Part 1 – MANAGE FINANCES FOR A NEW VENTURE

INTRODUCTION

Finance and accounting systems help drive business performance by efficiently handling a multitude of daily

transactions, sharing valuable information hidden in transactional data, and adapting processes fluidly as business

conditions and regulatory environments change.

Financial Management Systems enables business integrates and streamline financial resources and processes. By

doing so, they achieve a reliable, apples-to-apples view of financial performance across the entire enterprise, as well

as the flexibility and control necessary for adapting to the demands of even the most challenging business

environment. An effective Financial Management system will ensure that the business:

Reduce transaction costs

Shorten process cycle times

Achieve data consistency

Enforce global financial standards and processes

Improve financial transparency

IMPORTANCE OF MANAGING YOUR FINANCES

Financial management is about planning income and expenditure, and making decisions that will enable you to

survive financially.

Financial management includes:

financial planning and budgeting

financial accounting

financial analysis

financial decision-making

financial problem solving

Financial planning

Financial planning is about:

Making sure that the organisation can survive

Making sure the money is being spent in the most efficient way

Making sure that the money is being spent to fulfil the objectives of the organisation

Being able to plan for the future of the organisation in a realistic way.

FINANCIAL ACCOUNTABILITY

Financial accountability means having to account for the way money is spent in the business.

Being able to account for the way the money is spent to:

boards and committees

members, and

the people whom the money is meant to benefit

FINANCIAL RESPONSIBILITY

Managing finances also include meeting all obligations required such as:

Paying staff and accounts on time

Keeping proper records of the money that comes into the organisation and goes out of the organisation

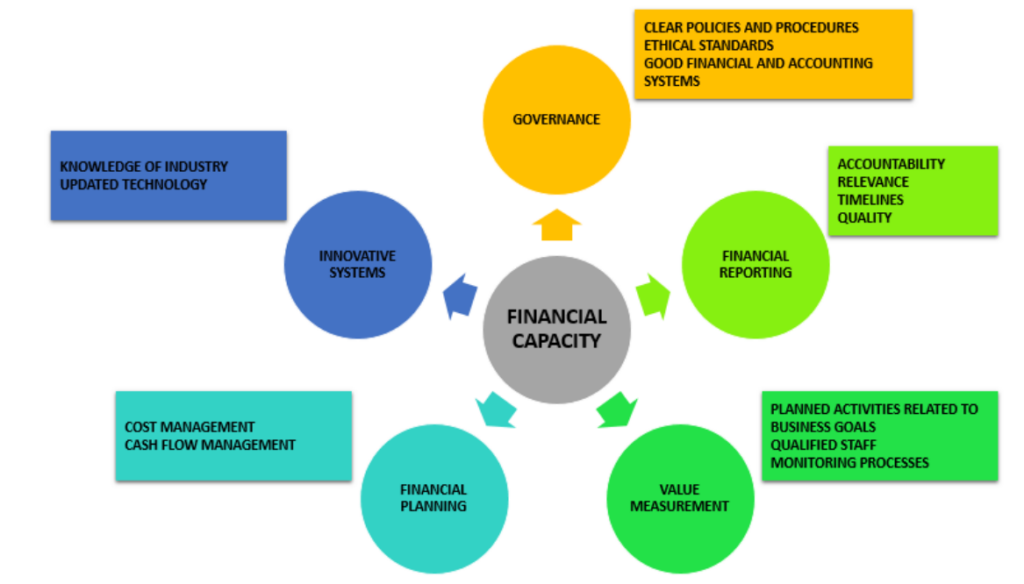

Financial Capacity is the essence of financial management and is summarised in the following diagram:

