confused. Cash flow is different to profit and loss (as profit and loss is recorded in the balance sheet and cash flow is recorded on the cash flow statement). Cash flow is quite

simply a measure of cash coming into your business and cash going out of your business. It is given an elevated status because if your business runs out of cash, you

will go bust. So it well worth your efforts monitoring it carefully.

REASONS WHY CASH FLOW IS DIFFERENT FROM PROFIT AND LOSS/INCOME AND EXPENDITURE

Just because you receive an invoice, cash doesn’t necessary leave the same day. In most circumstances, you will charge an invoice to your profit & loss statement according to the date on the invoice. However, you may not pay that invoice until, say, 30 days later which is the point at which you will charge that transaction to your cash flow statement. Similarly, when you issue an invoice, unfortunately not everyone pays the same day.

VAT is paid every three months. When you pay, cash leaves the business and hence an entry appears on your cash flow statement. But VAT doesn’t appear on your profit and loss account at all because it isn’t a cost to your business. You just collect it up and pay it to the tax man.

If you sell off one of the company vehicles, for instance, real cash comes into your business, hence onto your cash flow statement. But the sale would be recorded as the sale of a capital item, not part of your operating profit, hence the transaction would feature on your balance sheet, not your profit & loss statement. The same argument applies if you receive a cash injection from an investor or a loan from the bank.

BASIC ELEMENTS OF A CASHFLOW STATEMENT

The basic elements of cash flow are:

Starting cash — This is your starting balance what you have on hand at the beginning of each month.

Cash in — This is all cash received during the month, including sales, paid receivables, interest or cash from sales of assets or stock.

Cash out — Includes all fixed and variable expenses.

Ending cash — This is your ending balance. Add starting cash to cash in for total cash, and then subtract cash out.

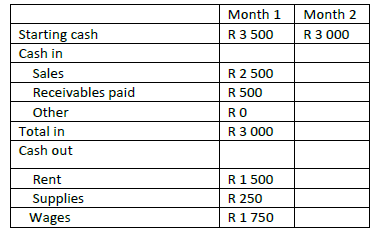

Here is an example of how you measure cash flow by subtracting your monthly ending balance from your starting balance.

Let’s say you started the month with R3, 500. You brought in R2 500 in sales and R500 in paid receivables. You paid out R1 500 in rent, R250 in supplies, and R1 750 for wages This equals a total of R 3 500 in expenses. Your ending balance is R3 000.

While you did show some sales, your monthly cash flow would be -R500. To survive, you want positive cash flow, which means taking in more than you are spending. Positive cash flow gives you forward motion to build and grow.

Even a small lag in sales or an outstanding bill can make a dramatic impact on cash flow, but you won’t know that without your cash flow budget. At the end of every month, compare actual business sales with estimated cash flow and hold them up against your master budget.

If they are out of sync, consider the cause. Maybe you didn’t factor in the need to hire summer vacation replacement help or the jump in paper prices for your printing business. Cut back on cash out where you can, and adjust monthly cash flow projections to more realistically meet your needs.

CASH FLOW MANAGEMENT

Good cash flow management means you can anticipate when your cash flow needs will occur. Your cash flow budget will help you predict what’s coming, but you have to be diligent in daily record keeping and reporting of cash in and cash out.

The following steps can help you monitor cash flow:

- Use renumbered cash receipts and account for all receipts

- Deposit checks daily

- Send customer invoices within two days

- Collect receivables within 60 days

- Take advantage of cash discounts

- Use renumbered checks for all disbursements