MANAGE BUSINESS ACCOUNTS AND MAINTAIN BUSINESS RECORDS

INTRODUCTION

Running a successful business entails keeping accurate and timely financial information. A clear financial picture allows you to monitor the success or failure of your business. A good record keeping system also provides you with the information you need to evaluate the financial consequences of your financial decisions.

As a small business owner, you probably rely on an outside accountant to do your taxes and prepare financial statements. However, it is best that you or someone in your organization take on the responsibility of keeping an accurate set of financial records. Doing the routing bookkeeping chores yourself, however unpleasant it may seem, will minimize your costs of paying an accountant and allow you more control of your financial information and operations.

DEFINITIONS OF KEY TERMS

RECORDS KEEPING

Record keeping is a process of managing the creation, amendment, distribution, filing, retention, storage and disposal of records, which is administratively and legally sound.

RECORDS MANAGEMENT

Records management involves the storage, retrieval and use of information. In records management, the guiding principle is that information must be readily available at the prerequisite time and in the form it is required. In order to effectively utilise the information in the system, the data must be accurate, reliable and informative.

RECORDS

A record is any document, book, paper, photograph, map, sound recording or other material, regardless of physical form or characteristics, made or received pursuant to law or in connection with the transaction of official business.

FINANCIAL RECORDING SYSTEM

For starters, make sure that you file paid bills, cancelled cheques and other business documents in an orderly fashion and keep them in a safe place. You may use manila folders, filing boxes, or an accordion file divided into “car,” “utilities,” “entertainment” and so on. At a minimum, put receipts in the proper categories throughout the year so it would be easier to total them up at tax time. Staple the adding machine tape to each folder or stack of receipts. You are not required to keep records in a formal “set of books;” however, you need to find the best record keeping system that works for you.

Take record keeping seriously. A perfectly adequate record keeping system for a small business might include some or all of the following:

Cheque register – preferably a separate bank account for your business. Make sure that when you receive your bank statement every month that you prepare bank reconciliation. This document will help you balance your cheque book.

Summary of receipts of gross income – totalled daily, weekly or monthly. Keep track of where your money comes from, putting notes explaining the origin of all money received. Your record of revenues received should, at the least, record similar information:

- The type and amount of payment

- Date of the transaction

- The party who paid the money

- The work performed or good provided

- Monthly summary listings of expenses

Disbursements record showing payments of bills. This could be a purchase journal or an expense journal where you record all the transactions in which you paid out cash or cheques. In addition to such records, you should keep a journal or “record of expenses” recording, at the least, the following information:

- How the expense was paid (credit card, cash, check number)

- Date of the transaction

- The party to whom the money was paid.

- The particular type of expense involved (e.g., office supplies, equipment, utilities, rent, etc.)

Asset purchase listing (equipment, vehicles, real estate used in business)All equipment (e.g., computers, fax machine, copiers, etc.) and other assets which have a life span of more than a year must be recorded and the cost amortized (i.e., deducted) over the life span of the asset. Thus, you need to keep records concerning your business’s asset. You must keep asset records providing the following information:

- Description of the asset

- Date of acquisition

- What month you started using the asset (usually the same as purchase)

- Total amount paid for the item, including taxes, delivery charges and fees

- Sales price of any asset sold

- Date of sale of any asset

- Cost of selling the asset (advertisement, broker’s fees, etc.)

- Whether you use the assets for personal use and, if so, how much time the asset is employed for such uses

- Employee compensation record (if you have employees)

ACCOUNTS RECEIVABLE

If your products or services are paid for at time of delivery, you will not need an accounts receivable tracking system. However, if you provide services or products for which people pay you at a later date, your accounts receivable records keep track of what is owed to you. You can monitor accounts receivable by holding on to a copy of all invoices sent out or by keeping an accounts receivable record. Either way, the information you need to capture includes: invoice date, invoice number, invoice amount, terms, date paid, amount paid, and the name of the entity being billed.

ACCOUNTS PAYABLE

Accounts payable are debts owed by your company for goods and services. Keeping track of what you owe and when it is due will enable you to establish good credit and hold onto your money as long as possible. Business owners with few accounts payable items use accordion file folders labelled with dates to keep track. Other small firms simply pay bills twice per month and keep all bills in a “To Pay” folder. Larger companies use accounts payable paper records organized by creditor. Regardless of the system you choose, you should retain the following information about accounts payable: invoice date, invoice number, invoice amount, terms, date paid, amount paid, balance (if applicable), and clients names and address.

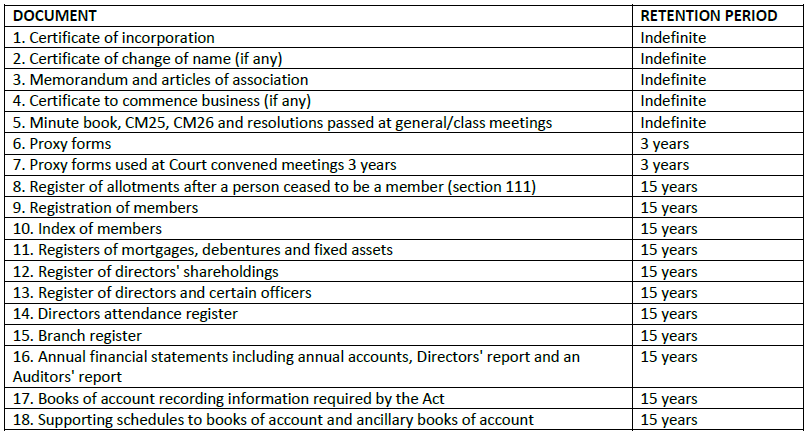

RETENTION PERIOD FOR BUSINESS RECORDS

Retention periods in terms of the Companies Act:

FOR COMPANIES

As a taxpayer, you are required to keep records such as ledgers, cash books, data in electronic form, all supporting documents and any records relating to capital gains or capital losses for a period of five years from the date on which the tax assessment for that year was received by SARS.

However, if objections and appeals have been lodged against assessments, you should keep all relevant records and information until the objection or appeal has been finalised, even if it takes longer than five years to sort out.