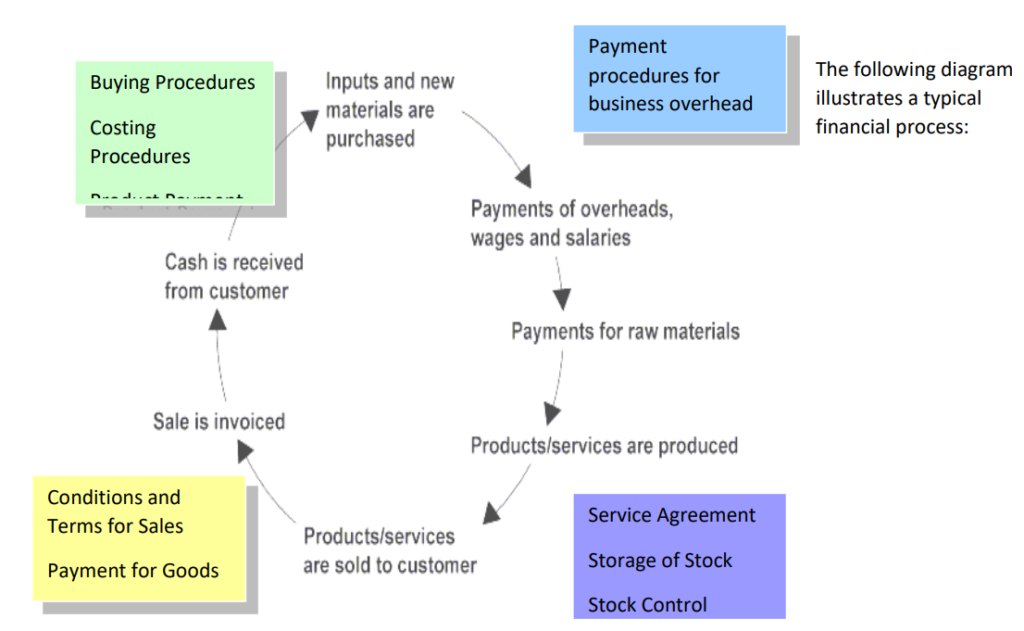

TYPICAL FINANCIAL PROCESSES

FINANCIAL CONCEPTS AND PRINCIPLES

The key financial concepts and principles that apply to new ventures include the following:

- START-UP CAPITAL

Start-up capital is the money needed to begin your business. This would include everything essential for product

development and the product launch. Before going after start-up capital make sure you know how much money you

need, and then how you will apply those funds. Being as specific as possible with the plans for the money will

increase the likelihood that your business will get financed.

Other factors needed before going after start-up capital is a business plan that spells out everything about your

business. Make sure that you spend some extra time on the Executive Summary of your business plan. This will be

the first part of the plan that lenders look at, and it also summarizes all aspects of your business plan. If it doesn’t

grab the attention of the lender your business plan will not get read which means you won’t get the business

financing you are seeking. Other things to consider before going after any capital is that your business has an

established business bank account and your business should be able to be found by the business 411 directory. - WORKING CAPITAL

Working capital is the amount of money that a company has tied up in funding its day to day operations. It is

regarded as the lifeblood of a business without which, a company can become bankrupt. A company has to tie up

money to fund its stocks, credit sales and other current assets, but this is offset by its ability to fund this from current

liabilities liabilities, such as purchases on credit. If a company buys on credit it does not have to tie up (as much)

money in its stocks. In some businesses (such as grocery retail) working capital can even be negative. A business that

buys on credit and sells for cash is being partly funded by its suppliers. - CASH FLOW MANAGEMENT

Cash flow management is the process of monitoring, analysing, and adjusting your business’ cash flows. For small

businesses, the most important aspect of cash flow management is avoiding extended cash shortages, caused by

having too great a gap between cash inflows and outflows. You won’t be able to stay in business if you can’t pay your

bills for any extended length of time!

Therefore, you need to perform a cash flow analysis on a regular basis, and use cash flow forecasting so you can take

the steps necessary to head off cash flow problems. Many software accounting programs have built-in reporting

features that make cash flow analysis easy. This is the first step of cash flow management.

The second step of cash flow management is to develop and use strategies that will maintain an adequate cash flow

for your business. One of the most useful strategies for small businesses is to shorten your cash flow conversion

BANKING AND BANKING ACCOUNTS

A bank is a financial institution that accepts deposits and channels those deposits into lending activities. Banks primarily provide financial services to customers while enriching investors.

TYPES OF BANKS

There are several types of banks in the world, and each has a specific role and function – as well as a domain – in

which they operate. In broad strokes, banks may be divided into several groups on the basis of their activities and

these include investment banks, retail, private, business, and also corporate banks. Many of the larger banks have

multiple divisions covering some or all of these categories.

- Retail banks deal directly with consumers and small business owners. They focus on mass market products

such as current and savings accounts, mortgages and other loans, and credit cards. - Private Banks normally provides wealth management services to high net worth families and individuals.

- Business banks provide services to businesses and other organizations that are medium sized, whereas the

clients of corporate banks are usually major business entities. - Investment banks provide services related to financial markets, such as mergers and acquisitions.

- Offshore banks operate in areas of reduced taxes, as compared to the country in which the investor lives in.

This is why most offshore banks are private banks. - Community banks are monetary organizations operated on a local basis, while community development

banks cater to the populations, or markets, which have typically not been served properly. - Postal savings banks are basically savings banks that operate in conjunction with the national postal systems

of South Africa. It targets the low income earners in the society - Building societies where traditionally mutually owned by their customers, which provide a full range of retail

banking services, but with a particular focus on mortgages.

TYPES OF BANK ACCOUNTS

There are different types of banking accounts offered by banks. The

following are the most common ones.

BASIC BANK ACCOUNTS (SAVINGS ACCOUNT)

Basic bank accounts offer a convenient place to keep money you need for

everyday use. You can arrange to have wages, State Pension and benefits

or tax credits paid into one. You can also pay in cheques or cash free of

charge, and set up ‘direct debits’ which pay regular bills automatically

from your account.

With a basic bank account, you get a cash card which you can use at a

bank machine to withdraw cash. Some also offer a ‘debit card’ that you can pay for items with, and get ‘cashback’;

but with a basic account these will only work if there’s enough money in your account.

You don’t get a cheque book with a basic bank account, and you can’t take out more money than is in the account

(‘go overdrawn’). For this reason, basic bank accounts are useful for anyone worried about overspending.

CURRENT ACCOUNTS

Current accounts have more features than basic bank accounts. For example, they usually offer:

cheque book

cheque guarantee card (acts as a ‘guarantee’ so makes cheques more widely acceptable)

debit card (some allow payments without checking your account)

direct debits (automatic bill payments direct from your account)

standing orders (regular set payments from your account to someone of your choice)

BACS (Bankers’ automated clearing service) – the facility to accept payments directly into your account (e.g

from your employer), or for you to make one-off payments to someone else out of the account

overdraft facility – the bank may allow you to go overdrawn up to a certain amount; but you need to arrange

this in advance and charges apply (you pay extra charges if you go overdrawn without an agreement)

THE IMPORTANCE OF A BANK ACCOUNT TO A BUSINESS

Many small business owners avoid or do not pay too much attention when considering whether to open up a bank

account in their business name. They make the mistake of using their personal account to carry out their business

transactions, just so they can save a small amount of money required to open a new business bank account. The

following are some of the importance of a bank account to a business:

GIVES THE BUSINESS A PROFESSIONAL IMAGE

A business account gives your business a more professional look when dealing with your customers or clients. Using

your personal account for business purposes gives the impression you are not really serious regarding your business

and it is more like a hobby.

IT MAKES IT EASY WHEN PREPARING BUSINESS ACCOUNTS

Having a separate business account proves to be beneficial when you need to complete the accounts for the

business and any related tax returns. Indeed, you can quickly check the income and expenses for the year, rather

than having the hassle of separating your personal and business transactions if you only have a personal account.

IT HELPS TO SHOW TRANSPARENCY OF THE BUSINESS TO AUTHORITIES

Another good reason to have a business bank account is to show the tax authorities that your business is transparent

in terms of the financial transactions it carries out. All the income and expenses should be accounted for through the

business account. Thus, if SARS Customs & Revenue want to look at your records, this will demonstrate that you are

declaring all your income and only claiming expenses related to business.

THE BANK ACCOUNT GIVES THE BUSINESS ACCESS WITH ADDITIONAL PERKS AND FACILITIES

Opening a company account with a bank also has other additional perks. For example, you can usually obtain free

banking for at least a year as a new business. Also some banks even offer new clients special deals on accounting

software to use in their businesses. Lastly, it may be easier for you to obtain a business overdraft or loan if you have

a company bank account.

Some entrepreneurs are put off from opening a business bank account because they think it will be complicated in

terms of the formalities and legalities. This is a misconception as it is very easy to open a bank account most of the

time.

MINIMAL BALANCE THAT YOU NEED TO MAINTAIN

A company bank account may initially seem to be an extra overhead on your business, but the amount paid will be

worth in terms of the time and money you will save by not having to separate out your business transactions from

your personal transactions. Having a business bank account also sends a clear message to other businesses you deal

with and the tax authorities that you are a proper business with nothing to hide.

OPERATING A BUSINESS ACCOUNT

It is critical to keep track of funds in the bank account (e.g. by checking your bank statement and recording the

balance of funds available at any point). It is important to monitor Direct Debits, Standing Orders etc for accurate

recording of receipts and payments from the bank account.

CHEQUES

You should issue a cheque for payment only if you are certain that sufficient funds are available in the account to

meet the payment. The bank is most likely to return the cheque by not honouring if sufficient funds are not

available in the account. It is paramount to make prior arrangements with the bank for temporary overdrafts where

there are gaps in meeting financial commitments. The golden rule is not to issue cheques unless sufficient funds are

available in the account after taking into account all the payments channelled through the account including bank

charges.

It is also critical to recognize that cheques issued by others and deposited to your account would not be regarded as

funds available until such time the said cheque has been realized and recorded in your bank account as a receipt.

This is part of the clearing process delay and varies depending on the issuing bank, branch, couriering timings,

central clearing timings etc.

STATEMENTS

The banks issue periodic statements for your accounts showing all the transactions through the account. The period

for which the statements are issued depends on the type of account and your needs. It is customary to issue

monthly statements for current accounts and the customer could request for the preferred timing for statements.

The bank may levy a charge for special requests of customers. It is advisable to check the bank statements for

accuracy. Mistakes are rare but may occur. The bank should be informed promptly for any inaccuracies. If a cheque

guarantee card is given, it is advisable to keep in a safe place separate from the cheque book

LEGITIMACY

Further the bank is legally required to take steps in ensuring that transactions undertaken by the customers through

the bank account do not contravene the law. Money laundering is a matter of serious concern to regulators and

therefore the banks are required to be vigilant. For this purpose, it is not uncommon for banks to seek verification

from customers with regard to unusual transactions as a step towards protecting against unlawful conduct. The

regulators / state authorities are generally given statutory rights to have access to information about bank accounts

of customers and transactions. Therefore, customers must ensure that bank accounts are only used for legitimate

transactions

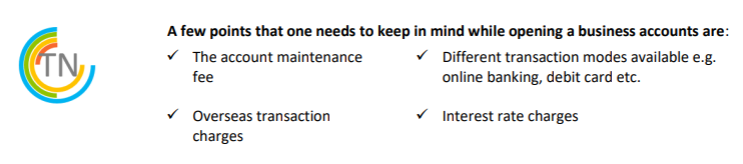

BANK CHARGES

It is also advisable to check the basis on which charges are levied against any account for facilities offered. Financial

institutions thrive on levying various forms of charges though they appear small to an individual customer, in

aggregation the amounts run into billions. These are hard earned money of individuals just taken off by financial

institutions due to ignorance or carelessness of customers.

The banks are in a unique position and do not need to obtain your consent for levying charges. The agreement for

opening a bank account / securing facilities would generally give the bank the right to levy charges to the account

and there is no legal requirement to consult the customer. The bank would automatically charge the account for any

dues even if funds are not available in the account for recovery. Thereafter, the bank would levy further charges for

overdrawing the account. Sadly, the bases of arriving at the figures are never disclosed in the statements.

The basis of computing charges and interest vary from, bank to bank. Further, factors such as credit rating, overall

market rates, duration, type of facilities required etc, will have a bearing on the charges / interest levied. For

example, the overdraft rate is linked to the risk level of the customer and the bank’s cost of funds. High Street banks

today offer an extensive range of financial products/services. Bank accounts, credit cards, loans, bonds, insurance,

savings, investments, pensions, travel, shares dealings are some of the facilities that could be obtained from a High

Street banker.

ONLINE AND TELEPHONE BANKING

Many banks today offer on line facilities for managing bank accounts which means 24-hour banking. Telephone

banking is generally limited to extended office hours. There are claims that the security issues on internet banking

are weak and therefore banks are exposing customers to risks of hacking. It is understood that teething problems at

infantry stages are part and parcel of new concepts and systems implemented. However, benefits accruing from

online facilities outweigh such drawbacks. Customers must support and commend the efforts taken by financial

institutions to invest and promote the concepts that are likely to change the way financial products would be used

for betterment of our lives.

There is no doubt that the facility offered to operate a bank account from a location and time of your choice is a

major breakthrough in managing our finances. The customers must encourage growth of online facilities to enhance

competition, efficiency and effectiveness of markets to a scale that boundaries are broken for the benefit of all.

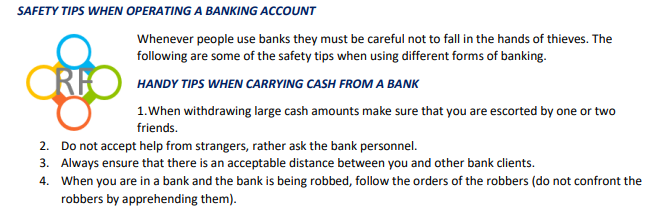

HANDY TIPS TO KEEP IN MIND WHEN USING ATMS:

- Choose your ATMs carefully – make sure it’s clearly visible and well lit

- Don´t let anyone distract or assist you when you are using the ATM

- Be wary of strangers around you, make sure that they are not watching you key in your PIN

- Key in your PIN only when prompted to do so by the screen

- Use your free hand as a shield when keying in your PIN (to protect you from secret cameras)

- Do not count your money at the ATM

INTERNET BANKING SAFETY TIPS

- When accessing your account through the internet make sure that you verify the site certificate.

- Ensure that you are on the secure Internet banking website by checking that the URL begins with “https”

rather than “http”. - Always ensure the secrecy of your Profile number, PIN and Password.

- Your digital banking profile number is not a derivative of any of your bank account numbers.

- Never disclose your PIN number and Password to anyone. This information is stored in a manner that bank

employees cannot access. - Make sure that your logoff and close your browser after banking online.

- As an added security measure, some banks make use of a cryptographic generated reference number which

is sent to you via an SMS on your mobile phone. This feature ensures two-factor authorisation when

performing selected functions. - Check your statements regularly for any unauthorised entries.

GENERAL TIPS

- Check that the card is actually yours before and after a transaction

- If only one ATM is working in a specific area be conscious of the fact that the others could have been

sabotaged to direct, you to that one - Set a low daily and monthly withdrawal limit on your account, but note that this limit is not always

applicable to purchases - Cancel your card immediately if it is lost, stolen or retained by an ATM

- Immediately report your lost or stolen cards to your bank and police

- Safe use of Personal Identification Numbers (PINs), passwords and credit cards

- The bank tells its clients to be careful about tearing up the PIN that they send you with a new card. But did

you know that there are more things that you can do to protect your number and ensure that nobody tries

to use your account? Debit cards are very attractive to would-be thieves because immediate cash is always

more desirable than goods on a credit card. Here are some additional, simple steps for you to take to protect

your PIN (personal identification number)

STEPS IN SAFEGUARDING YOUR PIN NUMBER

- Never share the PIN. It might be tempting to trust a friend or a family member with your PIN but it is not a

good idea - Never give out your PIN in response to e-mail or telephone requests

- Shield your PIN when using it. Use your hand, a piece of paper etc. to shield the PIN as you enter it into a

bank machine or a store machine. Be especially vigilant in store queues, where somebody may be paying

more attention than you. Also, be wary of “card skimmers” at ATMs - Choose a PIN password that is not obvious. Your birth date, wedding anniversary, phone number and home

address are obvious picks, so just do not use them. Instead, think of numbers unrelated to major events and

addresses in your life to create your PIN - Do not write your PIN down on the card, ever. Do not even write it in a diary. If you must write it down,

disguise it in some way or put it somewhere totally unrelated to the card, such as in the middle of

Shakespeare’s Complete Works - Vary your PIN on different cards. Don’t keep the same PIN for all your cards. Have a different PIN for each

one, so that if you do happen to lose your wallet, it will be much harder for the PINs to be cracked - Contact your bank immediately if your card is stolen or lost. Tell them immediately if you think that there is

anything that may compromise your PIN, such as an easy PIN, other ID in your wallet making it easy to work

out or, horror of all horrors, the PIN being written down somewhere in the wallet or on the card. Get the

bank to cancel the card immediately - Be proactive. If you suspect any fraudulent activity using a card still in your possession, apart from notifying

the bank and the police, have your PIN changed immediately

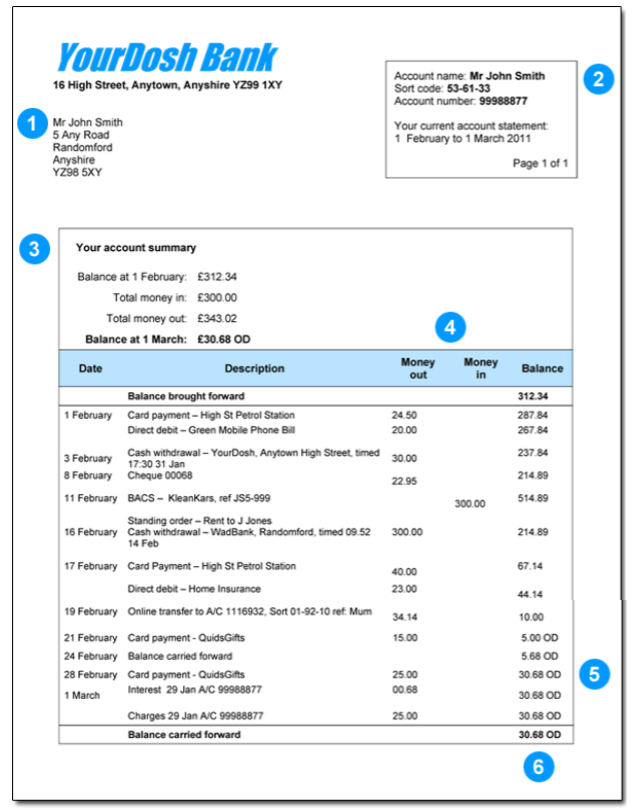

UNDERSTANDING THE BANK STATEMENT

The bank statement is a handy way of seeing all your incomings and your outgoings at once. It’s definitely a good

idea to open and read your bank statements so you can check you’ve received what you expected, and that you

recognise all the payments going out too. We’ll help you to understand how to read and make sense of your bank

statement.

Your bank statement might be sent monthly, quarterly or yearly, depending on what type of account you have. Have

a look at the table below for a simple explanation:

You’ll probably get your statement through the post, but if you bank online, you can also access it on the internet,

and possibly opt out of receiving paper statements.

Your statement will show all the money in and out for your account during the set period (monthly or

otherwise). The details will include the date, amount and an identifier for the payment (such as a shop name for

purchases). For benefits, the identifier could be the Department for Work and Pensions, Jobcentre Plus or HM

Revenue and Customs, or your local council if it’s housing benefit.

Here’s our handy example of a bank statement showing the kinds of things you’ll see. Yours might look a bit

different, but the same kind of information will be on there.

EXAMPLE BANK STATEMENT

WHAT DOES THIS MEAN?

- YOUR PERSONAL INFORMATION

This is your name and permanent home address. Make sure it’s right, and that you haven’t got someone else’s bank

statement! It’s really important to tell your bank if you move house, so they can safely and securely send any

information about your account to you. - YOUR ACCOUNT INFORMATION

This will show the name you used to open your account with. In addition, it will show the type of account (such as a

cheque or savings account or credit card). It will also show your account number and branch code. Your sort code is

a six-digit number with dashes in (for example, 53-61-33) that helps the whole banking system identify which bank

and local branch your account’s based at. - STATEMENT SUMMARY

You’ll be shown a basic account summary, which will usually show the total amounts paid in and out during that

month (or other period if it’s a savings account). You can also see here that there’s a closing balance – this means

the balance of your account at the time the statement was sent out. - MONTHLY INCOMINGS AND OUTGOINGS

On your statement there will be two columns showing money paid into your account (credits) and one for money

paid out (debits). Your statement will be ordered by date, so it’ll show the oldest payments at the top, working

down to the most recent. Next to each payment is also a description, which shows where you were when you made

the payment (a shop or cash machine) or who you paid. There might also be standing orders or direct debits you’ve

arranged. This information should also be available for the ‘money in’ section – it might say ‘bank transfer’ for your

wages, ‘counter credit’ for cash or cheques you’ve paid in at your branch, refunds from shops, or automated

payments made by the state to you, such as benefits.

Sometimes payments will show up on your statement a few days after you actually made them. For example, if you

buy something with your debit card in a shop (or withdraw cash from a machine), it might not show up on your

statement for a few days. This is because it takes time for payments to go through the banking system, especially

over a weekend. When this happens, the actual date you made the purchase or cash withdrawal should be shown in

the ‘description’ column.

In the far right column, you can see a running total, the ‘balance’. This means the total you have in your account

each day, as a result of money in and out of your account. - GOING OVERDRAWN

In your balance column, sometimes you’ll see the letters OD or a minus sign next to the figure. This means your

account’s gone overdrawn and you’ve spent more money than you had in your account. So, if you had R10.00 in your

account, but buy something on your debit card for R15.00, you’ll go overdrawn by R5 (R10-R15=-R5). You’ll have to

pay this back to the bank, along with any interest and charges unless you have an interest-free overdraft. The longer

you leave it to pay pack your overdraft, the longer you’ll be charged interest on it, and the harder you may find it to

get out of your overdraft.

That’s why it’s really important not to become reliant on your overdraft it costs you more money in the long-term to

borrow from the bank like this. It’s a good idea to do all you can to stay in ‘the black’ (plus numbers) and get out of

‘the red’ (minus numbers). It could be a spiral into debt, so make sure you’re not always right at the limit of your

overdraft. - BANK CHARGES

If your account’s gone overdrawn beyond your agreed limit, or you didn’t have an agreed overdraft, the bank will

charge you for ‘unarranged borrowing’. They can also charge you if you pay in a cheque that bounces (that’s when

the other person doesn’t have enough in their account to cover the amount they wrote the cheque for). Banks have

to notify you before they take any money from your account for these charges.